Is the massive Microsoft AI Investment spree a smart long-term bet or a costly detour that markets are suddenly doubting?

Is Microsoft’s selloff justified?

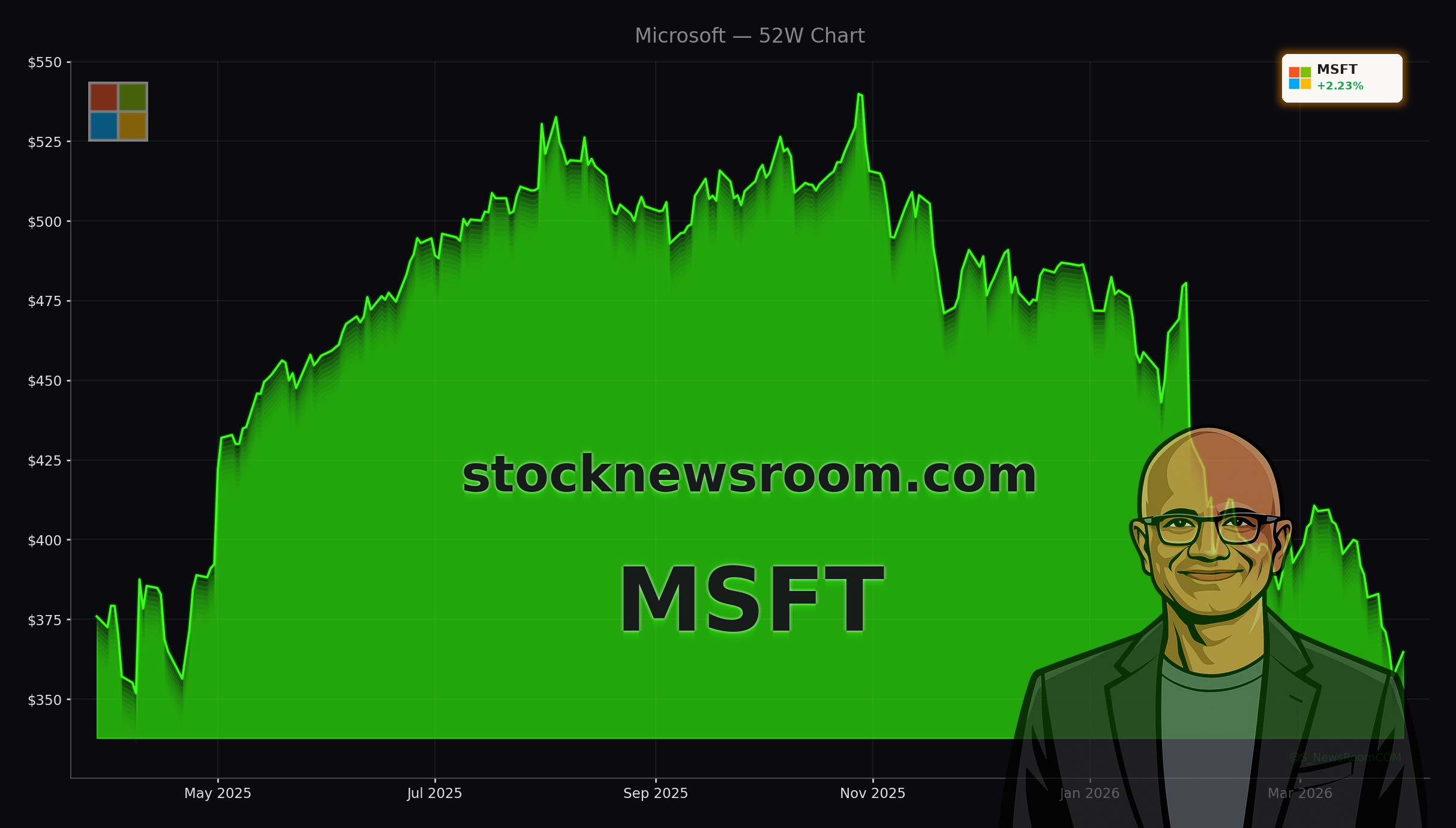

Microsoft Corporation (MSFT) is up about 1.3% today to $361.50, but that bounce barely dents the damage from a brutal first quarter. The stock is roughly 25% lower year‑to‑date and about 35% below its October 2025 all‑time high near $480, putting it among the weakest performers in the so‑called Magnificent Seven alongside Tesla.

Unlike past drawdowns driven by recessions or structural issues, this slump is more about “growth pains.” Microsoft just reported another double‑digit revenue quarter, with total sales up around 17% and Microsoft Cloud revenue growing 26%. Yet the market is punishing the shares over concerns that the company and its hyperscaler peers are overspending on AI infrastructure just as the initial hype cools and monetization takes longer than expected.

Valuation has compressed sharply. Recent estimates put Microsoft at about 19x forward earnings and a forward price‑to‑cash‑flow multiple of roughly 13.7, the lowest in years and well below many other mega‑caps. By comparison, Apple trades at about 24x forward cash flow and Tesla above 80x, while NVIDIA remains richly valued despite its own pullback. This re‑rating means the Microsoft AI Investment story is now being priced more like a high‑quality compounder than a speculative AI favorite.

How big is the Microsoft AI Investment wave?

Behind the rerating is a staggering capital‑expenditure cycle. Microsoft is one of the core hyperscalers, alongside Amazon, Alphabet, Meta and Oracle, that are driving what could be the largest infrastructure build‑out in tech history. Collectively, these firms are expected to spend around $650–700 billion on CapEx in 2026, up roughly 60–70% from 2025, with Microsoft a leading contributor.

Internally, Microsoft has signaled AI‑driven CapEx of roughly $140–150 billion spread across data centers, networking, custom silicon and capacity commitments to GPU suppliers and AI partners. Azure alone is now generating over $30 billion in quarterly revenue, so management argues that scaling infrastructure is a rational response to surging cloud and AI demand, not a reckless bet.

Still, the timing has unnerved Wall Street. Elevated CapEx tends to pressure free cash flow and operating margins in the short term, and there are open questions over how quickly AI‑powered services like Copilot can be monetized across the installed base. Skeptics also point to intensifying cloud competition, with IndexBox highlighting that Google Cloud’s revenue growth is currently accelerating faster than Azure’s, stirring fears of market‑share skirmishes that might weigh on pricing.

What role does green power play in the strategy?

The spending surge is not just on servers and chips. A less appreciated piece of the Microsoft AI Investment thesis is energy. AI data centers are extremely power‑hungry, and ensuring reliable, low‑carbon electricity at scale has become a strategic priority.

In May 2024, Microsoft signed a colossal 10.5‑gigawatt renewable‑energy agreement with Brookfield Renewable, widely described as the largest clean‑power deal ever inked by a corporate buyer. Deliveries to Microsoft are slated to begin this year, effectively locking in a long‑term pipeline of greener electricity to feed its expanding global data‑center footprint.

This mega‑deal accomplishes three things. First, it offers better visibility on energy costs for AI workloads in an environment of volatile power prices. Second, it supports Microsoft’s pledge to run its operations on 100% renewable energy and become carbon negative, strengthening its ESG profile for institutional investors. Third, it potentially creates a competitive moat: not every rival will be able to secure comparable volumes of low‑carbon power at scale.

For shareholders, the Brookfield agreement underscores how far‑reaching the Microsoft AI Investment theme has become. It is no longer just about software and GPUs; it spans power infrastructure, land, cooling, and grid‑scale planning.

Is Copilot still a credible AI growth driver?

A key controversy around Microsoft’s AI narrative is whether Copilot is living up to expectations. Critics argue that the company has lost its status as clear AI frontrunner, pointing to turbulence in the relationship with OpenAI and tepid enthusiasm from some users about Copilot’s day‑to‑day utility.

Management is pushing back with a steady drumbeat of product updates. Today, Reuters reported that Microsoft is rolling out upgraded AI features for its Copilot research assistant, including a new “Critique” capability that allows Copilot’s Researcher agent to use multiple models such as OpenAI’s GPT and Anthropic’s Claude in tandem. Claude can review and refine GPT’s responses, aiming to reduce hallucinations and improve factual accuracy.

SiliconANGLE adds that Microsoft is launching Copilot Cowork for Microsoft 365, an agentic automation tool that can manage long‑running, multi‑step workflows across apps like Outlook, Teams and Excel. Rather than just generating individual drafts or summaries, Cowork is designed to plan and execute tasks end‑to‑end while allowing human oversight. The multi‑model “council” approach again leans on both OpenAI and Anthropic models to boost reliability.

On the demand side, Microsoft says more than 80% of Fortune 500 companies are already using some form of its AI technologies, with broad pilots and rollouts of Microsoft 365 Copilot in large enterprises. Revenue growth in the Intelligent Cloud segment has held in the mid‑20s percentage range, suggesting that AI services layered on top of Azure and Office are starting to contribute meaningfully, even if they are not yet a standalone blockbuster.

How do analysts view Microsoft’s risk‑reward?

Despite the sharp drawdown, the sell‑side has largely stuck with bullish calls. One of the most optimistic voices is DBS Bank, where analyst Sachin Mittal maintains a Street‑high price target of $678, implying more than 80% upside from current levels. His thesis is that the market is over‑discounting short‑term AI monetization risks and underestimating the durability of Microsoft’s software and cloud cash engines.

Other strategists echo the notion that the latest correction looks more like a valuation reset than the start of a structural decline. Several growth funds highlight Microsoft’s historically low leverage ratio (debt at less than 20% of capital), immense free‑cash‑flow generation and a diversified portfolio spanning enterprise software, Azure, gaming, and cybersecurity as reasons the downside appears limited versus many pure‑play AI names.

On the flip side, IndexBox notes that the recent 7% weekly drop in the share price, despite strong cloud results, underscores just how fragile sentiment around AI CapEx has become. RBC Capital’s equity strategy team has also warned that U.S. mega‑caps are losing some of their valuation premium versus international markets, meaning that even quality names like Microsoft can underperform if investors rotate toward cheaper regions or sectors.

In cybersecurity, Morgan Stanley recently highlighted Microsoft as one of its top picks to benefit from the surge in AI‑driven security demand, alongside Palo Alto Networks and CrowdStrike. The bank argues that as enterprises deploy more AI, protecting identities, endpoints and cloud workloads will become even more critical, and vendors with integrated AI security stacks could gain share.

What does this mean for portfolios?

At around 19x forward earnings and roughly in line with or even slightly below the S&P 500’s multiple, Microsoft is trading at a valuation that many retirees and conservative investors may find surprisingly reasonable for a company still expected to grow revenue and EPS in the low‑to‑mid‑teens annually. The stock also offers a modest dividend yield near 1%, backed by more than $100 billion in trailing 12‑month profit.

For diversified index investors, Microsoft remains a core building block. It is a top‑two or top‑three holding in many broad U.S. funds, from S&P 500 ETFs to mega‑cap strategies, and it often sits alongside NVIDIA and Apple as a primary driver of returns. That concentration cuts both ways: when the Microsoft AI Investment story is in favor, it can power index gains; when investors question AI CapEx and cloud competition, the headwinds can weigh on broader benchmarks like the NASDAQ‑100.

Tactically, traders are watching technical support in the $340–350 range. Several chart analysts view that zone as a critical floor; if it holds, a sharp 20–25% relief rally back toward the low‑$400s is seen as plausible. If it fails decisively, the next leg of the selloff could unfold as AI infrastructure fears and macro jitters compound.

Related Coverage

For a deeper dive into how Copilot specifically fits into the Microsoft AI Investment blueprint, including the company’s $72 billion AI build‑out and its ambition to turn agentic AI into a mainstream productivity tool, see Microsoft Copilot Strategy Boom and the $72B AI Bet. That analysis examines whether the Copilot push can become the next major growth leg for Microsoft’s software and cloud ecosystem.

Investors tracking the broader AI hardware and memory cycle may also want to read Micron Technology AI Memory Boom: -5.2% TurboQuant Shock. That piece looks at whether the recent sell‑off in Micron shares signals that the AI memory boom is already cracking or instead presents a rare entry point, an important backdrop for understanding downstream impacts of hyperscaler AI spending.

In sum, the Microsoft AI Investment cycle is at a pivotal moment: valuation is cheap by its own history, execution in cloud and AI remains strong, but the market is demanding faster proof that record CapEx and mega energy deals will translate into durable, high‑margin growth. For long‑term investors willing to ride out volatility, the next few quarters should reveal whether this is a classic opportunity to buy fear in a blue‑chip franchise or a sign that AI infrastructure spending needs to cool before sentiment can fully recover.