Is Microsoft’s aggressive AI spending spree a mispriced risk or the foundation for its next trillion dollars in value?

Is Microsoft’s stock slump mispricing AI?

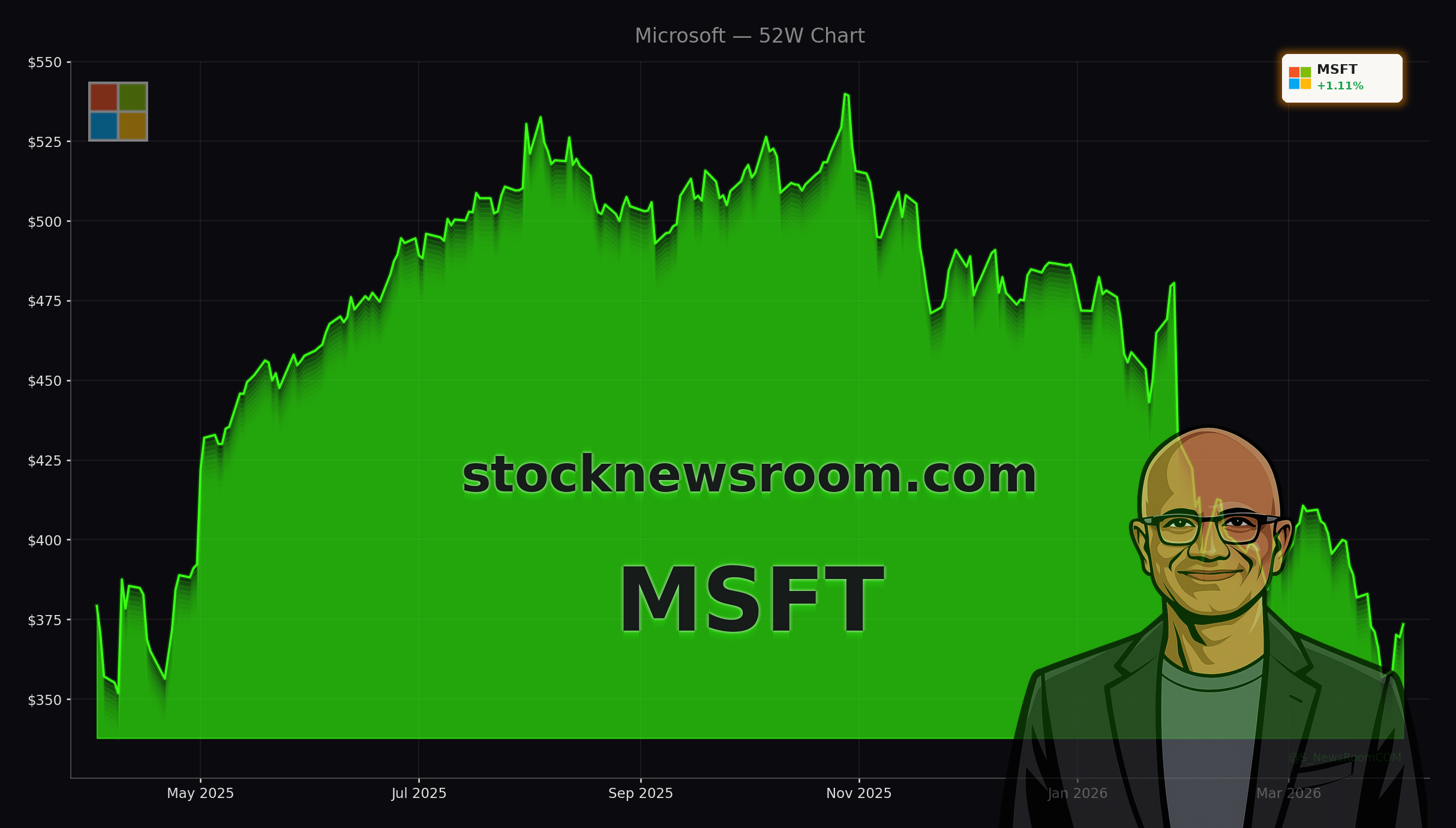

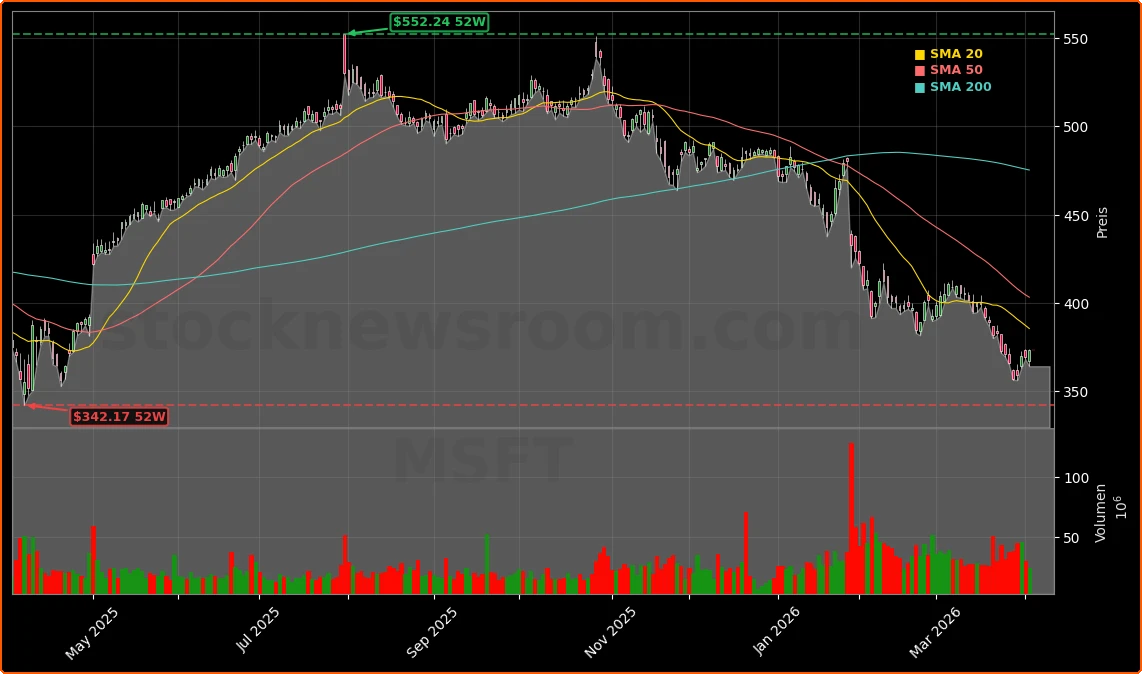

Microsoft Corporation gained about 1.1% to $373.46 on Thursday, modestly rebounding from a steep year‑to‑date decline of roughly 22.8% and hovering above its 52‑week low near $344. The move contrasts with weakness in chip names like NVIDIA, which had led the market earlier in the week but cooled as investors rotated out of the most crowded AI trades. Despite the bruising pullback, Microsoft still carries a market cap of about $2.77 trillion and remains a core pillar of the S&P 500 and Nasdaq Composite.

The Microsoft AI Strategy is central to explaining the disconnect between the stock price and analyst optimism. Capital expenditures surged 89% year over year in the latest reported quarter to $29.88 billion, pushing full‑year FY2025 capex to $64.55 billion and compressing free cash flow slightly to $71.61 billion. That spending is flowing into data centers, custom AI chips and the Azure platform to capture surging demand for generative AI workloads, even as some investors question the timing of the payoff.

How strong is Azure and the AI backlog?

Operationally, Microsoft is still hitting on almost every cylinder. Total revenue in the most recent quarter grew 16.7% year over year to $81.27 billion, while Microsoft Cloud revenue climbed 26%. Azure itself posted 39% growth and is guiding for 37%–38% in the upcoming quarter, one of its best stretches in the past decade. Management noted that AI demand is exceeding available compute capacity, suggesting the infrastructure build‑out is chasing, not leading, customer requirements.

A key pillar of the Microsoft AI Strategy is locking in long‑term usage commitments. Commercial remaining performance obligation (cRPO) jumped 110% to $625 billion, reflecting contracted future revenue across cloud and enterprise software. The recapitalized OpenAI partnership alone added about $250 billion in incremental Azure commitments and gives Microsoft intellectual property rights to OpenAI models through 2032. That positioning has effectively made Azure a default infrastructure layer for many AI applications, even as competitors like Apple and Alphabet sharpen their own cloud and AI stacks.

What does the Japan AI push signal?

Microsoft’s latest move underscores how global its AI ambitions have become. The company unveiled a four‑year, $10 billion investment plan in Japan aimed at expanding AI and cloud infrastructure, strengthening cybersecurity cooperation, and training over one million workers in AI‑related skills. The initiative includes partnerships with Sakura Internet and SoftBank to deliver compute capacity tailored to Japan’s growing AI needs, and it aligns with Tokyo’s economic security agenda.

This overseas push dovetails with a broader Microsoft AI Strategy that couples infrastructure with workforce development. Similar datacenter academy programs are being rolled out with universities, such as a recently announced partnership focused on skilling students for datacenter and AI operations. For U.S. investors, the Japan package is another data point that management is willing to front‑load billions in capex to secure regional cloud share and regulatory goodwill, even if that means tolerating near‑term margin drag.

Are analysts still backing Microsoft?

Wall Street remains overwhelmingly bullish. Across 58 covering analysts, 55 rate the stock a Buy or Strong Buy and none carry a Sell, with an average price target of about $587 implying more than 57% upside from current levels. Research desks at large U.S. banks, including Goldman Sachs and Morgan Stanley, continue to emphasize Microsoft’s cloud momentum and the scale of its $625 billion backlog as reasons the multiple can re‑rate once the capex cycle peaks.

Valuation has already reset meaningfully. At roughly 23 times trailing earnings and a little over 20 times forward estimates, Microsoft trades below its three‑year average forward multiple around 31. Some analysts compare the setup to Alphabet’s 2025 trough, arguing Microsoft could become the “Alphabet of 2026” if sentiment inflects while Azure and Copilot revenue keep compounding. Still, others warn that rivals like Alphabet and Tesla are pushing aggressively into AI and automation, and that Microsoft must prove its OpenAI‑centric model does not leave it dependent on an external partner whose losses recently topped $3 billion in a single quarter.

How risky is the AI capex bet for shareholders?

The main near‑term risk is that AI returns arrive slower than the spending. With Microsoft investing tens of billions annually into datacenters, custom silicon and software R&D, free‑cash‑flow growth has flattened even as earnings per share continue to beat expectations. A “Great Rotation” away from richly valued tech has amplified that concern, hitting the “Magnificent Seven” — including NVIDIA, Apple, Tesla and Microsoft — and erasing more than $2 trillion in combined market value so far this year.

On the demand side, Copilot adoption within Microsoft 365 looks encouraging: consumer cloud revenue rose 29% with higher average revenue per user as customers pay for AI features, suggesting that AI is enhancing rather than cannibalizing the productivity suite. But bears argue that cheaper AI‑generated alternatives could eventually pressure pricing in Office and other software products. For now, there are few signs of erosion, but investors will be watching the next earnings report, expected in late April, for any hint that growth in Azure or Copilot is slowing just as capex remains elevated.

Related Coverage

For a deeper dive into how surging infrastructure spending is reshaping the balance between growth and profitability, see “Microsoft AI Investments $145B Shock and Stock Slump”, which dissects whether the massive build‑out is a springboard for future dominance or a drag on near‑term returns. Investors comparing big‑tech AI roadmaps can also read “Alphabet AI Strategy Warning: TPU Edge, SpaceX Upside and Legal Risk” for a look at how Google’s custom chips and legal overhangs stack up against Microsoft’s more partnership‑driven model.

In the end, the Microsoft AI Strategy is forcing the market to choose between short‑term cash‑flow pressure and long‑term platform dominance. The combination of a 39% Azure growth rate, a $625 billion cloud backlog and a $10 billion Japan AI push suggests management is betting heavily that demand will justify today’s spending. For U.S. investors willing to stomach volatility, the next several quarters of earnings and capex guidance will be crucial in determining whether the current sell‑off marks a rare opportunity or a warning that the AI payoff will take longer than hoped.