Is the latest Microsoft Forecast signaling a temporary AI setback or the start of a long-term value opportunity into 2030?

Is Microsoft still a core AI holding?

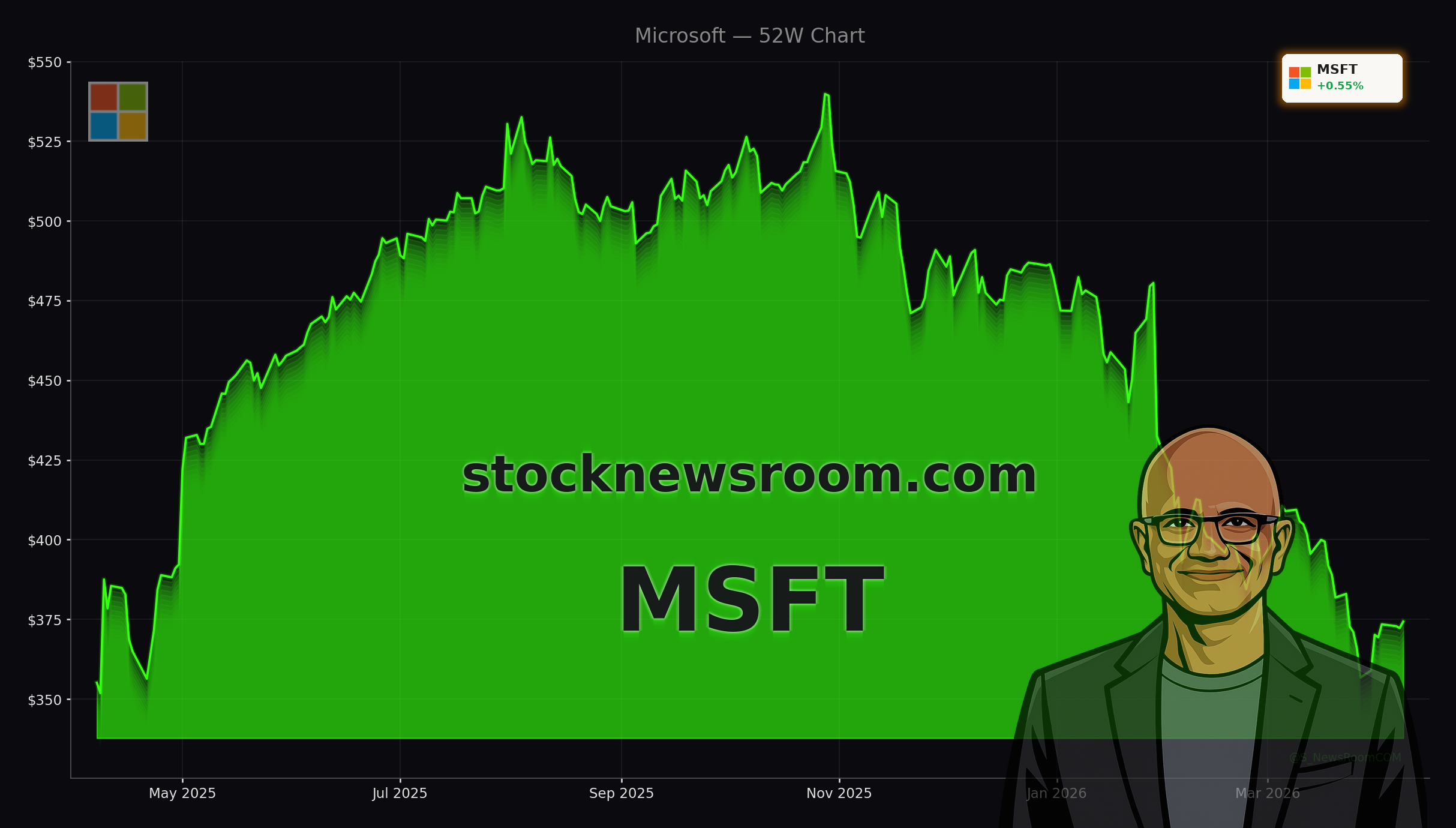

Microsoft (MSFT) trades around $374.33 in Thursday’s pre‑market, up a fraction from Wednesday’s close but still roughly a third below its 52‑week high near $552. After one of its worst first quarters in almost twenty years and a drop of more than 20% year‑to‑date, the stock has lost much of the valuation premium it historically commanded over the S&P 500. Microsoft now changes hands at roughly 19–23x forward earnings, essentially in line with the broader index despite growing revenue much faster.

The business fundamentals tell a different story than the share price. In its most recent reported quarter, Microsoft delivered about 17% revenue growth, with Q2 FY2026 revenue at $81.27 billion, up 16.7% year over year. Non‑GAAP EPS of $4.14 beat consensus by more than 7%. The outperformance was driven by a 39% surge in Azure and other cloud services and a 110% jump in commercial remaining performance obligation (RPO) to $625 billion, giving Microsoft multi‑year revenue visibility most peers cannot match.

Yet sentiment remains fragile. Investors worry that Microsoft — a line item in almost every Global 2000 IT budget — could face incremental cuts as enterprises rebalance spending amid a platform shift toward generative AI. At the same time, early versions of Copilot have been criticized as less robust than hoped, raising questions about near‑term monetization.

How does the Microsoft Forecast stack up to Big Tech?

The current Microsoft Forecast from major research shops points to a company growing faster than its largest peers while trading at a relative discount. Wall Street projects mid‑teens revenue growth in the coming quarters, comfortably above the 10% threshold many portfolio managers use to define a true growth stock. Some models see Microsoft earning around $19 per share by the end of fiscal 2027; placing a 30x multiple on that figure implies a price near $570, more than 50% above recent levels.

Valuation comparisons are also instructive. High‑margin, mega‑cap peers like Apple and Alphabet still trade at richer earnings multiples, in the high‑20s to low‑30s range. That suggests Microsoft’s lost premium is not about structural deterioration but about a cyclical derating after an AI euphoria peak. Several institutional investors appear to be leaning into this dislocation: Mn Services Vermogensbeheer B.V. recently increased its Microsoft stake by 2.3%, making the stock its fourth‑largest position, and Sherman Wealth Management LLC initiated a new position in Q4. Even at the political level, Representative Richard McCormick of Georgia added Microsoft to his Roth IRA, underscoring continued confidence from a diverse investor base.

Price‑target models embed this optimism. One detailed framework values Microsoft at $491.47 over the next 12 months, implying roughly 30–35% upside from current prices and rating the stock a BUY with high confidence. The same model extends the Microsoft Forecast out to 2030 with a base‑case path through $650 in 2028 and $818 by 2030, and a bull‑case scenario that pushes above $1,100 if AI monetization accelerates.

What are the key risks around AI and Copilot?

Under the surface of the bullish Microsoft Forecast are real risks. Capital expenditures have surged, nearly doubling year over year in Q2 FY2026 to $29.8 billion as Microsoft races NVIDIA, Apple and other hyperscale players to build AI data centers. Free cash flow actually declined about 3% in FY2025 to $71.6 billion, despite top‑line growth, as AI infrastructure spending pulled forward.

On the demand side, Microsoft’s AI backlog is enormous. The company’s $625 billion RPO and OpenAI’s commitment to purchase roughly $250 billion of incremental Azure services create a strong structural floor under cloud and AI revenue. But those commitments must translate into profitable usage. Losses from the OpenAI stake have widened sharply, hitting $3.1 billion in Q1 FY2026 versus $523 million a year earlier, highlighting the volatility tied to this partnership.

Execution also matters. The More Personal Computing segment shrank 3% last quarter, showing that not all business lines are benefiting equally from the AI wave. And while Microsoft still dominates enterprise IT, true large‑scale AI deployment across big corporations is not expected until 2027–2028. That lag gives management time to improve Copilot and vertical AI solutions — including in high‑value areas like healthcare — but it also means investors may need to stomach several more quarters where costs rise faster than visible AI revenue.

How should investors read the 2030 Microsoft Forecast?

For long‑term, US‑based investors, the 2030 Microsoft Forecast is primarily about compounding. If Azure can sustain roughly 30–40% growth over the next few years and commercial cloud adoption continues to deepen, the base‑case trajectory toward the high‑$700s or low‑$800s by 2030 looks reasonable. The commercial AI RPO pipeline gives rare visibility, and Microsoft remains deeply embedded in corporate workflows from Office to security and developer tools.

Still, the bear case cannot be ignored. If macro headwinds slow enterprise cloud spending, if Azure growth decelerates meaningfully below the mid‑30s, or if CapEx keeps climbing without a matching increase in backlog, some models see Microsoft closer to the mid‑$400s over the next 12 months and around the high‑$500s by 2030. That would still be positive in absolute terms but underperforming the most bullish expectations and potentially lagging a resurgent NASDAQ 100 driven by AI hardware leaders like NVIDIA and electric‑vehicle and autonomy plays such as Tesla.

Related Coverage: AI capex and sector context

For a deeper dive into how Microsoft’s spending spree fits into the broader AI race, investors can review Microsoft AI Strategy Boom: $64B Capex Shock for Azure, which analyzes whether the company’s record data‑center outlays are a mispriced risk or the foundation for its next trillion dollars in market value. On the sector side, NVIDIA AI Infrastructure +2.2%: Cheap Valuation or AI Hype? explores whether NVIDIA’s data‑center dominance remains attractive at current prices, offering important context for comparing AI infrastructure plays in a diversified portfolio.

In conclusion, the current Microsoft Forecast paints a picture of a high‑quality franchise under short‑term pressure but with one of the strongest AI and cloud runways in Big Tech. The next few quarters, starting with FY2026 Q3 results on April 29, will be crucial in proving that Azure growth, Copilot adoption and AI backlog can justify today’s heavy investment. For long‑term investors willing to ride out volatility, Microsoft remains a cornerstone candidate in any AI‑tilted portfolio.