Is the aggressive MicroStrategy Capital Strategy a visionary Bitcoin play or a leveraged bet that could backfire in the next crypto downturn?

How is MicroStrategy funding its next BTC wave?

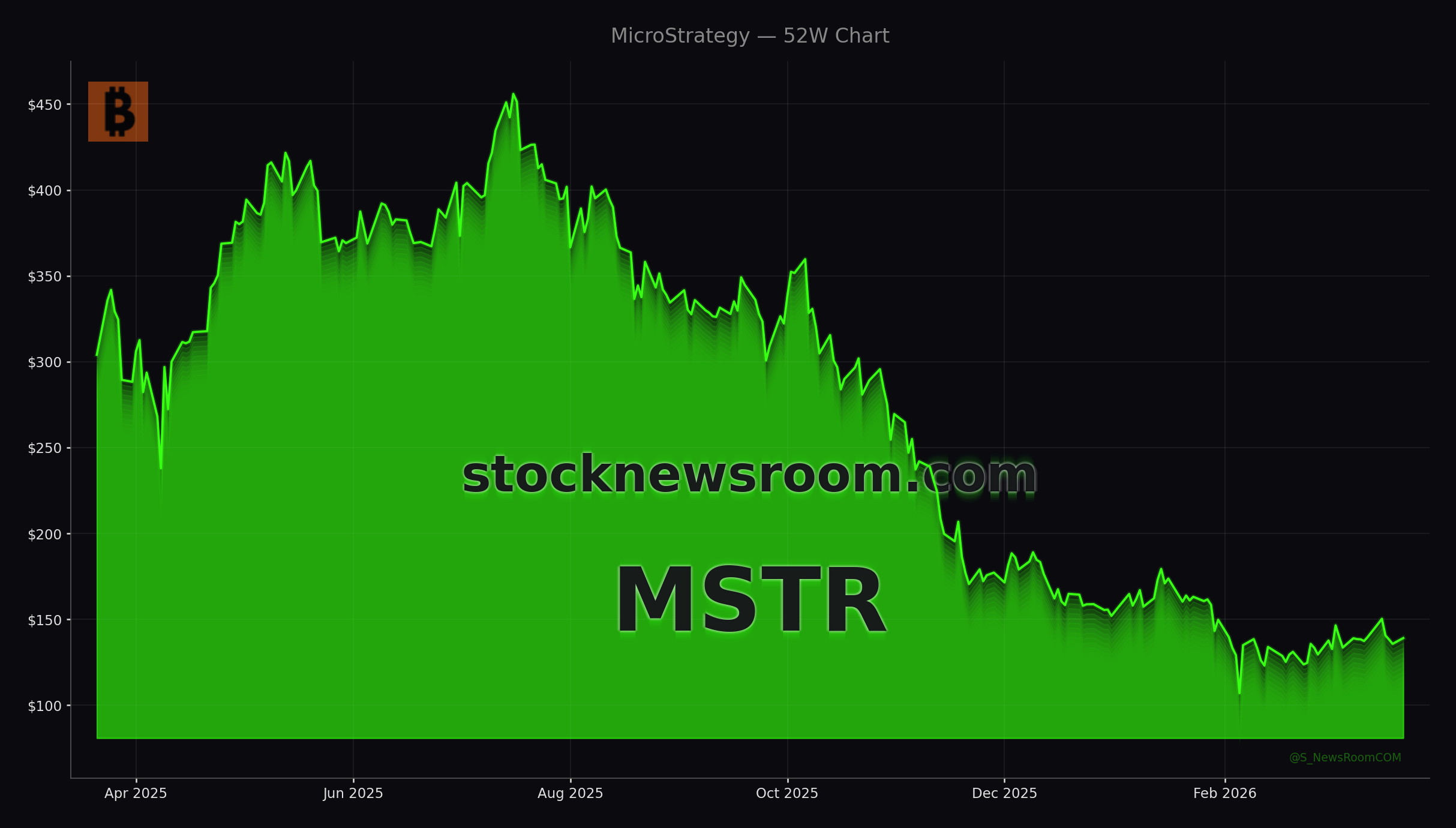

MicroStrategy Incorporated (MSTR) shares were recently trading around $137.18, up about 1.1% on the day, as Wall Street parsed a flurry of new filings detailing expanded capital-raising tools. Between March 16 and March 22, the company sold 509,111 shares of its Class A common stock through its ATM program, raising roughly $76.5 million in net proceeds. Those fresh dollars went almost one-for-one into Bitcoin: MicroStrategy acquired 1,031 BTC over the same period for about $76.6 million, at an average price near $74,326 per coin including fees.

That purchase lifts MicroStrategy’s total Bitcoin stack to roughly 762,099 BTC, with an aggregate cost of about $57.69 billion and an average purchase price around $75,694. With Bitcoin trading close to that blended cost basis, the balance sheet is effectively sitting near breakeven on a mark-to-market basis, underscoring just how tightly the MicroStrategy Capital Strategy is tied to crypto price swings.

Management continues to present this as a long-duration, even open-ended strategy: Bitcoin accumulated via equity and preferred offerings is intended to be held for at least a decade or longer, not traded quarter to quarter. That puts MSTR in a very different bucket from typical software peers like Apple or NVIDIA, whose capital allocation is dominated by buybacks and traditional R&D rather than leveraged cryptocurrency exposure.

What changed in MicroStrategy Capital Strategy today?

The company has significantly retooled its financing architecture. On March 23, MicroStrategy entered new addenda to its existing Omnibus Sales Agreement, enabling fresh ATM offerings for three security types: additional Class A common stock, additional Variable Rate Series A Perpetual Stretch Preferred Stock (STRC), and additional 8.00% Series A Perpetual Strike Preferred Stock (STRK). The new annex for common stock authorizes up to $21.0 billion in incremental ATM capacity, while a separate annex for STRC preferred also allows up to $21.0 billion in new issuance.

For STRK preferred, MicroStrategy terminated a prior, much larger prospectus that had allowed more than $20.3 billion of issuance and replaced it with a new program capped at $2.1 billion. As of March 20, STRK traded around $75.41 per share on the Nasdaq Global Select Market, while the company’s common stock last closed at $135.66, illustrating that investors are willing to fund the structure but at a meaningful yield — STRK carries an 8.0% coupon and a floating liquidation preference designed to track recent trading levels.

On the corporate governance side, MicroStrategy filed a Certificate of Increase to boost authorized STRC preferred shares from about 70.4 million to 282.6 million, while simultaneously filing a Certificate of Decrease to cut authorized STRK preferred shares from 269.8 million to roughly 40.3 million. That shift reinforces management’s current preference for the variable-rate STRC structure as a core tool in the broader MicroStrategy Capital Strategy, while keeping STRK as a more limited, yield-focused component.

How risky is this Bitcoin-centric funding model?

For U.S. investors, the key question is whether this layering of ATM equity, high-yield STRK, and variable-rate STRC is sustainable if Bitcoin turns sharply lower. Recent trading commentary has highlighted that MSTR often amplifies BTC’s moves in both directions, and some technical analysts warn that a deep crypto drawdown could stress the firm’s highly levered balance sheet. A recent pullback in the stock, with sharp single-day drops, shows how quickly sentiment can shift when Bitcoin cools after a run.

At the same time, bullish voices on Wall Street argue that MicroStrategy’s model resembles a long-dated call option on Bitcoin, funded by investors who are willing to accept equity and preferred issuance in exchange for upside participation. Commentators drawing retirement-planning comparisons suggest that if Bitcoin resumes a strong multi-year uptrend, the MicroStrategy Capital Strategy could turn the company into one of the most powerful BTC proxies in the NASDAQ universe, potentially rivaling the performance of high-beta innovators like Tesla.

Importantly, no major firm such as Goldman Sachs, Morgan Stanley, Citigroup, or RBC Capital has publicly abandoned coverage of MSTR; instead, research notes tend to emphasize extreme volatility, correlation to spot BTC, and the risk that further capital raises will dilute common shareholders if crypto enters a prolonged bear market.

What should U.S. portfolios watch next?

With the new ATM authorizations in place, investors should assume that MicroStrategy will periodically tap both common and preferred markets whenever liquidity and Bitcoin pricing look favorable. The firm has also expanded its roster of sales agents, adding Moelis & Company, A.G.P./Alliance Global Partners, and StoneX Financial alongside existing heavyweights such as Morgan Stanley & Co. and Barclays Capital. That broader syndicate increases placement flexibility and could lower execution risk for large block sales.

For portfolio managers benchmarking against the S&P 500 or NASDAQ, MSTR now behaves less like a traditional enterprise software name and more like a leveraged Bitcoin ETF with an active treasury desk. Position sizing, therefore, needs to reflect both crypto beta and the idiosyncratic risks of complex preferred structures. Some ETF providers have already woven MSTR into thematic products focused on digital assets, giving retail investors indirect exposure even if they never buy the stock outright.

Related Coverage

Investors looking for deeper context on leverage and timing can review earlier coverage of the company’s aggressive BTC posture in MicroStrategy Bitcoin Strategy: +1.7% Rally and Leverage Warning, which examines how prior capital raises amplified gains during Bitcoin rallies but also raised the stakes in potential downturns. For a broader macro view on the underlying asset, Bitcoin Market Analysis -2.3%: Geopolitics and ETF Shock explores how war headlines and ETF flows are reshaping crypto market structure — dynamics that feed directly into MicroStrategy’s balance-sheet risk.

In sum, the latest expansion of the MicroStrategy Capital Strategy confirms that the company intends to keep leaning on Wall Street to fund its massive Bitcoin bet. For U.S. investors, MSTR remains a high-volatility vehicle whose fortunes hinge far more on crypto cycles than on traditional software fundamentals. The next leg in Bitcoin’s trend — up or down — will be the decisive catalyst for whether this capital strategy delivers outsized gains or a painful dilution-driven reset.