Is Netflix dodging a costly mistake or missing a once-in-a-generation content grab by walking away from Warner Bros. Discovery?

Did markets just reject the Netflix Acquisition story?

When talk of a Netflix Acquisition of Warner Bros. Discovery first surfaced, sentiment was mixed but clearly high-stakes. The stock slid sharply once a potential all‑stock component and massive price tag – roughly $83 billion for Warner’s studio and streaming business – came into focus, echoing a familiar pattern: shareholders generally dislike equity-funded mega-deals that dilute existing holders. Investor Gary Black highlighted that point by comparing the reaction in Netflix to what could happen if SpaceX ever tried a similar equity-financed takeover of Tesla, arguing that buyers rarely want to fund a public offering only to see their stake diluted by an immediate acquisition.

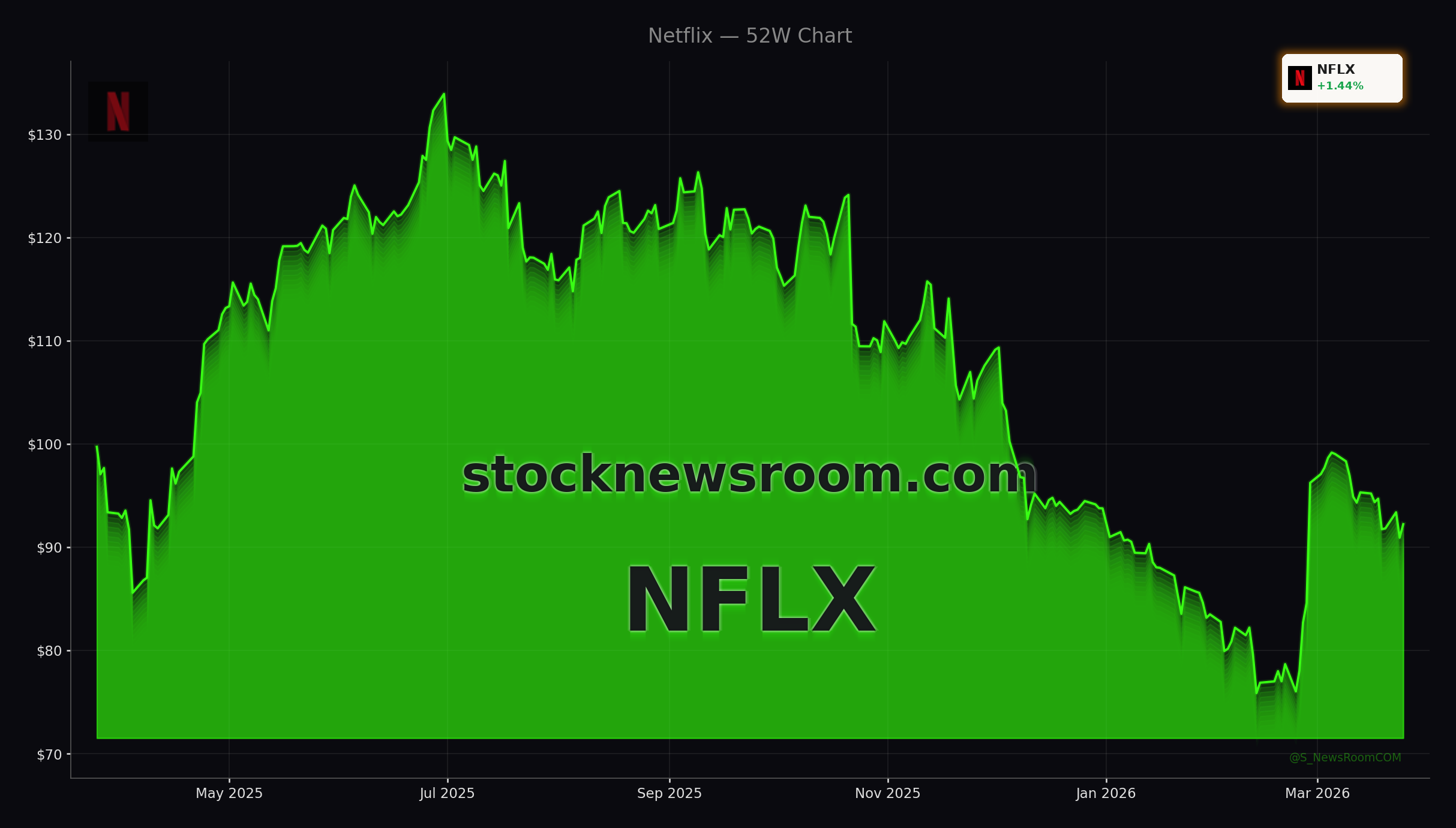

Ultimately, the market appeared to be signaling what many portfolio managers already know: streaming has become a cash-flow business, not a land‑grab at any price. With Netflix shares off their 52‑week high of $134.12 and now in the low $90s, investors clearly preferred the company’s existing growth and free‑cash‑flow story to a complicated integration of legacy media assets. The Netflix Acquisition narrative may have excited M&A bankers, but it did not excite long-only institutions tasked with compounding capital over years.

Why did Netflix walk from Warner Bros.?

Strategically, the Netflix Acquisition case was easy to make on paper. Owning HBO, Warner Bros. film and TV studios, and a century-deep content library could have fortified Netflix’s position against rivals like Apple TV+, Amazon Prime Video, and Disney+. Yet the logic broke down once a rival bidder – Paramount Skydance – reportedly pushed the price toward $110 billion, turning a strategic match into a classic bidding war. The higher the price went, the thinner the return on investment and the more flawless the integration would have needed to be just to break even.

Netflix has been clear that Warner was a “nice to have” at the right valuation, not a “must have” at any price. Walking away preserves balance sheet flexibility and avoids the distraction of merging vastly different cultures, tech stacks, and distribution models. Integrating HBO Max, theatrical distribution, complex licensing agreements, and studio operations could easily have consumed management attention for years – exactly when Netflix is gaining traction with its ad‑supported tier and live content experiments.

How does this reshape the Netflix Acquisition playbook?

The failure of the Netflix Acquisition bid sends a strong signal about how the company will approach M&A going forward. Rather than swinging for a single transformational deal, Netflix seems poised to favor targeted content and technology acquisitions, while leaning on its own scale to fund originals. Institutional investors appear to support that approach: multiple filings show firms like Perennial Advisors, Curated Wealth Partners and others increasing positions in NFLX, even as insiders have taken profits after a strong run.

Analysts broadly agree that Netflix remains a core growth name in the streaming and tech ecosystem. Across Wall Street, the stock carries a “Moderate Buy” consensus with an average price target of roughly $114, suggesting meaningful upside from current levels. Citigroup has been among the more constructive voices, previously flagging a $115 target that underscored confidence in subscriber momentum, advertising upside, and margin expansion without relying on a blockbuster Netflix Acquisition to drive the story.

Can Netflix grow without a mega-merger?

Recent operating trends suggest it can. Netflix has posted double‑digit revenue growth alongside rising free cash flow, helped by password‑sharing crackdowns, price increases, and stronger engagement around tentpole series and films. Its ad‑supported tier is scaling faster than many expected, creating a new monetization lever that legacy media peers are still trying to optimize.

On the content side, the company is pushing more aggressively into live and event programming. A high‑profile BTS concert livestream recently drew 18.4 million global viewers, showcasing the platform’s ability to turn cultural moments into global events in real time. In sports, Netflix has secured an exclusive Major League Baseball Opening Night game, a $60 million‑per‑year splash into live sports designed to bring in casual fans who might not pay for traditional cable bundles. These moves support the view that Netflix can keep expanding its addressable market organically, even without closing a giant Netflix Acquisition.

Marketing collaborations also illustrate how Netflix is monetizing IP in new ways. A fresh partnership with McDonald’s around the animated film “KPop Demon Hunters” will roll out themed meals, collectibles, and first‑access content, blending fast food, fandom, and streaming into a single global campaign. For investors, these initiatives hint at a flywheel where hit content can be leveraged across consumer brands, live events, and licensing – again, independent of any Warner‑scale takeover.

What does this mean versus rivals like Disney and NVIDIA?

For U.S. investors building diversified tech and media exposure, the end of the Netflix Acquisition saga helps clarify the competitive map. Disney is in the midst of its own strategic reset, including management changes and sharper cost discipline in Disney+, reflecting how tough the streaming economics have become. Netflix, by contrast, exits this episode with its balance sheet intact and its strategic focus sharpened, even if it ceded a rare asset in Warner.

In the broader NASDAQ and S&P 500 context, Netflix remains part of the growth‑oriented cohort that includes cloud, semiconductor, and AI beneficiaries like NVIDIA. While those hardware names are tied to the infrastructure behind AI and streaming, Netflix is one of the most visible ways to play the front‑end demand for digital entertainment and live events. If Paramount ultimately completes a Warner deal, it could become a stronger content rival, but it will also inherit integration challenges and higher leverage that Netflix has now decisively avoided.

Related Coverage

For a closer look at how Wall Street is valuing Netflix after the failed Warner bid, including Citigroup’s $115 price target and the role of institutional buying, see this detailed Netflix forecast analysis. To understand how competitive dynamics across the media and entertainment space are shifting, especially at legacy giants, it is also worth reading about the latest executive shake‑ups and investor reaction in Disney in this report on Disney’s management change and stock move.

This transaction was always a ‘nice to have’ at the right price, not a ‘must have’ at any price.— Netflix management statement on the abandoned Warner deal

The collapsed Netflix Acquisition of Warner Bros. Discovery ultimately underscores that the company is prioritizing disciplined capital allocation over empire‑building at any price. For shareholders, that restraint keeps dilution and integration risk in check while management doubles down on ads, live content, and global sports experiments as growth engines. The next catalysts will be subscriber trends, ad‑tier ramp, and any smaller bolt‑on deals, but for now Netflix looks set to pursue scale on its own terms rather than through a single make‑or‑break acquisition.