Can Netflix Advertising and AI-fueled content efficiency drive the next leg of growth even as subscriber momentum slows?

Is Netflix’s shift to ads finally paying off?

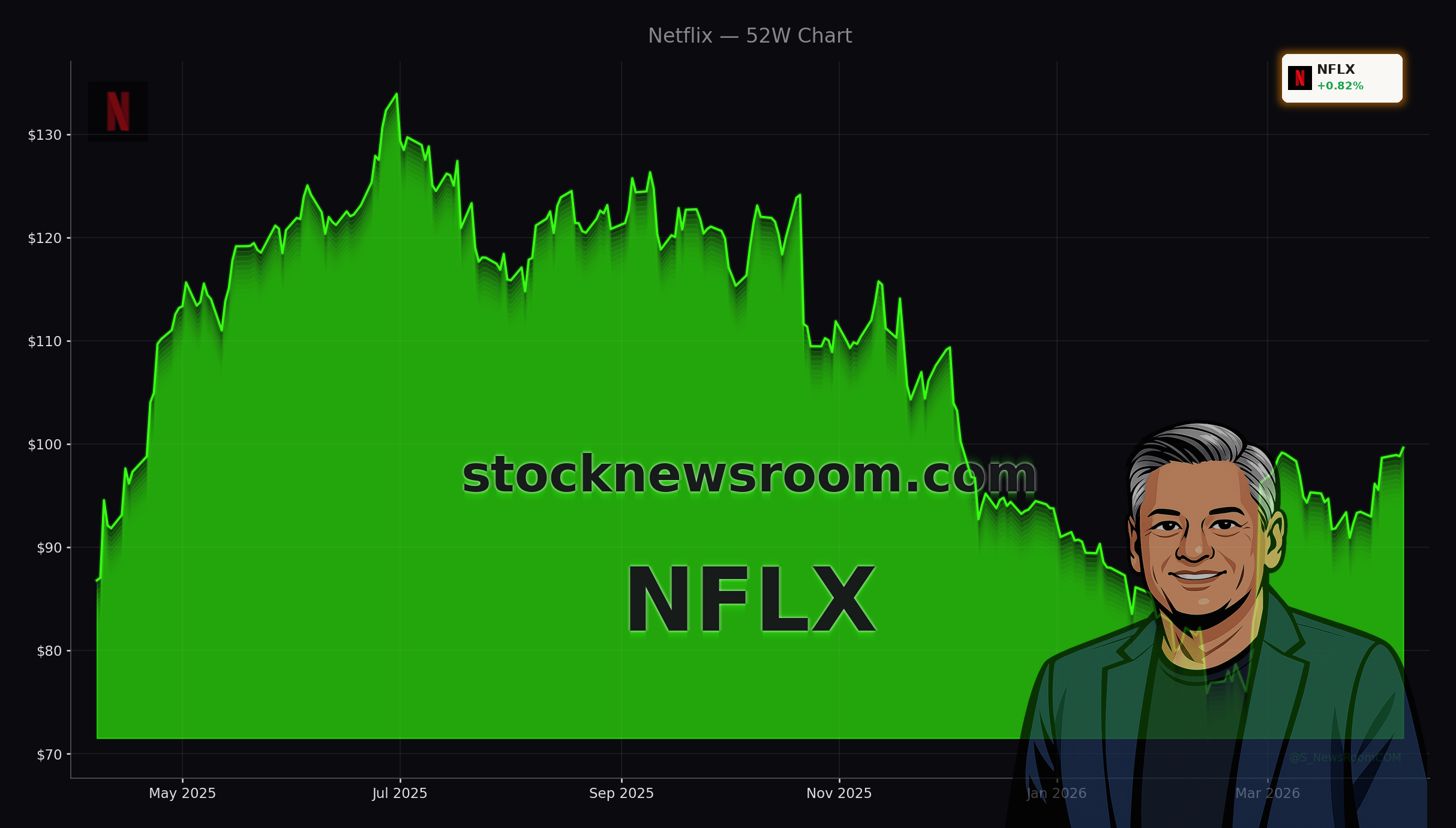

Netflix, Inc. (NFLX) heads into Q2 2026 with momentum in both subscribers and profitability, even as its share price remains roughly 25% below its 2025 peak near $132. The company ended 2025 with more than 325 million paying members and a record $45.2 billion in revenue, up about 16% year over year. Crucially for equity investors, operating margin has climbed into the 25%–30% range as management prioritizes monetization over pure subscriber growth.

Within that strategy, Netflix Advertising is the clear swing factor. The ad-supported tier, launched in 2022 at $8.99 per month, is dramatically cheaper than the Standard and Premium plans, but the economics improve as Netflix sells more targeted ad inventory against this growing audience. Ad revenue reached roughly $1.5 billion in 2025, more than 2.5 times the prior year, yet it still represents only a small slice of the overall top line. That under-penetration is exactly what bullish analysts are keying in on.

How big can Netflix Advertising become?

Netflix has rapidly built one of the largest premium ad-supported streaming audiences, with management indicating that ad-tier subscribers reached around 190 million by late 2025. If the company can steadily raise ad load, improve targeting, and push into higher-priced sponsorships, each ad-tier member could become more valuable than a traditional subscription-only user.

Beyond on-demand shows and movies, Netflix is leaning into live events that command premium ad rates. The platform now carries weekly WWE programming, marquee boxing cards, select Major League Baseball matchups, and exclusive rights to both NFL Christmas Day games through at least 2026. Management is also pursuing additional NFL inventory, which could further enhance the pricing power of Netflix Advertising as brands chase large, live audiences that are increasingly hard to reach on linear TV.

Wall Street expects ad revenue to more than double again in 2026, which would still leave ample runway relative to Netflix’s overall scale. If higher-margin advertising continues to outpace subscription growth, it could push earnings higher even if revenue growth moderates into the low-teens range over the next several years.

Where does AI fit into the Netflix story?

On the technology side, Netflix is accelerating its use of artificial intelligence to support content production and recommendation systems. The planned acquisition of InterPositive, an AI filmmaking specialist, for up to $600 million signals a willingness to embed AI deeper into the creative pipeline, from pre-production and visual effects to localization. Actor and director Ben Affleck has framed the deal as using AI as a tool for filmmakers rather than a replacement, a positioning that may help Netflix manage talent relations while still driving efficiency.

For investors, the AI angle is less about hype and more about cost discipline. Smarter production workflows and more accurate audience targeting can stretch each content dollar further, helping Netflix maintain its spending edge versus rivals like Disney and Warner Bros. Discovery without eroding margins. It also keeps the company in the broader AI conversation alongside heavyweights like NVIDIA and Apple, which many institutional investors view as core holdings in any tech-focused portfolio.

How are analysts valuing Netflix now?

After a volatile 2025 marked by a now-abandoned bid for Warner Bros. Discovery, sentiment toward Netflix on Wall Street has turned noticeably more constructive. Goldman Sachs recently upgraded the stock from “neutral” to “buy” and lifted its 12‑month price target to $120, citing attractive valuation and an expected acceleration in revenue driven by price hikes and advertising. Oppenheimer has reiterated its “Outperform” rating and raised its target to $135, pointing to Netflix’s industry‑low churn, pricing power, and a stronger content moat following the Warner Bros. Discovery–Paramount tie‑up.

At around $99, Netflix trades at roughly 40 times its 2025 earnings of $2.53 per share, below its five‑year average multiple. With consensus forecasts calling for EPS of $3.17 in 2026 and $3.84 in 2027, the forward P/E compresses into the low‑30s and then mid‑20s if the stock price doesn’t move. That dynamic means the share price would have to climb more than 50% by the end of 2027 just to keep the current valuation intact, underscoring how pivotal sustained growth in Netflix Advertising and margins will be.

What about kids, gaming and retention?

Beyond advertising, Netflix is investing in stickier family use cases to reduce churn and support pricing. The new “Netflix Playground” app offers ad‑free, age‑appropriate games for children eight and under, featuring characters like Peppa Pig and Sesame Street. The app is included with existing memberships, playable offline, and carries no in‑app purchases, addressing prior criticism that Netflix’s first gaming push was too hard to access. Reuters and Yahoo Finance both highlight Playground as part of a broader strategy to deepen family engagement and blunt competition from Disney+ in the kids segment.

By bundling gaming with the core subscription and keeping it ad‑free, Netflix reinforces its positioning as a premium, safe environment for younger viewers, while reserving monetization muscle for live events and mainstream entertainment through Netflix Advertising. For long‑term investors, this combination of high‑value ad inventory and low‑churn family accounts could be a powerful mix.

Related Coverage

For a deeper dive into how recent price increases intersect with the ad strategy, readers can look at Netflix Price Hike +2.8%: Surge That Tests Subscriber Loyalty. That analysis explores whether higher monthly fees and the growth of Netflix Advertising risk alienating subscribers or simply reflect the platform’s strengthened market position in global streaming.

Netflix Advertising now sits at the center of the company’s next growth chapter, supported by AI‑enabled content production, live sports, and new family‑focused initiatives like Playground. For U.S. investors, the setup is clear: if Netflix can keep ad revenue scaling faster than subscriptions while defending its premium valuation, the stock still has room to run within a diversified tech or communication‑services portfolio. The upcoming earnings reports and advertiser demand trends will show whether this revamped playbook can sustain Netflix’s comeback on the NASDAQ.