Can a bold $115 Wall Street target and heavy institutional buying reignite the Netflix Forecast after its recent pullback?

How does Citigroup shape the Netflix Forecast?

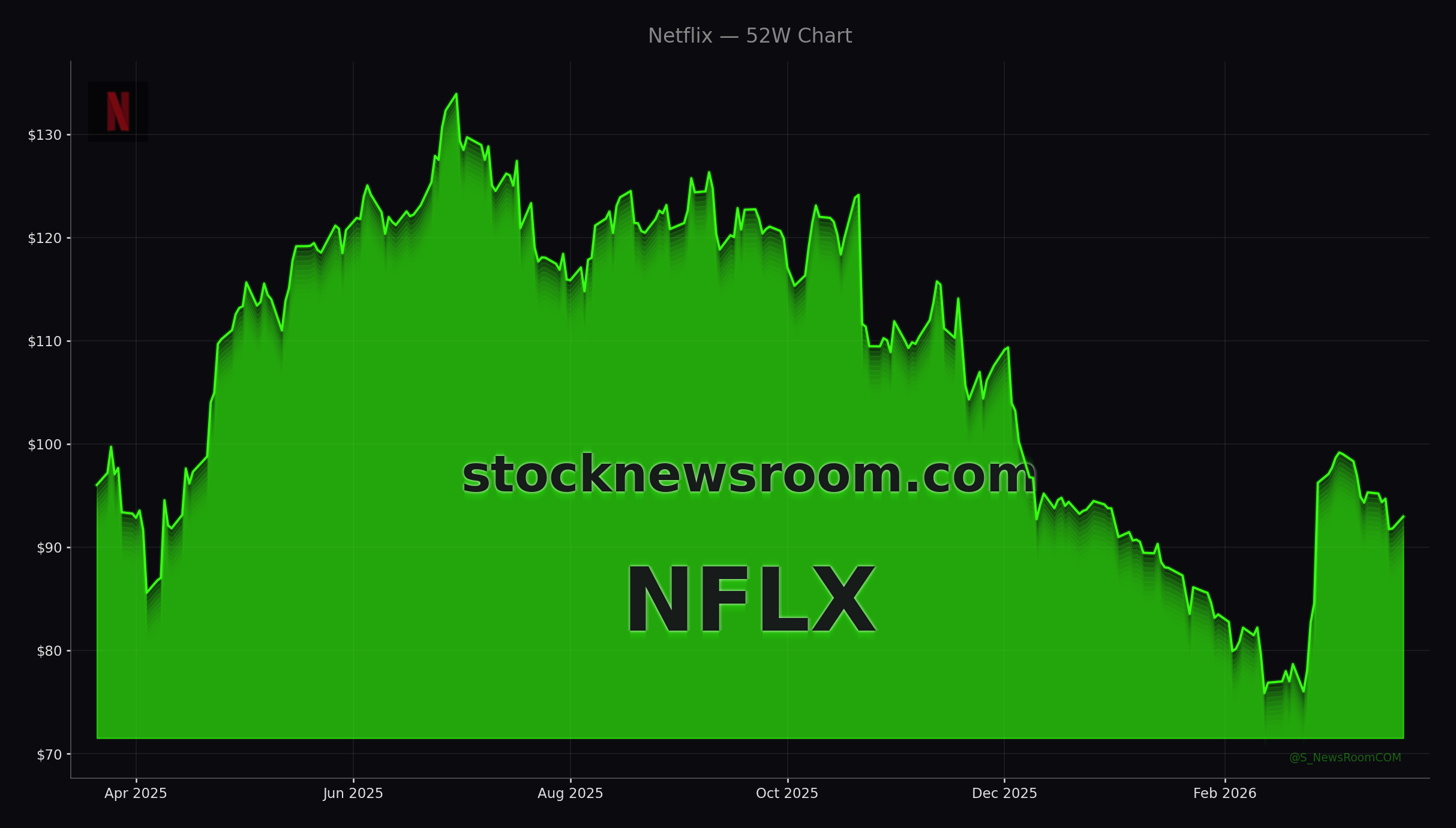

Citi analyst Jason Bazinet re-initiated coverage on Netflix, Inc. with a Buy rating and a $115 price target on March 18, giving bulls a clear reference point for the current Netflix Forecast. That implies upside of roughly 24% from Monday’s $93.03 quote, signaling that at least one major Wall Street house sees the recent pullback as an opportunity rather than the start of a prolonged downtrend.

The Citi call aligns with the broader analyst view. Across major brokerages, Netflix currently carries a “Moderate Buy” consensus, with an average target price clustered around $114–$115. While some firms have trimmed their targets on valuation and growth worries, the street is far from abandoning the name. Instead, the narrative is shifting toward whether Netflix can convert its scale into more disciplined, profitable growth, rather than simply chasing raw subscriber additions.

Intraday, the stock has been “having a good morning,” with traders noting that the price action looks similar to other large-cap tech names like Amazon and Apple as they try to reclaim pre-market highs. At $93, Netflix remains comfortably below the psychologically important $100 level, giving the Netflix Forecast room for a potential re-rating if fundamentals and sentiment improve in tandem.

What are institutions signaling on Netflix?

Beneath the headline volatility, institutional money has been quietly but aggressively accumulating Netflix. Multiple recent 13F filings show dramatic fourth-quarter position increases by wealth managers and asset allocators, reinforcing the constructive Netflix Forecast from a flow-of-funds perspective.

Wealth Enhancement Advisory Services boosted its Netflix stake by more than 800%, taking its holdings to 942,443 shares valued at roughly $85 million. Gradient Investments expanded its position by over 1,000% to about 325,918 shares, worth around $30.6 million. Additional buyers include Traveka Wealth, Wedmont Private Capital, Sound View Wealth Advisors, NorthCrest Asset Management, Legacy Private Trust, and Bennett Selby Investments, each reporting position increases often exceeding 800% quarter over quarter.

In aggregate, institutional investors now own roughly 81% of Netflix’s float. For long-term U.S. investors who track smart-money behavior, this wave of accumulation offers a counterweight to headline risk. It suggests that professional allocators continue to view Netflix as a core growth holding within the NASDAQ ecosystem alongside names like NVIDIA and Tesla, even if the stock has underperformed some mega-cap peers recently.

Does insider selling undermine the Netflix Forecast?

The major caveat to the bullish institutional picture is a notable pick-up in insider selling. Over the past quarter, insiders including co-founder Reed Hastings, CFO Spencer Neumann, and CEO Gregory Peters have collectively unloaded more than 1.5 million shares, worth roughly $137 million. Directors such as Bradford L. Smith have also trimmed positions.

While executives frequently sell for diversification or tax planning, the size and timing of these sales—against a backdrop of slowing subscriber growth and rising content budgets—have fueled skepticism. Some analysts worry that management may be signaling limited near-term upside, especially with the share price still below $100 and well off its historical peaks.

Even so, the market’s reaction has been measured rather than panicked. Netflix slightly beat Q4 earnings expectations and issued constructive Q1 2026 EPS guidance, supporting the case that the core business remains solid. The average Wall Street target near $114 reflects this balance: recognition of execution risk alongside confidence in Netflix’s ability to monetize its global scale, advertising initiatives, and live-event experiments.

How does Netflix stack up against rivals and the NASDAQ?

For U.S. investors benchmarking against the S&P 500 and NASDAQ-100, Netflix sits in an interesting middle ground. It lacks the AI-driven hyperscale premium enjoyed by NVIDIA but still commands a high multiple relative to traditional media players. Recent strategic moves, including dropping its pursuit of Warner Bros. Discovery assets and focusing on partnerships and live K-pop events, point toward a more asset-light model that could support margins over time.

On CNBC’s “Halftime Report” Final Trades segment, Bill Baruch highlighted Netflix as his pick, citing the Citi upgrade and potential for sentiment recovery. That television endorsement adds to the renewed attention from active traders, who are watching whether the stock can build a base in the $90s and eventually challenge the $100–$115 band targeted in the current Netflix Forecast.

Against a market where mega-cap tech dominates index performance, Netflix offers a different flavor of growth: subscription revenue, global content IP, and growing ad-supported tiers, rather than pure AI or hardware exposure like Apple or Tesla. That diversification angle may make Netflix attractive for investors seeking to balance their tech allocations without straying too far from the NASDAQ growth story.

Related Coverage

For a deeper dive into strategy and valuation, investors can review the recent analysis “Netflix Strategy -3.8%: Can Discipline Still Drive Growth?” which examines whether tighter capital allocation and franchise building can sustain the company’s premium multiple. The piece is available at Netflix Strategy -3.8%: Can Discipline Still Drive Growth? and offers additional context on how management’s long-term playbook feeds into the evolving Netflix Forecast.

Citigroup’s $115 price target, combined with broad institutional buying, shows many on Wall Street still see Netflix as a core long-term growth holding despite recent volatility.— Maik Kemper, Editor in Chief, stocknewsroom.com

Overall, the Netflix Forecast is cautiously optimistic: Citigroup’s $115 target and a wall of institutional buying suggest meaningful upside from current levels, while heavy insider selling and content-spend concerns argue for selectivity. For U.S. portfolios, Netflix remains a high-beta, high-conviction growth name whose next few quarters of execution will likely decide whether it rejoins the market’s leadership ranks or lags behind other NASDAQ giants.