Is the latest Netflix Price Hike a risky test of subscriber loyalty or the start of a powerful new cash machine phase?

Is Netflix pushing pricing power too far?

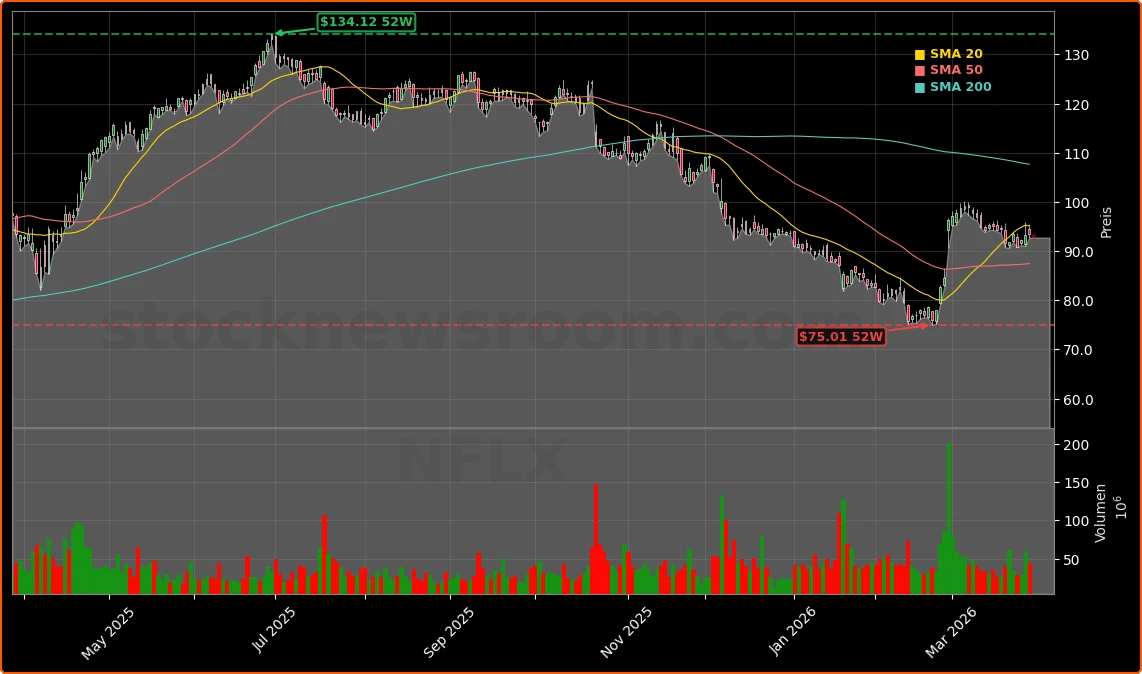

Netflix’s standard ad-free plan now costs $19.99 per month, up from $17.99, while premium jumps to $26.99 and the ad-supported tier to $8.99. The stealthy Netflix Price Hike — implemented via website changes and higher invoices, without a formal announcement — comes just over a year after the last increase, earlier than many analysts expected. Yet early trading action suggests investors approve: the stock edged higher after the news, even as the broader S&P 500 softened.

On the numbers, Netflix hardly looks desperate for cash. In 2025 the company generated roughly $9.46 billion in free cash flow on a robust 29.5% operating margin, while holding about $13 billion in current assets against $13.5 billion in long-term debt. A recently secured $2.8 billion breakup fee from Paramount Skydance further strengthens an already solid balance sheet.

How does Netflix stack up against rivals?

For U.S. investors, the key question is whether higher pricing opens the door for competitors such as Apple, Walt Disney and Warner Bros. Discovery to steal share by holding the line on subscription costs. Disney+, Paramount+ and HBO Max have all participated in the broader streaming inflation trend, but none has yet matched Netflix’s combination of scale, engagement and global reach. Meanwhile, Apple is leaning on Apple TV+ and its growing game portfolio to support a fast-expanding Services business, setting up a multi-front battle for consumer attention and wallet share.

Analysts at Jefferies highlighted the early U.S. price move as a potential upside driver to 2026 revenue guidance, while several Wall Street firms, including Goldman Sachs and Morgan Stanley, have recently reiterated bullish stances on the stock. Across the Street, targets cluster above the current $90s trading range, with MarketBeat data showing an average around $114 and a “Moderate Buy” consensus.

What will Netflix do with the extra cash?

Pricing is only one lever. In 2025, Netflix spent $9.1 billion on share buybacks, reduced debt by $1.8 billion, and poured $17.1 billion into new content, from prestige series to gaming experiments. Management has been clear that its priorities are sustaining revenue growth, expanding operating margins and growing free cash flow — exactly what the latest Netflix Price Hike supports.

With more than 325 million customers still paying and churn historically low after past increases, many analysts expect this move to flow through to margins more than it hurts subscriber counts. That dynamic is why some on Wall Street now view Netflix alongside megacap compounders like NVIDIA and Tesla: mature growth stories where incremental pricing power can significantly accelerate earnings without massive new user acquisition.

Related Coverage: For a deeper dive into how this Netflix Price Hike could impact long-term profitability, readers can explore our companion analysis “Netflix Price Hike Shock: Can Margins Boom From Here?”, which examines whether rising subscription rates can turbocharge margins without triggering damaging churn. The broader sector implications for streaming and digital entertainment are also discussed in “Netflix Price Hike Shock: Can Margins Boom From Here?”, putting the move in context with the evolving competitive landscape.

In sum, the latest Netflix Price Hike underscores a confident bet on pricing power and shareholder returns rather than raw subscriber growth. For investors, it reinforces the margin expansion story and adds another catalyst ahead of the April 16 Q1 report, where the impact on churn and guidance will be crucial. If subscriber losses remain contained, Netflix could solidify its position as one of the NASDAQ’s most reliable cash machines.