Can the latest Netflix Price Hike really turbocharge profits without triggering a subscriber backlash that derails the streaming giant’s growth story?

Does the Netflix Price Hike risk a churn shock?

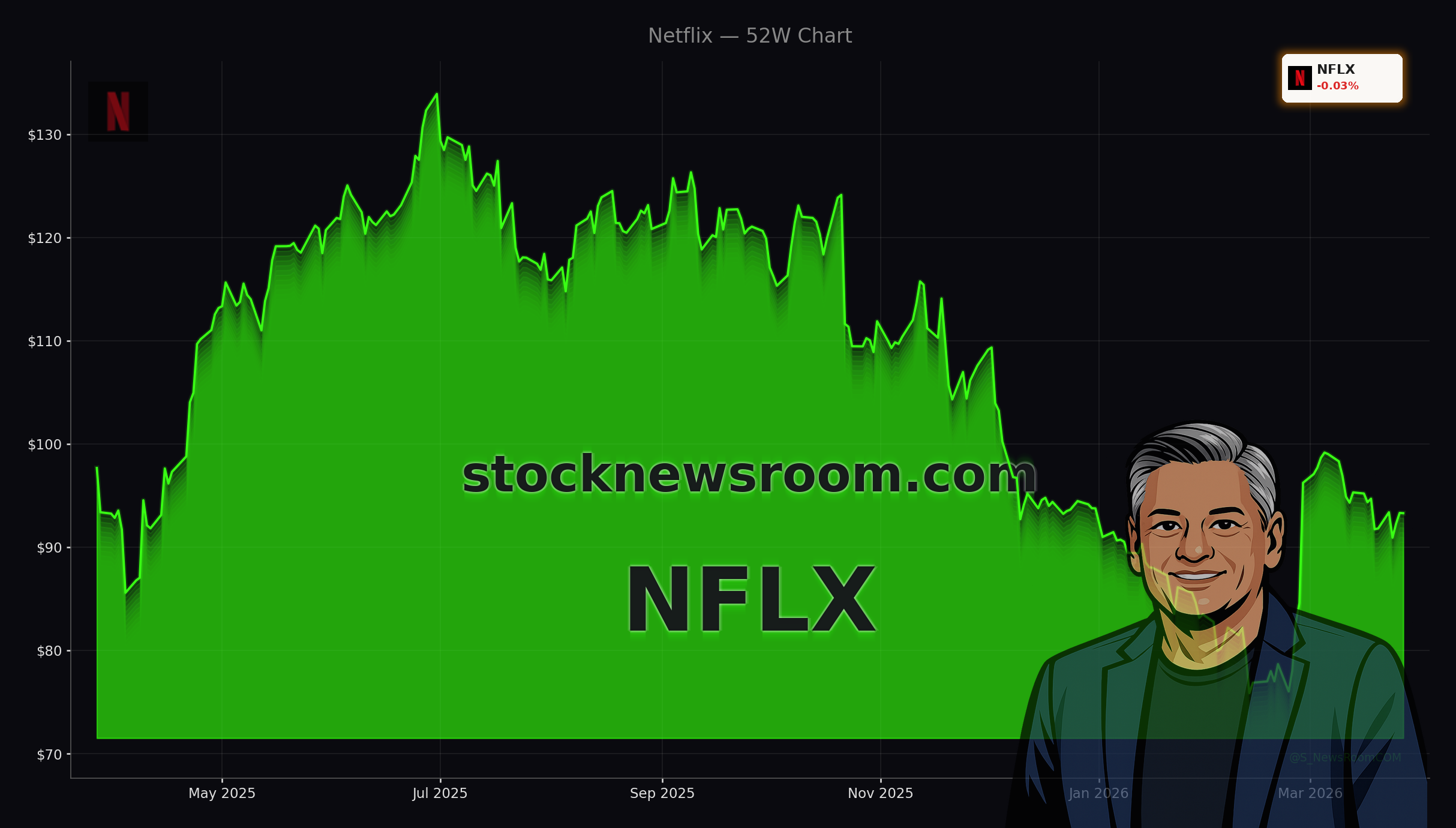

The new pricing pushes the ad-supported tier to $8.99 per month, the Standard plan to $19.99 and Premium to $26.99, with extra-member fees also up by $1. That translates to roughly an 11% average increase and follows the company’s decision to walk away from acquiring Warner Bros. Discovery, removing a contentious M&A overhang. Despite the move, the stock is only fractionally higher year over year and currently trades well below its 52-week high of $134.12, suggesting the earnings upside from this Netflix Price Hike is not fully priced in.

JPMorgan estimates the new structure could unlock about $1.7 billion in incremental annualized revenue with minimal churn, while Morningstar argues earlier-than-expected hikes are consistent with a strategy to maintain double-digit revenue growth in a maturing U.S. market. Analysts point to Netflix’s industry-low cancellation rates and strong engagement as buffers against a wave of cancellations.

What are analysts expecting from Netflix now?

Citigroup keeps a Buy rating with a $115 target, looking for a modest “beat and raise” when Netflix reports Q1 earnings on April 16, aided by higher prices and lower acquisition-related costs after abandoning the studio deal. Oppenheimer’s Jason Helfstein reiterated an Outperform rating and lifted his target to $135, highlighting the company’s ability to raise U.S. prices just 15 months after the last increase as proof of durable pricing power.

Evercore ISI and Bernstein also rate the shares Outperform, emphasizing growing ad revenue — already above $1.5 billion in 2025 — and operating margins around 30%. While some managers, including Cathie Wood at Ark Invest, have recently trimmed positions, institutional buying from large funds underscores continued confidence in the long-term streaming thesis versus megacap peers like Apple or diversified tech names such as NVIDIA.

How does this reshape the streaming landscape?

Netflix already commands roughly 9% of U.S. TV time and sits in a stronger financial position than many rivals, which are still bleeding cash on streaming. Its ability to push through a Netflix Price Hike contrasts with the more fragile models at legacy media players and even challenges consumer tolerance tested by other high-profile brands like Tesla. With over $20 billion earmarked for content and live events this year, the company is effectively asking customers to underwrite a bigger programming bet, while Wall Street anticipates expanding margins through scale.

Some critics, including Senator Elizabeth Warren, have blasted the timing after Netflix secured a multibillion-dollar breakup fee from its failed Warner Bros. pursuit. Yet most analysts expect churn from the Netflix Price Hike to remain contained as households continue to see the service as a relatively affordable entertainment staple, especially versus travel or live sports tickets.

Related coverage

For a deeper dive into whether richer plans can really fund the next wave of streaming hits, investors can explore Netflix Price Increase Shock: Can Costly Plans Fund a Content Boom?. That analysis looks at how much headroom Netflix may still have on pricing and how its strategy compares with other global streamers in the fight to own living-room screen time.

The Netflix Price Hike underlines how the company is shifting from pure subscriber growth to ARPU and margin expansion, a pivot Wall Street has long wanted to see. For U.S. investors, the key question is whether that pricing power can offset slowing net adds and rising content costs without eroding its competitive moat. The next earnings report will show whether this reset becomes a lasting tailwind for the stock or a first real test of subscribers’ loyalty at scale.