Is the latest Netflix Price Hike a smart monetization move or the moment subscribers and investors finally push back?

How aggressive is the Netflix Price Hike?

Netflix, Inc. has lifted monthly prices across all U.S. subscription tiers for the second time in under two years. The ad-supported plan rises by $1 to $8.99, the standard tier jumps $2 to $19.99, and the premium plan climbs $2 to $26.99. Extra members on ad-supported accounts now cost $6.99 per month, while ad-free add‑ons are $9.99, both up $1. Since October 2023, that translates into roughly 29% cumulative increases for the standard plan, nearly 29% for ad-supported, and more than 17% for premium.

While a dollar or two per month sounds modest, the percentage move is substantial, especially for price-sensitive households already managing higher rents, food costs, and gas prices. It is also a bold test of the lower-priced ad tier, which was designed as a safety valve to keep users inside the ecosystem when they trade down from premium or standard plans instead of canceling outright. By lifting prices across the board, Netflix is signaling strong confidence that churn will remain contained.

What does this mean for Netflix’s growth story?

The Netflix Price Hike comes against a backdrop of robust fundamentals. Full-year 2025 revenue reached about $45.2 billion, up nearly 16% year over year, while free cash flow surged roughly 37% to $9.5 billion. The company finished 2025 with more than 325 million global subscribers, up from around 300 million a year earlier, even after prior price increases and a crackdown on password sharing.

Management is guiding for $50.7 billion to $51.7 billion in 2026 revenue, with an operating margin near 31.5%. Advertising is the key swing factor: ad revenue more than doubled in 2025 to over $1.5 billion and is expected to roughly double again in 2026. Citigroup analysts argue that the new pricing will likely lead Netflix to raise its 2026 outlook, while JPMorgan estimates the higher subscription rates could add around $1.7 billion in annual revenue, much of which may already be embedded in current guidance. Oppenheimer’s Jason Helfstein has highlighted that the added cash helps support a roughly $20 billion 2026 content budget.

How does the Netflix Price Hike stack up against rivals?

From a U.S. consumer perspective, the ad-supported plan sits broadly in line with other major platforms, including offerings from Disney and Apple’s Apple TV+. Where Netflix stands out is the $26.99 premium tier, now one of the most expensive pure-streaming options on the market. That premium price tag is being justified by a heavier push into live events and sports — from NFL and WWE rights to a planned 2026 MLB Opening Day package — as well as experiments in live comedy and podcasts.

For U.S. investors, this makes Netflix look less like a high-growth speculative streamer and more like a recurring-revenue, pricing-power story akin to Apple’s services or even subscription models at Tesla and NVIDIA. Analysts at UBS have gone as far as naming Netflix a top pick, pointing to this blend of pricing power, ad growth, and disciplined capital allocation after walking away from a debt-heavy Warner Bros. asset deal.

What is Wall Street pricing in now?

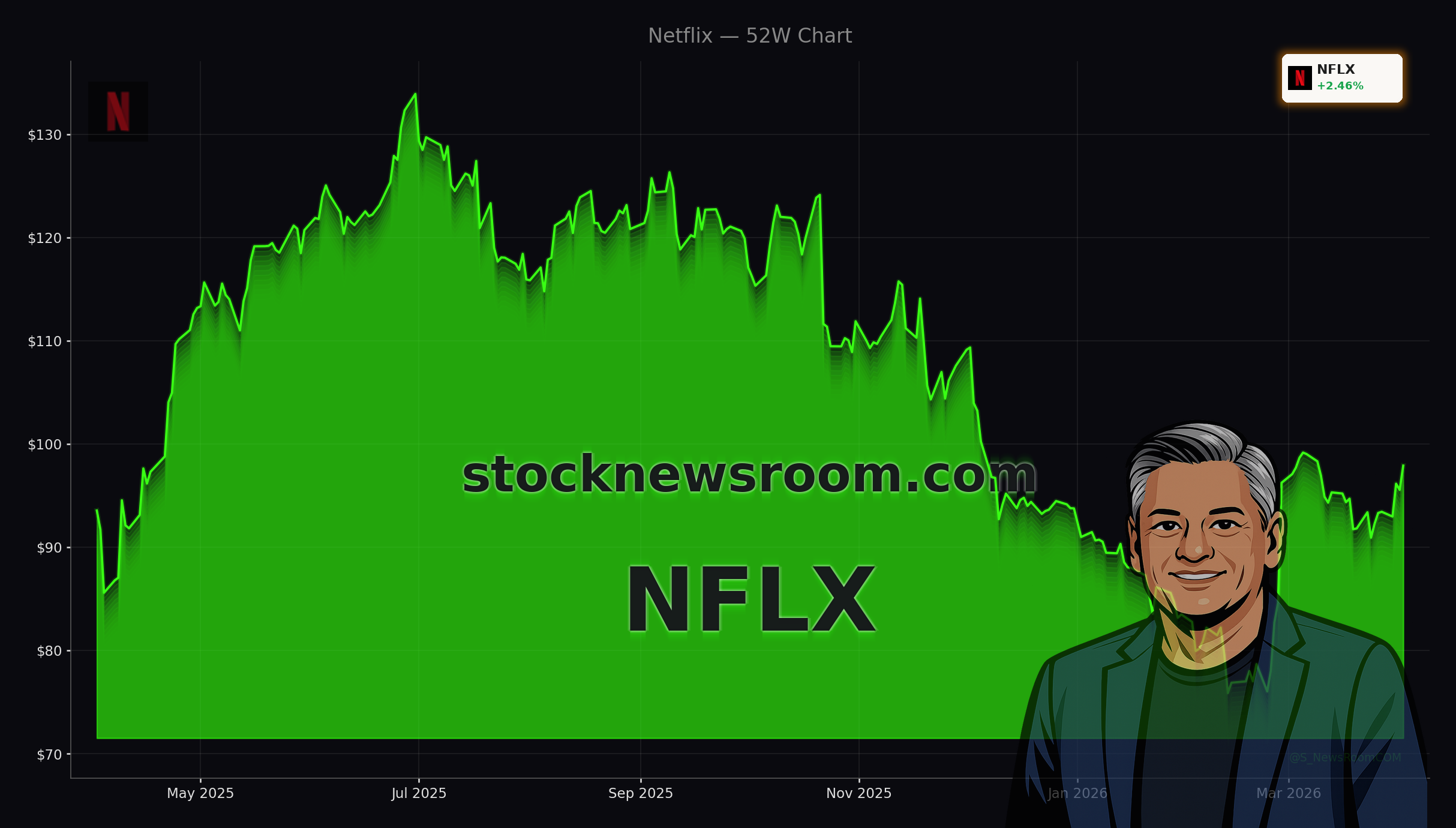

On Thursday, NFLX closed at $98.22, up 2.80% and comfortably between its 52-week low of $75.01 and its 52-week high of $134.12 — not near new highs, but outperforming a weak NASDAQ and S&P 500 so far in 2026. Of 51 analysts tracking the stock, 37 rate it a Buy, 13 a Hold, and just one a Sell. The average price target near $113 implies roughly 15%–20% upside from current levels, with Needham’s Laura Martin at $120 and some Seeking Alpha contributors arguing the shares could ultimately reach the $170 range if 2026 targets are met.

Institutional investors are leaning in. Hedge funds such as Paul Tudor Jones’s operation and D.E. Shaw have sharply increased their stakes, helping push institutional ownership to the mid‑80% range. At the same time, several top executives — including co‑CEOs Ted Sarandos and Greg Peters and CFO Spencer Neumann — have taken profits in the $80s and $90s, while founder Reed Hastings has been exercising options and selling shares as part of a long-standing pattern. The stock trades at about 38 times trailing earnings, a premium that leaves little room for execution errors if the Netflix Price Hike backfires and churn spikes.

Related Coverage: How do sports and ads fit in?

Investors trying to handicap the Netflix Price Hike should also watch how its expanding sports slate and ad business evolve. A recent deep dive on StockNewsroom asks whether live NFL games and other rights can reboot growth in both subscriptions and advertising; see this analysis of Netflix’s sports rights and potential $50 billion growth path for more detail. The article highlights how bundling sports into the core subscription may strengthen engagement and, in turn, support future price increases without triggering major churn.

Together with the new pricing structure, that strategy underscores Netflix’s shift from pure streaming disruptor to diversified entertainment platform. The upcoming Q1 2026 report on April 16 — where management will be judged against revenue guidance around $12.16 billion and EPS of $0.76 — will be the first major test of whether higher prices, richer content, and fast-growing ads can keep the flywheel spinning.

In the end, the Netflix Price Hike reinforces the company’s bet that its content moat and growing sports and ad ecosystems give it room to charge more without losing its place as a core household subscription. For investors, the stock looks like a high-quality, inflation-resilient growth name, albeit one priced for continued flawless execution. The next few quarters will show whether consumer resilience and ad momentum justify today’s multiple, but for long-term portfolios, Netflix remains a compelling candidate to hold through the next cycle of streaming consolidation.