Can expanding Netflix Sports Rights around live NFL games really reboot growth and its new ad business at the same time?

Will Netflix Sports Rights change the growth story?

Netflix, Inc. is in talks to expand its current two‑game NFL slate to a four‑game package, including the new Thanksgiving Eve matchup and a standalone international game early in the season. The company is already in the final year of its Christmas Day deal, for which it has been paying roughly $75 million per game. Doubling that inventory would further cement live football as a strategic pillar, not just a one‑off holiday experiment.

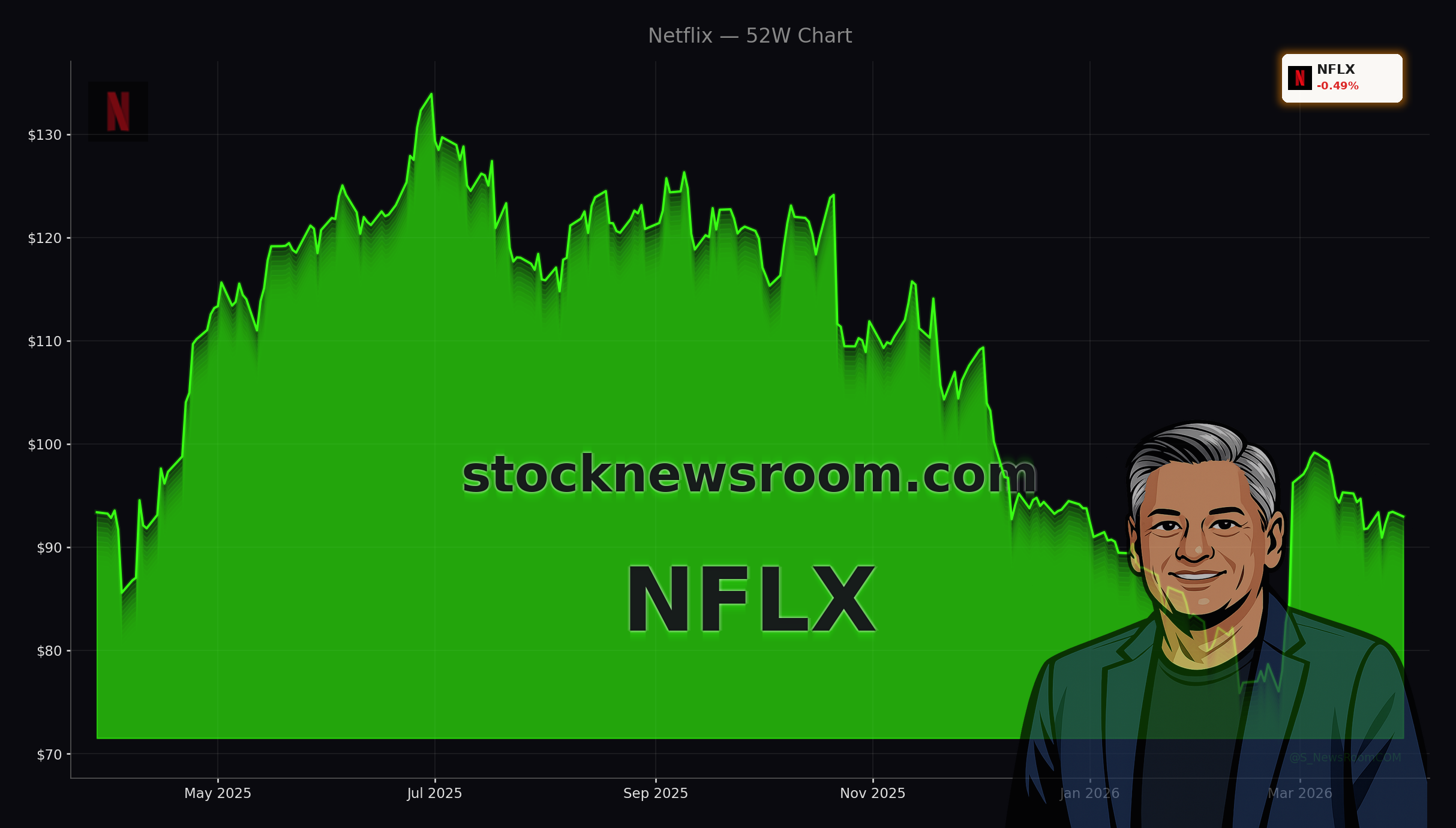

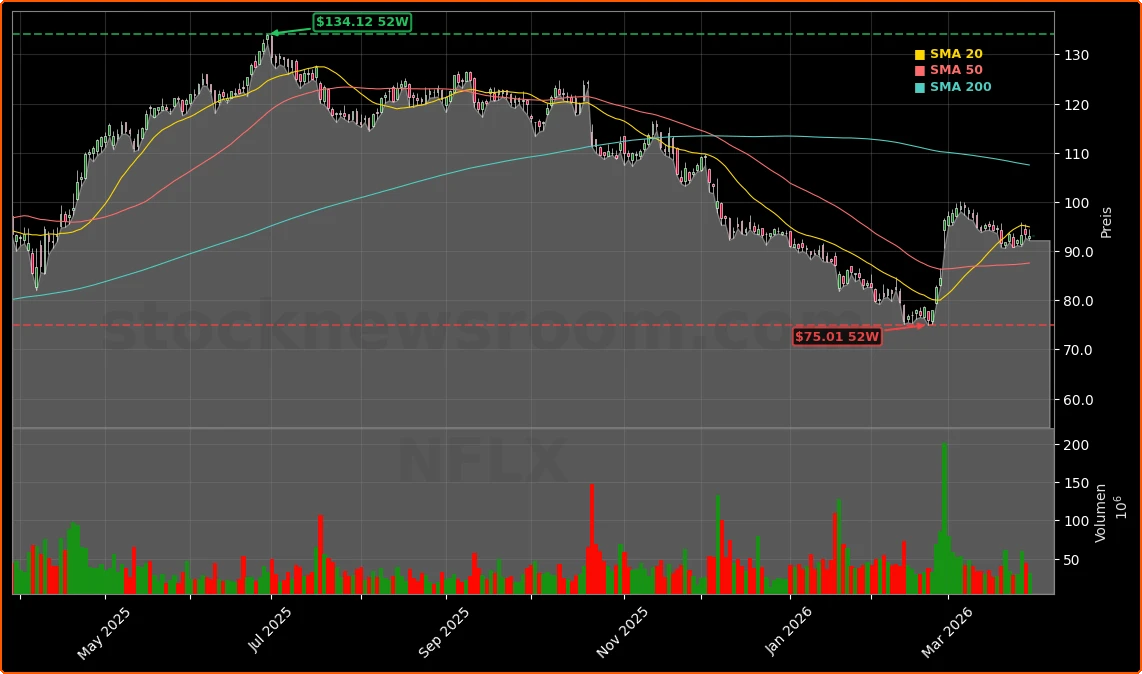

The stock, which peaked near $135 in mid‑2023, has corrected to about $92.97, down roughly one‑third from those highs, even as the broader NASDAQ and S&P 500 hover near record territory. Concerns about inflation, higher oil prices and potential churn from subscription price increases have weighed on sentiment. Technically, the shares look oversold, and several Wall Street firms still see upside; Needham, for example, recently reiterated a Buy rating with a $120 price target, pointing to pricing power, advertising upside and differentiated content.

Fundamentally, management is targeting revenue growth from about $33 billion in 2023 to more than $50 billion by 2026, with operating profit potentially more than doubling from $7 billion to roughly $16 billion. Free cash flow for the current year is estimated above $11 billion, supported by disciplined content spending and an additional $2.8 billion break‑up fee from a failed Warner Brothers deal. Against that backdrop, Netflix Sports Rights look less like a risky splurge and more like a targeted investment in appointment viewing that can support higher ad yields.

How do NFL games power Netflix advertising?

Sports and other live events are rapidly becoming the backbone of Netflix’s young but fast‑growing advertising business. Management and analysts expect ad revenue to roughly double from about $1.5 billion in 2025 to around $3 billion this year, aided by higher ad‑tier uptake, improved targeting and must‑watch events. A broader package of Netflix Sports Rights in the NFL would give advertisers premium inventory around Thanksgiving and the season kickoff—two of the most coveted slots on the U.S. media calendar.

Needham’s Laura Martin has argued that recent U.S. and Canada price hikes alone could drive roughly $1.7 billion in incremental revenue and boost North American growth by about 300 basis points in fiscal 2026. Combined with ad growth, this creates significant operating leverage: more revenue flowing across a largely fixed cost base, with sports serving as a high‑impact funnel into the ad tier. Competing platforms like Amazon’s Prime Video, which carries Thursday Night Football, and Google’s YouTube, which owns Sunday Ticket, have already demonstrated how live football can accelerate ad demand.

At the same time, Netflix faces rising competition from Roku on the ad‑supported side. Research from Zacks highlights Roku’s AI‑driven ad tools and more attractive valuation versus Netflix, underlining that Netflix Sports Rights alone will not guarantee dominance in ad‑supported streaming. Still, Netflix’s unmatched global scale, sophisticated recommendation engine and rising sports portfolio—from boxing and WWE to a fresh Major League Baseball package valued at roughly $50 million annually—position it as one of the best‑placed players to monetize live content at scale.

What does this mean for the stock and its rivals?

Institutional investors have been leaning into the weakness. Boston Common Asset Management recently boosted its stake to over 346,000 shares, while Private Advisory Group and AA Financial Advisors also sharply increased their positions, according to recent 13F filings. The stock remains a high‑conviction idea for many growth managers, with some price targets clustering in the $108–$120 range, implying roughly 15%–30% upside from current levels if execution remains on track.

On the competitor front, the NFL is taking a flexible approach to selling its reclaimed rights inventory, meaning those five available games could be split across multiple partners. Traditional broadcasters CBS, NBC and Fox, as well as Amazon, have expressed interest in additional games, and Google’s YouTube is also in the mix. That raises the possibility of a fragmented but more expensive rights landscape, similar to what investors have seen in the NBA’s latest media deals. For Netflix, discipline will be critical: overbidding could pressure margins, but walking away risks ceding ground in the most valuable sports league on U.S. television.

Investors should also track how Netflix Sports Rights intersect with the company’s broader ambitions in cloud gaming and interactive entertainment, areas where the likes of NVIDIA and Apple are investing heavily in underlying technology and ecosystems. While Netflix is still early in gaming, integrating sports‑themed experiences and cross‑promotions could further deepen engagement and reduce churn, especially among younger demographics.

Related Coverage

For a deeper dive into how subscription price increases might fuel a new cash‑generation phase, investors can read “Netflix Price Hike Shock: Is a Cash Machine Boom Ahead?”. The analysis explores whether recent price hikes are a risky test of subscriber loyalty or the beginning of a more durable margin expansion story. Taken together with the growing importance of Netflix Sports Rights, this perspective helps frame how pricing, ads and content investments could interact over the next few years.

Netflix Sports Rights are emerging as a central lever in the company’s shift toward live events and higher‑margin advertising revenue. For U.S. and global investors, the combination of NFL expansion, rapid ad growth and strong free cash flow suggests the recent share price pullback could be more of an opportunity than a warning sign. The next NFL deal cycle and April 16 earnings update will show how aggressively Netflix is prepared to lean into sports while still protecting profitability and long‑term shareholder value.