Is Netflix’s new strategy of capital discipline and franchise building enough to justify its rich valuation after the latest pullback?

Is Wall Street rewarding discipline at Netflix?

In early 2026, Netflix (NFLX) lost an $111 billion bidding war for Warner Bros. Discovery, yet the market reaction was counterintuitive: investors were relieved. The failed deal spared Netflix from taking on a complex integration and a large legacy debt load, while rival Paramount-Skydance and backer Larry Ellison stepped in instead. Netflix also received a $2.8 billion breakup payment, bolstering its already-strong balance sheet and preserving room for buybacks and selective acquisitions.

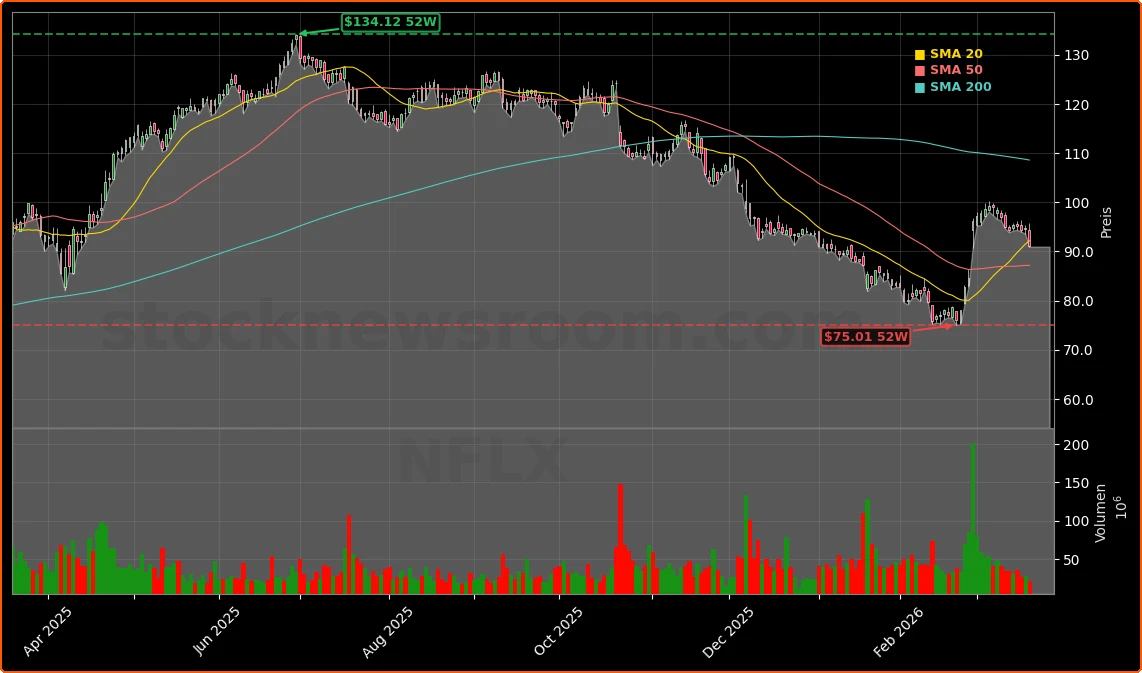

That decision fits a broader Netflix Strategy prioritizing capital discipline over empire building. The company generated roughly $9 billion in free cash flow last year with revenue growing about 17%, putting it firmly in the growth-and-quality camp of the S&P 500’s Communication Services sector. Yet at Thursday’s close of $91.11, the stock trades at about 37x forward earnings, leaving little margin for execution errors.

Technically, Netflix is trading about 1% above its 20-day simple moving average but still around 3% below its 100-day average, with shares closer to the middle of the 52-week range than to the highs after a rebound from late-February lows. An RSI near 60 and a slightly bearish MACD configuration suggest upside momentum is fading, even as the stock avoids overbought extremes. Key levels for traders include resistance near $100 and support around $75.

How is Netflix Strategy reshaping content?

On the content side, leadership is making a deliberate break from Hollywood’s reliance on sequels and reboots. Around half of Netflix’s recent film slate is built around new, original ideas, a push underscored by the 2026 film roadmap that heavily emphasizes fresh storytelling and theatrical-style comedies. Management is also leaning into genres that traditional studios have pulled back from, including comedies and young adult titles, aiming to capture viewers who feel under-served by legacy players.

At the same time, Netflix is planning a smaller number of large-scale “event films” each year designed to create global viewing moments. A new adaptation of “The Chronicles of Narnia” is being developed as one such tentpole, potentially anchoring both subscriber engagement and franchise spinoffs. This approach is meant to differentiate Netflix from rivals like Disney+ and Amazon Prime Video by balancing breadth of slate with a few high-impact projects.

The franchise-building logic is already visible. Animated hit “KPop Demon Hunters” has become Netflix’s most successful movie to date, and the company is now exploring a global concert tour around the film’s music, in negotiations with live promoters to bring its songs on stage worldwide. Netflix is layering on consumer products, licensing and potential sequels, making the title a template for how hits can be monetized far beyond a single streaming window.

What growth levers beyond streaming is Netflix pulling?

Beyond on-screen content, Netflix is testing multiple adjacency plays. It acquired a Ben Affleck–founded AI startup to help make films faster and cheaper, signaling that cost efficiency and production throughput are becoming strategic levers. The company is also experimenting with live sports, gaming and physical venues tied to its franchises, all designed to deepen fan engagement and create incremental revenue streams.

Live-action series like the newly announced “Scooby-Doo” reimagining, produced with Warner Bros. Television, highlight how Netflix can still partner with legacy studios without owning them. The show, which explores the origin story of Mystery Inc., fits the franchise-centric thrust and could feed into licensing, events and spin-offs if it lands with younger audiences.

Institutional investors are taking notice. Jacobs & Co. CA recently boosted its Netflix stake by more than 68,000%, buying over 138,000 additional shares to make the stock a meaningful part of its portfolio, even as company insiders sold around 1.5 million shares over recent months. That split between insider selling and institutional accumulation underscores the debate over how much upside remains at today’s multiple.

How are analysts valuing Netflix vs. mega-cap peers?

On Wall Street, sentiment skews constructive but cautious. Citigroup has a Buy rating and a $115 price target, while CFRA recently upgraded Netflix to Buy with a similar $115 target. Wells Fargo sits in the middle with an Equal-Weight rating and a $105 target. Across coverage, the consensus clusters around a Buy recommendation and an average target near $114, implying meaningful upside from current levels if growth holds.

With a P/E of roughly 37.4x, Netflix trades at a premium to many Communication Services peers, though still below high-flying names such as NVIDIA in the Information Technology sector. Compared to consumer-facing giants like Apple and Tesla, Netflix is seen less as a hardware or auto cyclical story and more as a recurring-revenue platform akin to Alphabet’s YouTube, with pricing power and global scale as key drivers.

Factor-based rankings reflect this mix. Momentum screens are weak, highlighting the recent pullback and difficulty sustaining breakouts, while quality and growth scores are strong, supported by rising free cash flow, double-digit revenue expansion and a tightening content focus. Value metrics remain stretched, making the upcoming April 16 earnings report – with consensus calling for EPS of $0.76 on $12.17 billion in revenue – a key test of whether guidance can catch up to expectations.

Related Coverage: For more context on how the abandoned Warner Bros. Discovery pursuit changed investor sentiment, readers can revisit our analysis in “Netflix Acquisition Exit: Why Walking Away Fuels a Rally”. That piece explores why Wall Street effectively rewarded management for stepping back from a mega-deal and refocusing on organic growth and returns of capital.

Ultimately, the Netflix Strategy now hinges on making fewer, bigger bets on original content, expanding winning franchises into live and physical experiences, and using AI and data to improve both costs and hit rates. For investors, the combination of robust free cash flow, disciplined deal-making and strong analyst support keeps Netflix a core growth name in the S&P 500, even if the stock’s premium valuation and soft technicals argue for selectivity on entry points. The next earnings update and execution on marquee projects like “KPop Demon Hunters” and “Narnia” will show whether this strategy can reignite momentum and sustain long-term outperformance.