Can the revamped Netflix Strategy of bigger bets, ads and new products justify the latest rally and reset the growth story?

Is Netflix Strategy Now Built on Quality Over Quantity?

Netflix, Inc. (NFLX) has quietly executed a major pivot: fewer but bigger bets in content, backed by price hikes and disciplined capital allocation. Benchmark analyst Daniel Kurnos describes the new Netflix Strategy as “quality over quantity,” replacing the old mantra of flooding the platform with volume. That approach is costlier, but he models mid‑teens revenue growth over the medium term and is not overly worried about churn from higher subscription prices.

Engagement sits at the center of this shift. U.S. users now spend roughly two hours per day on the service on average, but Netflix’s share of total streaming viewing has faced pressure even as its share of overall TV time inches higher. UBS points to the 2026 slate—new seasons of “Bridgerton” and “Night Agent,” a growing film pipeline, live events and video games—as key tests of whether premium content can pull more viewing time back from rivals like Disney and Amazon. A stronger engagement profile would underpin pricing power and support the valuation multiple.

How Did Walking Away from Warner Change the Story?

Earlier this year, Netflix stunned markets with an all‑cash bid for Warner Bros. Discovery that implied more than $40 billion in financing needs and an enterprise value near $83 billion. The stock quickly sold off to about $77 in February as investors priced in a more leveraged balance sheet and hefty integration risk. When Paramount‑Skydance raised its competing offer and pushed the valuation toward $110 billion, Netflix refused to chase the deal.

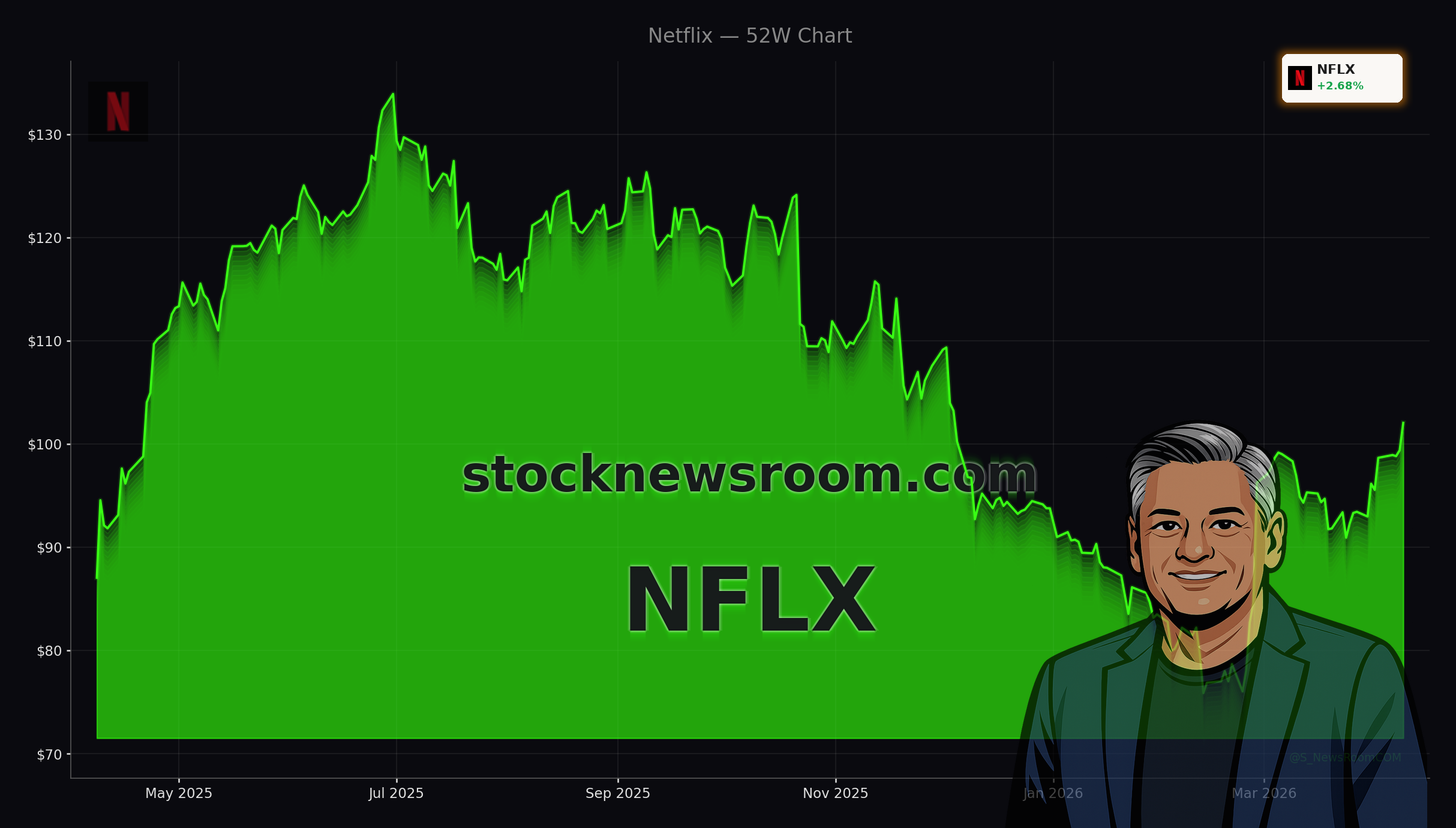

By stepping back, Netflix collected a $2.8 billion breakup fee and removed a major overhang. Co‑CEO Ted Sarandos has since reiterated that the company prefers “building rather than buying,” effectively doubling down on an organic Netflix Strategy instead of transformational M&A. With the Warner question resolved, the narrative has shifted back to fundamentals: subscriber growth, margin expansion and free‑cash‑flow generation without a balance‑sheet shock. The stock has rebounded from the lows and now trades about 26% below its 52‑week high, leaving room if sentiment continues to heal.

Can Premium Content and Ads Drive the Next Phase?

Financially, the core engine remains healthy. Q4 2025 revenue rose 17.6% year over year to $12.05 billion, while full‑year free cash flow jumped 36.7% to $9.46 billion. Ad‑supported plans are becoming a meaningful pillar of the Netflix Strategy: advertising revenue more than doubled to over $1.5 billion in 2025 and is expected to roughly double again in 2026. Goldman Sachs recently upgraded the stock to Buy with a $120 price target, citing attractive valuation, accelerating revenue from price hikes and ads, and the potential for renewed capital returns.

Morgan Stanley is similarly constructive. Analyst Sean Diffley raised his price target to $115 and kept an Overweight rating, arguing that easing concerns around engagement and margins make NFLX “an attractive entry point” ahead of earnings. He models steady double‑digit revenue growth, around 20% annual growth in earnings and free cash flow, and a path toward 40% EBIT margins by 2030. Meanwhile, BMO Capital reiterated a Buy with a more aggressive $135 target, placing Netflix among its top picks in communication services.

How Do New Products Like Playground Fit the Netflix Strategy?

Beyond video and ads, Netflix is using new products to deepen its ecosystem, particularly with families. The company just launched “Netflix Playground,” a standalone mobile app for children eight and under that offers ad‑free games tied to brands like Peppa Pig and Sesame Street. The app is bundled at no extra cost, supports offline play and is rolling out globally through late April.

This move extends the Netflix Strategy into interactive entertainment, reinforcing retention among households that might otherwise rotate between streaming services. It also complements the existing push into gaming for adults and teens, building another layer of engagement that can support both premium and ad‑supported tiers. For U.S. investors, the expansion echoes how Apple and NVIDIA use adjacent services and ecosystems to lift lifetime customer value rather than competing only on headline price.

What Are Analysts Watching into Q1 Earnings?

Wall Street expects Netflix’s April 16 report to be a key catalyst. Prediction markets assign a high probability of an EPS beat versus guidance of $0.76 diluted EPS, and 51 covering analysts skew overwhelmingly bullish: 37 rate the stock Buy or Strong Buy, 13 Hold and just 1 Sell. Jefferies, for example, maintains a Buy rating and anticipates that Netflix will raise its 2026 revenue and operating‑margin guidance on the back of price increases and scaling ads.

Still, the recovery is not risk‑free. Investors are monitoring slowing growth in streaming share, roughly $141 million of insider selling over the past 90 days and an Italian court ruling related to pricing for 5.4 million users. Any stumble in ad growth, content performance or engagement could stall the rally, especially with the stock trading at about 31x forward earnings versus the broader S&P 500. For now, NFLX is up modestly year to date, outperforming a slightly negative S&P 500 and regaining credibility as a core growth holding alongside names like Tesla in many U.S. portfolios.

Related Coverage

For a deeper dive into how advertising fits into the broader Netflix Strategy, readers can explore “Netflix Advertising Boom: Can Record Growth Last for NFLX?”, which examines whether ad tiers and AI‑driven content efficiency can sustain growth even if subscriber additions slow. The piece also discusses how competitive dynamics in streaming could influence NFLX’s long‑term margin profile.

Investors comparing Netflix’s quality‑over‑quantity approach with more aggressive cost cutting at rivals should also read “Disney Layoffs Cut 1,000 Jobs as DIS Stock Surges 3.5%”. That article looks at how Disney’s restructuring and layoffs are reshaping its streaming and studio operations, providing useful context for evaluating different entertainment strategies on Wall Street.

Netflix’s shift from chasing scale at any cost to focusing on premium, monetizable engagement is exactly what long-term shareholders wanted to see.— Sean Diffley, Morgan Stanley analyst

The evolving Netflix Strategy now centers on premium content, ad‑supported growth and targeted product bets like Playground, backed by a cleaner balance sheet after the scrapped Warner deal. For U.S. investors, consensus Buy ratings and rising price targets from firms such as Goldman Sachs, Morgan Stanley and BMO suggest the stock could still offer upside if engagement and margins track expectations. The upcoming Q1 earnings report will be the next test of whether this strategy can translate into sustained outperformance against the NASDAQ and the broader S&P 500.