Can NVIDIA AI Growth keep powering trillion-dollar forecasts while the stock still trades at a market-like valuation multiple?

How is NVIDIA moving the broader market?

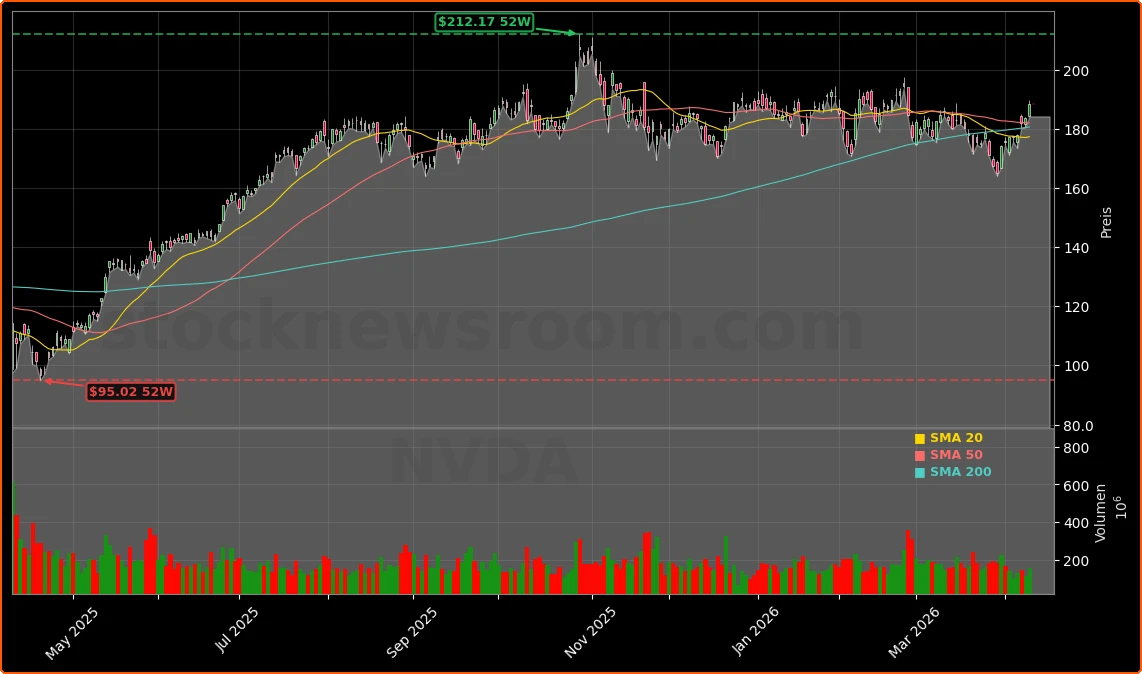

Tech once again did the heavy lifting for the S&P 500 and Nasdaq this week, and NVIDIA sat right in the middle of that move. The stock has now logged eight consecutive up sessions, its longest winning streak since November 2023, adding roughly 14% over that stretch. Even so, NVDA remains about 11% below its 52‑week high of $212.19 and is only modestly positive year to date, while the Nasdaq Composite is still down more than 5% in 2026 amid a rotation out of mega‑cap tech.

At Friday’s regular close, NVDA finished at $188.63, up 2.55% on the day, before slipping slightly to $188.37 in after‑hours trading. That puts the stock on a trailing price‑to‑earnings ratio near 38.5x, but on some forward estimates the multiple compresses toward the low‑20s as analysts bake in another year of outsized NVIDIA AI Growth. For a company expected to grow revenue at 70%‑plus this year and around 30% in 2027, that valuation looks far from bubble territory when compared with high‑growth software names or even peers like Advanced Micro Devices (AMD), which trades near 88x forward earnings.

What is driving NVIDIA AI Growth right now?

The latest leg of NVIDIA AI Growth is rooted firmly in the supply chain. Taiwan Semiconductor Manufacturing reported record preliminary Q1 revenue of about $35.6 billion, up 35% year over year, citing red‑hot demand for advanced AI chips at 3‑nanometer and 2‑nanometer nodes. NVIDIA has now overtaken Apple as TSMC’s largest customer, accounting for roughly 22% of the foundry’s revenue, underscoring just how central its accelerators have become to AI data centers globally.

On NVIDIA’s side, fiscal 2026 revenue surged 65% to $215.9 billion, with its Data Center segment alone climbing 68% to $193.7 billion. In the most recent quarter, revenue jumped 73% year over year, and management guided for about 77% growth in Q1 fiscal 2027. Wall Street consensus is even more aggressive for Q2, with some estimates pointing to 85% revenue growth as hyperscalers like Amazon, Meta Platforms, Alphabet and Microsoft ramp capital spending on AI clusters.

Partnerships are extending NVIDIA AI Growth beyond traditional cloud data centers. Cadence Design Systems expanded its collaboration to deliver agentic and physical AI‑accelerated tools optimized for Grace CPUs and Blackwell GPUs, already in use by industrial names like Honda and Micron. Power and optics suppliers such as Coherent are rolling out new high‑efficiency components under multi‑year agreements with NVIDIA to support ever larger AI data‑center builds.

Is the valuation still attractive for U.S. investors?

The remarkable twist in the NVIDIA AI Growth story is that earnings are accelerating faster than the share price. Multiple independent analyses now peg NVDA’s forward P/E near 21–22x, almost in line with the S&P 500’s roughly 20x despite radically different growth trajectories. By comparison, infrastructure monopolies like VeriSign trade around 27–28x forward earnings with far lower growth, and chip‑ecosystem backbone Taiwan Semiconductor commands roughly 35x earnings.

Major Wall Street houses remain broadly positive. Goldman Sachs has repeatedly highlighted NVIDIA as a core AI infrastructure holding for large‑cap growth portfolios, while Morgan Stanley continues to emphasize the durability of hyperscaler capex through at least 2030. Citi analysts have pointed to Blackwell and next‑gen Vera Rubin systems as the key catalysts behind the company’s forecast of $1 trillion in AI system sales across 2026–2027, arguing that consensus estimates may still be too conservative if agentic and physical AI demand scales as expected.

At the same time, risk is not absent. Investors are increasingly debating whether AI infrastructure spending, pegged at roughly $700 billion this year across the five largest hyperscalers, is approaching cyclical peak levels. Competitors are pushing alternatives: AMD is gaining share with ROCm and new GPU wins, while hyperscalers are designing custom ASICs and TPUs with partners like Broadcom and Marvell. In autos, Nio’s shift to its in‑house Shenji NX9031 chip for its L90 SUV underlines how some OEMs are weaning themselves off NVIDIA’s Orin platforms.

Can NVIDIA AI Growth extend beyond data centers?

The investment debate increasingly sits on whether NVIDIA AI Growth can broaden into new end‑markets fast enough to offset any eventual slowdown in cloud capex. Management is betting heavily on “physical AI” – AI‑enabled robots, autonomous machines and edge devices – and positions the company as the “brain” of emerging humanoid robotics platforms. The constraint for now is not demand but supply: high‑bandwidth memory and advanced packaging capacity are tight, and even major memory vendors like Micron are racing to catch up.

Still, the ecosystem around NVIDIA keeps deepening. Electronic design automation leaders like Synopsys and Cadence are building agentic AI workflows on top of Grace and Blackwell. Manufacturing and power‑electronics specialists such as Flex and Coherent are co‑developing racks and power infrastructure tailored to NVIDIA reference designs, enhancing lock‑in. Meanwhile, passive investors continue to accumulate NVDA through broad ETFs like Schwab’s SCHX and State Street’s SPGM, where the stock sits alongside fellow mega‑caps in top holdings, embedding NVIDIA AI Growth directly into thousands of U.S. retirement portfolios.

Related Coverage

For a deeper dive into how NVIDIA’s data‑center dominance underpins its long‑term narrative, our recent piece “NVIDIA AI Strategy +2.6%: Can the Data Center Boom Last?” analyzes whether hyperscaler spending and regulatory pressures can sustain trillion‑dollar ambitions. Investors interested in the broader AI ecosystem and political risk should also read “Palantir Military AI -1.9%: Trump Shock and ESG Warning”, which looks at how defense‑oriented AI players face valuation, ESG and policy headwinds that differ from NVIDIA’s infrastructure‑driven story.

In the end, NVIDIA AI Growth rests on a simple equation: earnings are compounding faster than sentiment, leaving valuation multiples well below where a textbook AI bubble would suggest. For American investors, that makes NVDA a high‑beta way to own the AI build‑out with a surprisingly reasonable price tag. The next few quarters – especially management’s updates on Blackwell, Vera Rubin and China demand – will show whether this NVIDIA AI Growth phase can convert trillion‑dollar forecasts into sustained shareholder gains.