Can NVIDIA’s AI infrastructure juggernaut keep powering explosive data-center growth, or are investors underestimating the risks building beneath the surface?

Is NVIDIA still driving the indices?

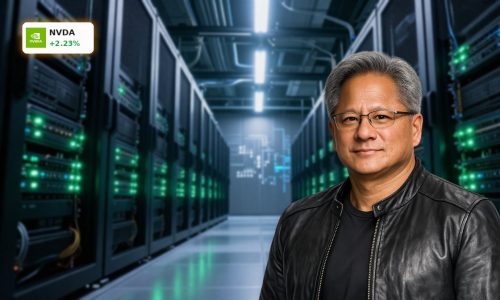

On Monday, NVIDIA Corporation (NVDA) was again one of the heaviest drags on the S&P 500 in pre‑market trading, echoing recent sessions where mega‑cap tech led the downside. At $177.66, the share price is off marginally from the prior close of $178.08, part of a pullback driven by concerns over higher interest rates, stretched valuations and whether AI capital spending can stay at today’s blistering pace. Yet over the last 12 months, the stock is still up roughly 60%, reflecting how central NVIDIA AI Infrastructure has become to both the NASDAQ and global equity benchmarks.

Recent quarters underline that dichotomy. NVDA delivered what many on Wall Street described as “incredibly strong” results, only to see the stock sold on worries about heavy capital expenditure at hyperscalers and the sustainability of China demand. Retail and institutional investors alike have tended to buy dips, treating NVIDIA alongside names like Apple and Tesla as core long‑term holdings rather than short‑term trading vehicles.

How strong is NVIDIA’s data-center engine?

The growth backdrop remains exceptional. For its fiscal 2026 year, NVIDIA reported revenue of almost $216 billion, up 65%, with non‑GAAP EPS rising 60% to $4.77. Management guided for $78 billion in revenue in the first quarter of fiscal 2027, implying 77% year‑over‑year growth and a non‑GAAP gross margin near 75%, versus 71.3% a year earlier. The bulk of this surge is coming from AI data centers, where NVIDIA AI Infrastructure – accelerated computing platforms, networking and software – has become the default standard for training and inference at scale.

Citigroup recently named NVIDIA and Broadcom as top semiconductor picks following earnings, highlighting AI‑driven data‑center demand as the key tailwind for both. Together they now account for roughly a third of total semiconductor sales into data centers. Other asset managers are increasing exposure as well: Greenwoods Asset Management Hong Kong and EDENTREE Asset Management both disclosed large percentage increases to their NVDA holdings, even as some insiders took profits.

NVIDIA AI Infrastructure: just GPUs, or much more?

While GPUs remain the flagship, the NVIDIA AI Infrastructure story now spans networking, software and edge deployments. The company describes itself as the “computational backbone” of modern AI, with platforms deployed from cloud regions to factory floors and even satellites. A recent demonstration of an H100 GPU operating in orbit underscored how far AI workloads are pushing beyond traditional data halls.

Physical AI is emerging as a major second act. NVIDIA has already generated about $6 billion in revenue from physical AI applications such as autonomous vehicles, drones and advanced robotics. In a fresh move, ABB Robotics announced it is integrating NVIDIA Omniverse and accelerated computing into its RobotStudio platform, aiming to close the gap between virtual simulations and real‑world robot performance in factories. By enabling highly realistic digital twins, the partnership should cut prototyping needs and time‑to‑market for industrial automation, further embedding NVIDIA AI Infrastructure in manufacturing workflows.

What about competition and supply risks?

The boom in AI hardware is reshaping upstream supply chains. For its next‑generation “Vera Rubin” AI platform, NVIDIA has reportedly tapped Samsung and SK Hynix as exclusive suppliers of sixth‑generation HBM4 chips, sidelining Micron, which has struggled to meet strict technical thresholds. The two Korean memory giants are using their clout to push through 20%–30% price increases, signaling that AI build‑outs will remain capital intensive for cloud providers and enterprises.

On the competitive front, hyperscalers like Apple and other members of the so‑called “Magnificent Seven” are developing custom accelerators, but the ecosystem of CUDA software, networking, and developer tools gives NVIDIA a moat that rivals find hard to match. At the same time, regulatory risks are real: tightened U.S. export rules have already forced NVIDIA to scale back certain high‑end shipments to China, introducing volatility into what has become a multi‑billion‑dollar quarterly revenue stream.

How is Wall Street valuing NVDA now?

Despite the huge run‑up of recent years, NVDA’s valuation has compressed as earnings have outpaced the share price. The stock now trades at roughly 22 times forward earnings, below the Nasdaq‑100’s aggregate multiple, even though consensus expects earnings growth above 70% in the current fiscal year. Some analysts have described an “unholy trinity” restraining upside in the near term – smaller earnings beats versus prior quarters, China revenue uncertainty, and questions around how aggressively NVIDIA will deploy its growing cash pile.

We are building this foundation that the market sits on, the engine of superintelligence.

— Josh Payne, CEO of Nscale

Conclusion

Nevertheless, several strategists now argue that mega‑cap AI leaders such as NVDA are transitioning from pure momentum plays to “value within growth.” On a wish‑list of buys for the latest sell‑off, portfolio managers have repeatedly grouped NVIDIA with long‑term compounders like Apple and Tesla, seeing them as rare beneficiaries of secular trends that can support portfolios through multiple cycles.

Further Reading

- NVIDIA Corporation (NVDA) quote and profile (Yahoo Finance)

- Broadcom, Nvidia, TI and Monolithic emerge as ‘top picks’ among semis after earnings (Seeking Alpha)

- What’s Behind The 60% Rise In Nvidia Stock? (Forbes)

- ABB teams up with Nvidia to improve factory robot training (Reuters)

- Nvidia-Backed Startup Nscale Raises Funds At $14.6 Billion Valuation (Wall Street Journal)