Is the NVIDIA AI Outlook signaling a durable trillion‑dollar supercycle or the moment the market finally calls peak AI?

Is the NVIDIA AI Outlook breaking the AI trade?

AI leaders have poured hundreds of billions of dollars into data centers, with total AI‑related capex this year estimated near $700 billion. That spending has created a historic chip supercycle and turned NVIDIA Corporation into the clear winner in AI GPUs, powering everything from large language model training to enterprise inference. Yet the broader “AI trade” that drove the S&P 500 and Nasdaq to records has started to fracture as investors rotate into value and smaller caps.

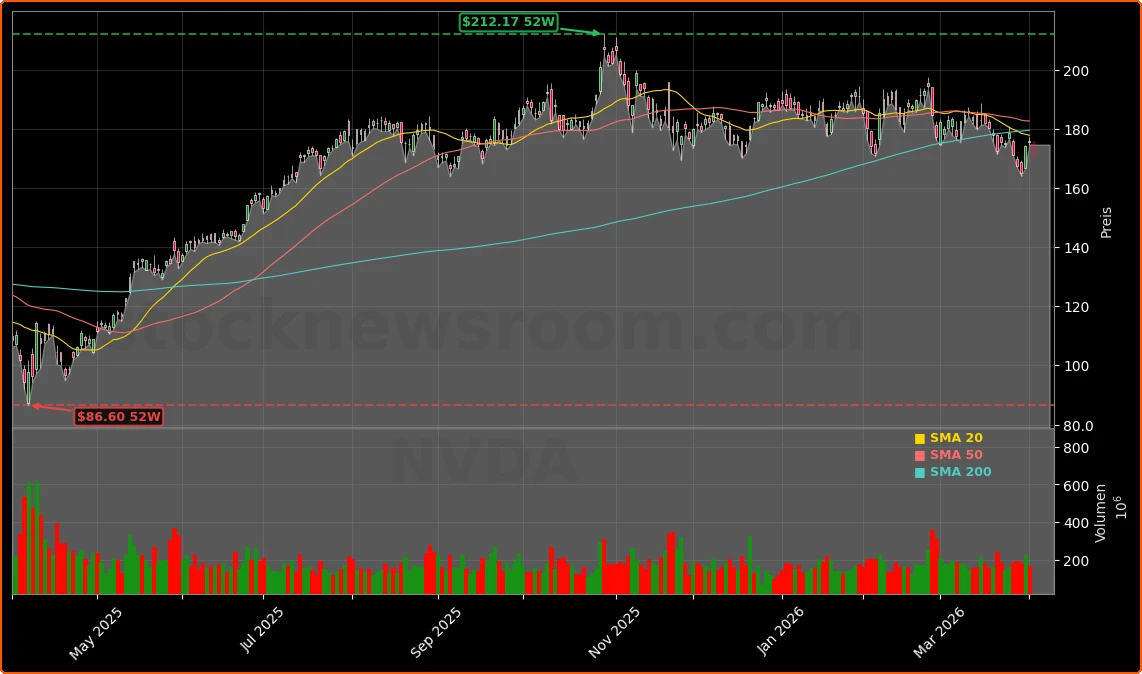

NVIDIA shares remain more than 20% below their recent peak, but the stock still sits on enormous long‑term gains. NVDA rallied sharply yesterday, jumping about 5.5% in a single session as volatility eased and the Magnificent 7 bounced together, before giving back some ground in pre‑market trading. The immediate push‑and‑pull reflects a market trying to reconcile extraordinary fundamentals with rising macro and geopolitical risks, from higher yields to the conflict in the Middle East that has weighed on semiconductor sentiment.

Institutional investors continue to lean in. First Merchants Corp lifted its stake in NVIDIA by 5.3% in Q4, now holding roughly 167,772 shares worth over $31 million, even as insiders sold about $253 million in stock over the same period. That mix of insider profit‑taking and institutional accumulation underscores how polarized the NVIDIA AI Outlook has become.

How strong is NVIDIA’s AI supercycle story?

NVIDIA’s current business is overwhelmingly tied to AI data‑center demand. The company generated about $215.9 billion in revenue over the last four quarters, with an EBIT margin near 62% and operating cash flow topping $100 billion. It holds a net cash position of roughly $34 billion and has returned about $41 billion via buybacks, despite offering only a token dividend yield around 0.02%.

The NVIDIA AI Outlook is anchored in CEO Jensen Huang’s claim that the company has line of sight to more than $1 trillion in cumulative sales through 2027 from its Blackwell GPUs and upcoming Vera Rubin platform. Blackwell remains its flagship training chip, while Vera Rubin targets inference and full‑rack AI servers, bundling GPUs, CPUs, and high‑speed networking. With agentic AI and digital employees emerging as the next wave of enterprise adoption, inference could be an even larger revenue pool than training over time.

NVIDIA’s moat goes beyond silicon. Its CUDA software stack and years‑long work with leading AI labs have created a de facto standard across hyperscalers and research institutions. Analysts estimate the company controls roughly 70–80% of the AI‑accelerated data‑center GPU market, with networking—bolstered by the Mellanox acquisition—now its fastest‑growing segment. That combination of hardware leadership, software lock‑in, and ecosystem depth remains central to bullish expectations from major Wall Street firms such as Goldman Sachs and Morgan Stanley, which both maintain Buy‑equivalent ratings and see the current pullback as a buying opportunity.

NVIDIA AI Outlook vs. Broadcom and hyperscaler chips

Even with its lead, NVIDIA is no longer the only way to play the AI infrastructure boom. Broadcom has emerged as a key competitor, especially in custom AI accelerators and networking. Ray Dalio’s Bridgewater Associates, for example, reportedly increased its Broadcom stake by nearly 40% in Q4, betting on the company’s “two‑engine” model of AI hardware plus high‑margin software. Valuations for NVIDIA and Broadcom are now comparable on a sales multiple basis—roughly 19–21 times trailing revenue—but Broadcom’s more diversified business mix gives it a different risk profile.

At the same time, several of NVIDIA’s largest cloud customers, from Amazon to Microsoft and Google parent Alphabet, are building in‑house AI chips to reduce dependence on expensive GPUs and gain more control over their roadmaps. These alternatives often lag NVIDIA in raw performance but can be cheaper and more readily available. Over time, that could chip away at NVIDIA’s pricing power and its ability to maintain gross margins in the mid‑70s, levels far above the semiconductor norm around 50%.

Meanwhile, geopolitical risk is rising. Escalating trade tensions and export controls have already limited high‑end GPU sales to China, capping near‑term growth in one of the world’s largest data‑center markets. On top of that, the current Iran conflict has pressured chip stocks such as NVIDIA and Broadcom on fears of energy‑price spikes and potential supply‑chain disruptions, as noted by recent coverage from Barron’s.

Could NVIDIA really fall to $100?

Some market strategists argue that the parabolic AI trade now looks vulnerable. The Shiller P/E ratio for the U.S. market entered 2026 at its second‑highest level in over 150 years—territory historically followed by 20%‑plus drawdowns. NVIDIA’s own price‑to‑sales ratio has reached levels previously associated with tech bubbles. In that context, one high‑profile forecast suggests NVIDIA shares could drop to $100, more than 40% below current levels and over 50% off their all‑time high, if the AI bubble deflates and AI capex slows more sharply than expected.

Bears also point to growing capex fatigue among the hyperscalers and rising concerns over power constraints for new data centers. If cloud giants begin to rein in spending, the impact would ripple through the entire AI hardware stack. For highly cyclical semiconductors, a turn in the spending cycle has historically led to steep inventory corrections and margin pressure, even for best‑in‑class players.

Bulls counter that fears of an imminent AI peak are overdone. NVIDIA’s last reported quarter showed revenue growth of roughly 73% year over year, with management guiding to further acceleration in the current fiscal period. On a forward basis, the stock now trades below 20x this year’s earnings estimates and under 15x next year’s, multiples some long‑term investors view as reasonable for a company still compounding revenue at outsized rates. Long‑only managers like Stephanie Long at Stash Away argue that supply bottlenecks at foundry partners such as TSMC could actually lengthen the cycle by preventing an immediate glut of AI chips.

What does this mean for U.S. investors now?

For American portfolios, the NVIDIA AI Outlook boils down to a classic high‑beta growth decision. NVDA is a core component of the S&P 500 and Nasdaq‑100, a favorite among day traders—often trading over 400 million shares daily—and a key driver of mega‑cap tech indices. Its dominance in GPUs makes it the closest thing to “picks and shovels” for AI, but its dependence on one secular theme leaves it exposed if AI infrastructure spending stumbles.

Investors worried about volatility have turned to more defensive structures, such as capped discount certificates and options overlays, to gain exposure without betting on aggressive upside. Others are pairing NVIDIA with rivals like Broadcom or even hyperscaler stocks to build a more balanced AI basket. Either way, risk management is increasingly front and center as Wall Street digests both trillion‑dollar opportunity and bubble talk in the same breath.

Related Coverage

For a deeper look at how new commercial wins may shift sentiment, see “NVIDIA Mega Deals +5.6% Rally Shock on OpenAI, Marvell Bets”, which explores whether recent OpenAI and Marvell partnerships mark a true inflection point for NVDA’s growth trajectory. Investors tracking the broader chip race should also read “Intel Fab 34 buyback $14.2B Surge in AI Ambition”, analyzing Intel’s attempt to close the manufacturing gap with rivals like NVIDIA and how that could reshape the AI hardware landscape over the next decade.

Ultimately, the NVIDIA AI Outlook remains a tug‑of‑war between supercycle optimism and bubble caution. For long‑term investors, the stock’s combination of ecosystem strength, balance‑sheet firepower, and secular AI demand keeps it firmly on the radar, even if near‑term volatility stays elevated. The next few quarters of data‑center orders and margin trends will be critical in showing whether today’s pullback is a buying window or the start of a more painful reset for one of Wall Street’s most important growth stories.