Can the NVIDIA AI Strategy keep turning explosive AI demand into outsized growth, or is the market finally nearing its limits?

Is NVIDIA still the AI market’s anchor?

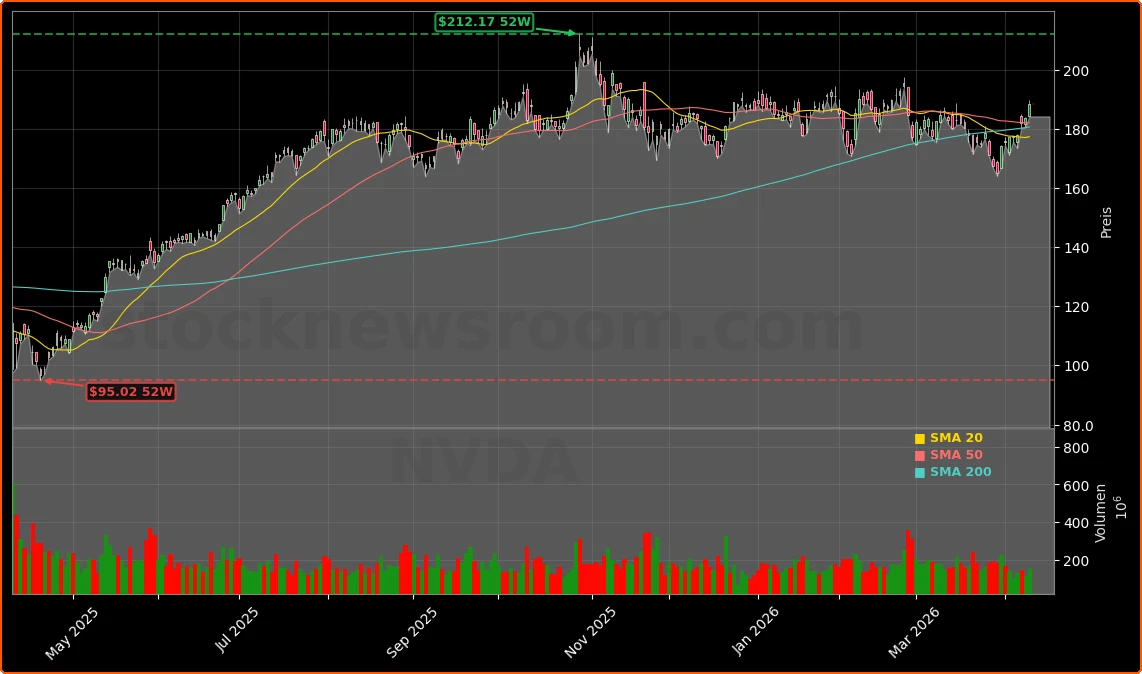

At roughly $188 per share, NVIDIA Corporation trades at about 21 times forward earnings, a multiple that is no longer nose‑bleed by high‑growth tech standards and only moderately above the S&P 500’s valuation. The company just delivered a 65% year‑over‑year revenue jump in fiscal 2026, an extraordinary pace for a business with a market value around $4.6 trillion. Despite recent volatility, analyst coverage remains overwhelmingly positive: TipRanks data show 41 of 43 Wall Street analysts rate the stock a “Buy,” with an average price target near $274, implying roughly 45%–54% upside from current levels.

The NVIDIA AI Strategy is built on selling the compute “picks and shovels” of the AI gold rush: GPUs for training and inference in hyperscale data centers. Unlike many software names that have fallen more than 20% during the 2026 tech shakeout, chipmakers tied directly to AI infrastructure have continued to post double‑digit gains. NVIDIA sits at the core of that trend and remains a top holding in many U.S. equity and even dividend‑oriented funds, where high weightings in NVIDIA, Apple and Microsoft tilt portfolios toward growth rather than pure income.

How is the NVIDIA AI Strategy evolving?

Management is not dialing back ambitions. CEO Jensen Huang has outlined a path to $1 trillion in cumulative chip sales from the Blackwell platform and the upcoming Vera Rubin architecture between March 2026 and the end of 2027. That guidance underpins the NVIDIA AI Strategy to refresh its entire data‑center stack roughly every 12–18 months, driving recurring upgrade cycles at cloud giants like Amazon, Alphabet and Meta, as well as enterprise AI adopters.

NVIDIA is also deepening its reach into the broader AI ecosystem. A recent expansion of its collaboration with Cadence Design Systems focuses on “agentic AI” and physical AI‑accelerated tools that optimize chips and systems for Grace CPUs and Blackwell GPUs, boosting throughput while lowering power consumption. Electronic design automation players Synopsys and Cadence increasingly tailor their flows for NVIDIA architectures, reinforcing NVIDIA’s role as the reference platform for cutting‑edge silicon and system design.

Beyond chips, the NVIDIA AI Strategy extends into robotics and so‑called “world models.” The company’s GPUs and software are frequently described as the “brain” of emerging humanoid robots, with U.S. AI research and low‑cost Asian manufacturing echoing the globalization model that helped Apple scale the iPhone. If autonomous machines and industrial robots ramp as expected over the next decade, NVIDIA’s compute platforms could become embedded in factories, warehouses and consumer devices far beyond today’s data centers.

What are the bottlenecks around NVIDIA?

The AI boom is straining the supply chain that feeds NVIDIA’s growth. Massive capex commitments from hyperscalers have created shortages in optical and electrical components, pushing prices sharply higher. Optical networking vendors such as Lumentum have reported that key AI‑related products are effectively booked through 2027, helped by long‑term purchase commitments and investments from NVIDIA that secure bandwidth for its GPU clusters.

This infrastructure angle is central to the NVIDIA AI Strategy. To sustain performance leadership, NVIDIA is tying up ecosystem capacity from fiber and laser specialists to advanced packaging, while partnering with CPU vendors like Intel that benefit from AI workloads needing more central processing alongside GPU accelerators. For investors, that means the AI trade no longer rests on a single stock but on a layered stack of enablers in chips, optics and cloud infrastructure, even as NVIDIA remains the economic core.

Does NVIDIA’s size cap future returns?

Despite stellar execution, the law of large numbers is the main bear argument. With a market cap already above $4 trillion, a 10x return from here would imply a $46 trillion valuation — financially implausible in any reasonable timeframe. More realistic is a scenario where sustained double‑digit revenue expansion and robust margins support a potential doubling to around $9 trillion over several years, even as the P/E ratio gradually compresses closer to the broader market.

That dynamic explains the recent split between growth and more conservative investors. For those seeking early‑stage, multi‑bagger upside, newer AI infrastructure names in optics or niche accelerators may look more exciting. Yet for institutions and retirees, the NVIDIA AI Strategy offers a rare combination: dominant market share, strong balance sheet liquidity of more than $60 billion, and ongoing earnings growth that could still outpace the S&P 500 without relying on speculative assumptions.

Related Coverage

Investors looking for a deeper dive into valuation can read how NVIDIA’s earnings momentum and trillion‑dollar ambitions stack up against its current multiple in “NVIDIA AI Growth +2.6%: Is the AI Boom Still a Bargain?”. For a broader sector perspective, Meta’s massive $135 billion AI capex push and its Muse Spark rollout are analyzed in “Meta AI Strategy Boom: $135B Capex Bet Shocks Wall Street”, highlighting how hyperscaler spending patterns feed directly into NVIDIA’s long‑term demand pipeline.

The NVIDIA AI Strategy continues to place the company at the heart of the global AI build‑out, even as its sheer scale tempers dreams of another 10x rally. For U.S. investors, the stock increasingly looks like a core AI infrastructure holding rather than a speculative rocket ship. The next few quarters of cloud capex and competitive launches will show whether NVIDIA can keep converting its strategic roadmap into market‑beating returns.