How can an NVIDIA quarter end with historic records while the stock simultaneously faces significant pressure?

How strong was the current NVIDIA quarter?

NVIDIA has reported figures for the completed fiscal year 2025/26 and the most recent quarter that are nearly unmatched in the semiconductor industry. Quarterly revenue surged by 73% to $68.1 billion, and net profit exploded by 94% to nearly $43 billion. The gross margin climbed to around 75%, with the operating margin approaching 60%. This positions the company among the most profitable large corporations worldwide.

The data center business remains the key driver, now accounting for nearly 90% of revenues. In this segment alone, NVIDIA generated $62.3 billion, an increase of about 75% year-over-year. In contrast, gaming and automotive revenues fell short of analyst expectations, with figures of $3.73 billion and $0.6 billion, respectively, further shifting the focus of the narrative towards AI infrastructure.

For the year, NVIDIA achieved nearly $216 billion in revenue—about two-thirds more than the previous year. Annual profit rose to approximately $120 billion, a 65% increase. Morgan Stanley referred to this momentum as the “greatest and cleanest beat-and-raise story in semiconductor history.”

Why did the stock market react so coolly to the NVIDIA quarter?

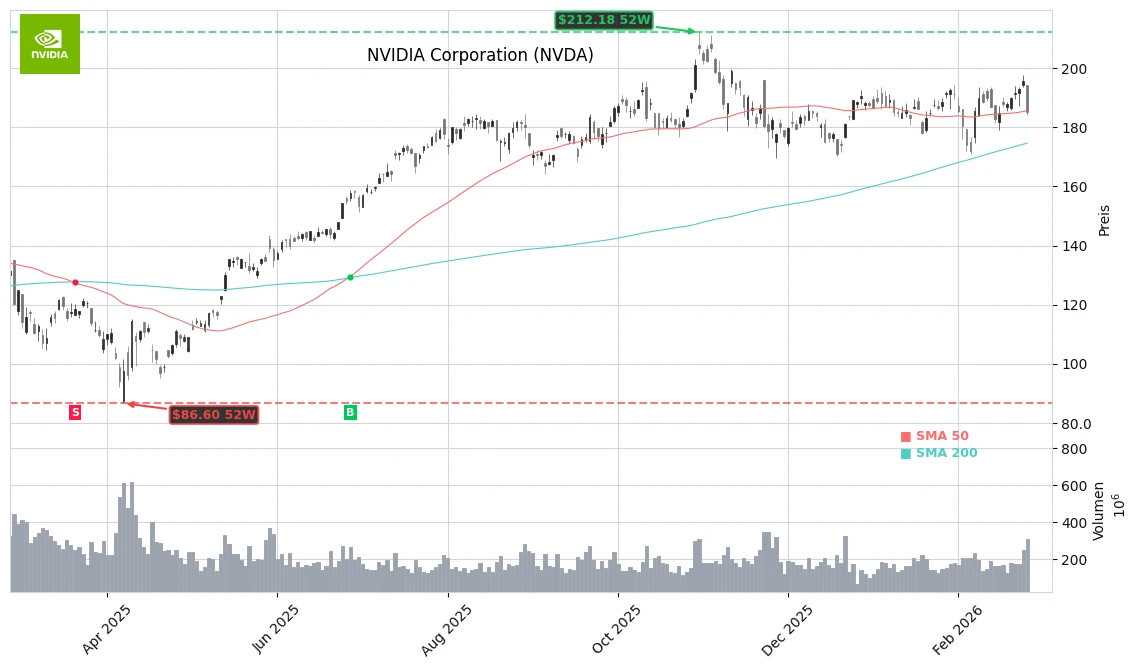

Despite the record NVIDIA quarter, the stock lost about 5% in US trading on Thursday, closing at approximately $185.33, significantly down from the previous day’s close of $195.63. The shares had already surrendered their initial gains overnight. This trend continues, which many market observers see as a sign of an “overcrowded trade”: expectations for NVIDIA are so high that even blockbuster numbers hardly spark any enthusiasm.

Analysts also point to structural concerns. A significant portion of revenue depends on a few hyperscalers like Microsoft, Meta, Alphabet, and Amazon, whose AI investment budgets for 2026 are estimated at around $650 billion. Investors doubt whether this level of CapEx can be sustained long-term—and how quickly these massive infrastructure investments can be monetized by customers.

Additionally, uncertainty surrounding China weighs heavily. In its forecast for the current quarter, NVIDIA does not account for any significant data center revenues from the People’s Republic, despite limited licenses for H200 chips being available again. There is also intensified competition from Chinese providers and custom AI chips from the hyperscalers themselves.

What does the outlook say for the next NVIDIA quarter?

The outlook is objectively strong: For the current quarter, NVIDIA expects around $78 billion in revenue, plus or minus 2%. This is significantly above the consensus of about $73 billion and implies growth of approximately 77% year-over-year. The gross margin is expected to remain exceptionally high at 75%. CFO Colette Kress emphasizes that demand for the current Blackwell systems, as well as the upcoming Vera Rubin and Rubin platforms, is visible well into 2027.

At the same time, supply shortages of High Bandwidth Memory (HBM) and a tenfold increase in inventory dampen the enthusiasm: inventory and receivables have risen sharply, and some investors fear “vendor financing,” meaning partial financing of large customers by NVIDIA itself. CEO Jensen Huang rejects accusations of an AI bubble, arguing that “computing power equals revenue” and that customers are already achieving high returns on their investments—especially through agentic AI and inference workloads.

The analyst front remains predominantly optimistic. Citigroup and Bernstein have set price targets in the range of $275 to $300, while Wedbush analyst Dan Ives describes the recent numbers as the “Michael Jordan moment” of the chip industry. At the same time, firms like Morgan Stanley caution that growth from 2027 onward is likely to depend more on the overall capital market sentiment and the CapEx willingness of hyperscalers.

What does the NVIDIA quarter mean for investors?

For investors, the current NVIDIA quarter serves as a lesson in expectation management. Fundamentally, the company delivers records in revenue, profit, and cash flow, dominates the AI accelerator market, and has a credible pipeline for reducing inference costs and increasing energy efficiency with future platforms like Vera Rubin. At the same time, the stock reaction shows that the market is now primarily pricing in the sustainability of the AI investment cycle and the concentration risk associated with a few large customers.

In this new world of AI, computing power is revenue. Without computing power, there is no way to generate tokens.

— Jensen Huang, CEO of NVIDIA

Bottom Line

While Zacks Investment Research continues to classify NVIDIA as a momentum favorite, market comments reflect “AI fatigue”: it is no longer enough to beat expectations—the growth scenario must also be credibly scaled beyond 2026. Therefore, those entering the market are betting less on whether AI is coming and more on how long NVIDIA can defend its dominant position and margins.

Related Sources

- NVIDIA Corporation (NVDA) on Yahoo Finance (Yahoo Finance)

- Nvidia earnings fail to lift broader chip sector; AMD, Broadcom down (Investing.com)

- Here’s just how impressive Nvidia’s earnings were, according to Morgan Stanley (MarketWatch)

- Nvidia Q4 report keeps analysts confident in AI chip firm’s long-term earnings power (Proactive Investors)