Will the upcoming NVIDIA quarter confirm the AI boom with new records or signal the start of a painful correction?

NVIDIA Quarter: How High is the Expectation Pressure?

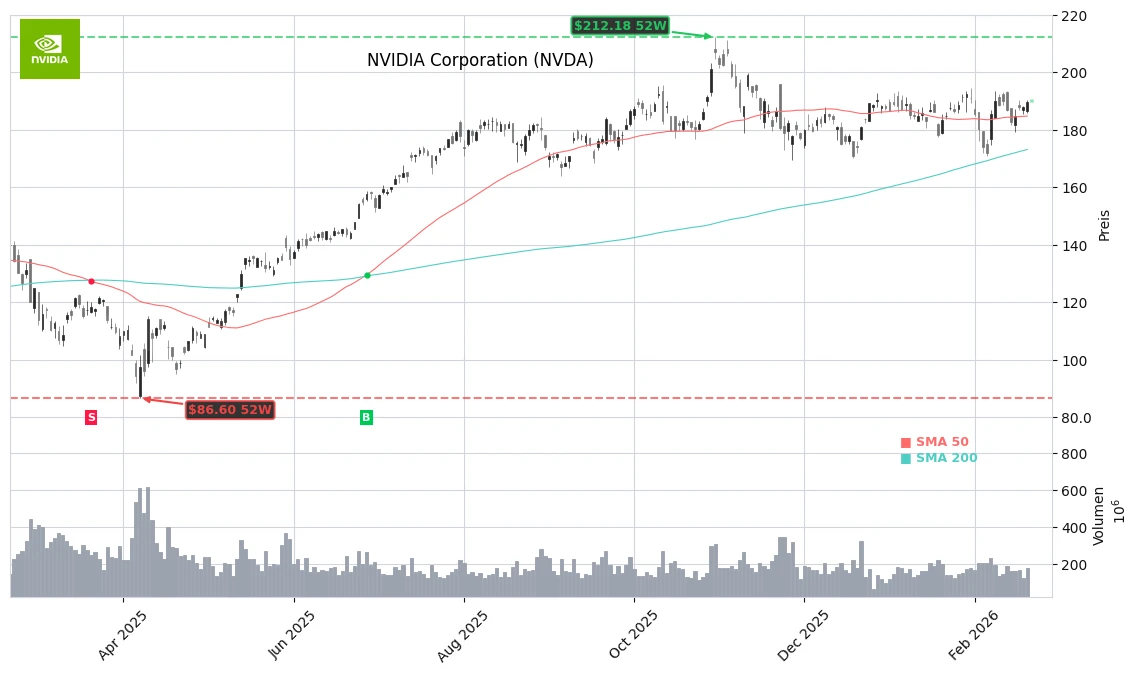

The significance of the current NVIDIA quarter cannot be overstated. The stock has experienced an unprecedented rally since the AI boom in 2023 but has been in a broad sideways phase since October, currently trading around $189.82, approximately $23 below its record high. Options traders are bracing for significant price swings: a movement of about 6% in either direction is priced in for the report on Wednesday evening, which could translate to a value change in the hundreds of billions given the massive market capitalization.

The consensus estimates are clear: for the current NVIDIA quarter (fiscal Q4), Wall Street expects revenue of about $65.7 to $66 billion and an adjusted earnings per share of around $1.52, representing a profit increase of about 71% compared to the previous year. What matters less is whether NVIDIA meets expectations—this is now seen more as a disappointment—but whether the company once again significantly exceeds them and confirms the growth story.

NVIDIA: The Heart of the AI Boom – But is the Growth Sustainable?

NVIDIA Corporation is the dominant provider of AI accelerators for data centers, with an estimated market share of around 80%. The company’s GPUs are considered the gold standard for training and inferencing large AI models. In the previous quarter, revenue surged to around $57 billion, profits increased even faster, and the gross margin was in the mid-70% range—well above the industry average of about 50%.

The management team led by CEO Jensen Huang projected further revenue growth of around 65% for the current quarter, aiming for a new record of approximately $65 billion. The Blackwell generation is particularly in demand, with demand described as “off the charts,” while cloud GPUs are essentially sold out. Strong impulses are also expected in the coming years from the new GB300-Ultra architecture and the Rubin platform, which address hyperscale AI data centers.

At the same time, the question of how to monetize the massive AI investments is coming into focus. Hundreds of billions of dollars in CapEx from hyperscalers and Mag-7 companies are flowing into AI infrastructure, but investors increasingly want to see how quickly these expenditures translate into additional revenues and margins—both for NVIDIA and for software and cloud providers.

NVIDIA: What Do Analysts Say About the Upcoming Report?

Several major firms see room for growth despite the already significant stock gains. Oppenheimer analyst Rick Schafer maintains his “Outperform” rating and believes NVIDIA could exceed revenue estimates for the NVIDIA quarter by $2 to $3 billion, primarily due to the ramp-up of the GB300-Ultra systems. His price target is $265. Canadian bank RBC Capital Markets also remains at “Outperform” with a price target of $240, supported by a growing order backlog and the Rubin GPU platform.

Other firms like Needham (price target of $240), Stifel Nicolaus (price target of $250), UBS (price target of $245), and Wells Fargo (price target of $265) average a target around $252—indicating an analyst consensus with an upside potential of about 35% from the current price. Notably, despite the extremely high expectations, some strategists assess the stock as relatively moderate based on the price-to-earnings ratio, after valuation metrics have significantly compressed in recent months.

NVIDIA: Risks from Competition, China, and Cycle End?

However, clear risks stand against the optimism. On the competitive side, players like AMD and major cloud providers are heavily investing in their own AI chips. Internal competition—meaning proprietary accelerators from key customers—could gradually weaken the previously extreme scarcity of high-quality GPUs and thus NVIDIA’s pricing power. Concurrently, there are geopolitical uncertainties surrounding export restrictions for high-end chips to China, a potential additional market of around $50 billion annually, should approvals for H200-based solutions be granted.

“NVIDIA has consistently delivered, but in this NVIDIA quarter, even a very strong result might not be good enough if it doesn’t exceed the extremely high whisper estimates.”

— Rhys Williams, Chief Strategist at Wayve Capital Management

Bottom Line

Additionally, operational risks such as potential bottlenecks in memory components and hard drives could delay the expansion of data centers or put pressure on margins. Therefore, investors are watching not only the numbers from the NVIDIA quarter but also the outlook: Will the growth rate remain in the mid-double-digit range as the market expects? And can management credibly demonstrate that the AI investment wave has not yet reached a cyclical peak?

Related Sources

- NVIDIA Corporation on Yahoo Finance (Yahoo Finance)

- Nvidia Stock Is Rising. Why It’s Defying the Tech Sector Selling Today. (Barron’s)

- Nvidia Stock Is Stuck, But JPMorgan Anticipates Another ‘Beat-And-Raise’ (Benzinga)

- KG: “Trust the Technicals” as NVDA Report Looms (Schwab Network)