Will the upcoming NVIDIA quarter continue to fuel the AI boom or reveal cracks in the hype for the first time?

NVIDIA Quarter as a Stress Test for the AI Hype?

The upcoming NVIDIA quarter is considered one of the most important events of this earnings season. Wall Street expects a revenue jump of about 67 to 68% to around $65 to $66 billion and an earnings per share increase of over 70% to about $1.53. Some firms like Goldman Sachs even anticipate revenues exceeding $67 billion. At the same time, a massive increase in free cash flow of over 100% compared to the previous year is expected.

This sets the bar extremely high: NVIDIA has almost ritualistically exceeded estimates in recent quarters, and buy-side whisper estimates are significantly above the official consensus. However, options traders are pricing in, according to Reuters, the smallest expected price movement after earnings in three years – an indication that many professionals expect a more controlled reaction rather than an “event trade” like in previous hype phases.

Additional nervousness stems from the fact that technology and especially AI stocks have started 2026 on a weaker note. Reuters points to growing skepticism towards highly valued tech stocks, while other sectors are attracting capital. NVIDIA thus finds itself at the center of the question of whether the AI investment cycle is losing its shock value for the overall market or triggering a new wave of euphoria.

NVIDIA: Expectations for Growth, Margins, and China

The focus of today’s report is on three key metrics. First: revenue growth in the data center business, which continues to account for the majority of the company’s revenue. Following over 60% growth in the previous quarter, investors expect demand from hyperscalers like Meta, Microsoft, and Amazon to remain high, confirming the pipeline of over $500 billion in orders for the coming quarters.

Second: the gross margin. Analysts expect GAAP gross margins of around 74 to 76%. If the outlook for the next NVIDIA quarter and the new fiscal year is significantly weaker here, it would be a clear signal that the extreme chip shortage is easing or that pricing pressure from AMD and the “Magnificent Seven” own solutions is increasing. Conversely, if margins remain in the high 70% range, it would be a strong indication that NVIDIA still possesses significant pricing power.

Third: the China complex. The U.S. government has recently tightened regulations on the export of high-performance AI chips, while discussions are underway regarding initial shipments of the H200 to China. Investors are paying close attention to precise statements from CEO Jensen Huang regarding actual demand, approvals from Chinese authorities, and potential circumvention risks through third countries. Any clarification could significantly influence the perception of regulatory risks in the upcoming NVIDIA quarter.

NVIDIA and the AI Market: What Are the Expectations?

Beyond the pure numbers, the NVIDIA quarter serves as a seismograph for the entire AI sector. New products like the Vera Rubin platform and the expansion of the Blackwell architecture are expected to bring another leap in computing power and memory bandwidth, according to company guidance. Crucial is whether NVIDIA will announce specific timelines, pre-orders, and CapEx commitments from major customers – particularly regarding the recently deepened partnership with Meta.

At the same time, NVIDIA is expanding its role in “Physical AI”: investments such as in Wayve in the autonomous driving sector demonstrate that the company is addressing not only data centers but also robotics and mobility. For many analysts, this area is not yet fully priced into the stock and could become an important growth story beyond the upcoming NVIDIA quarter.

On the investor side, the tailwind remains robust: MarketBeat reports significant position increases from major players like Principal Financial Group and Prostatis Group, while analysts generally issue buy recommendations and price targets around $245 to $270. Citigroup, UBS, and other firms emphasize NVIDIA’s central role as a “must-own” in the global AI infrastructure trend, but also warn of the risk of a “sell on news” if the outlook is not raised again.

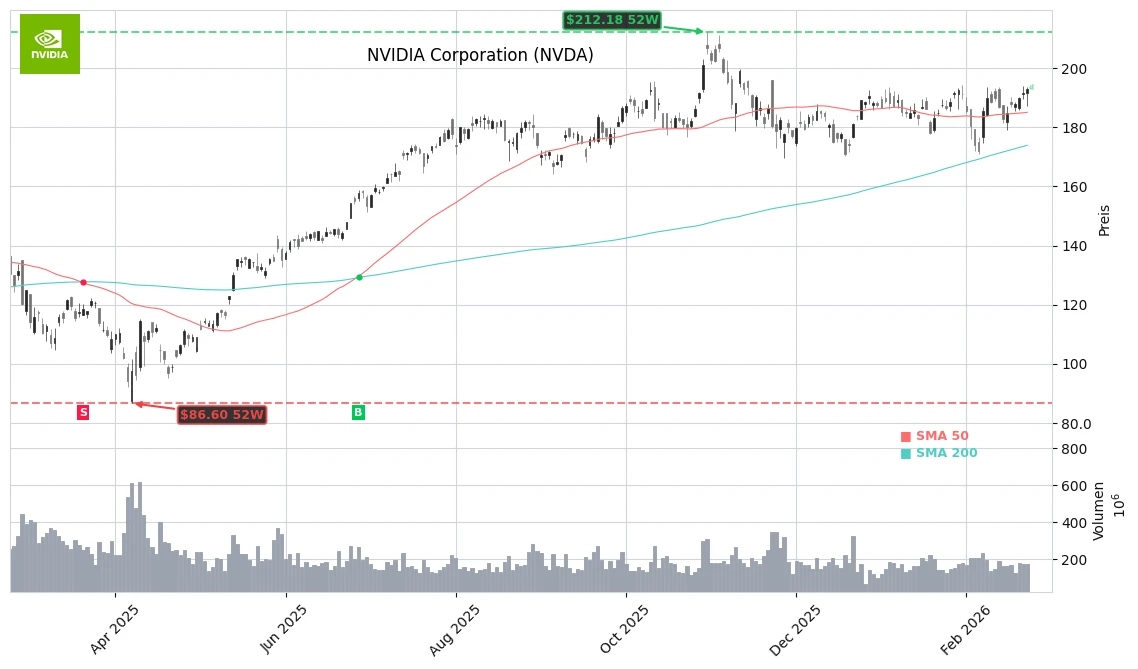

At the same time, valuation remains a topic: despite the consolidation since October, the stock is trading with a forward P/E in the high 20s, making it significantly cheaper than at its peak, but still vulnerable to disappointments if revenue growth visibly slows in the next NVIDIA quarter.

NVIDIA is doomed to exceed expectations – any small disappointment could send ripples through the market beyond its own stock.

— Christian Henke, IG Markets

Bottom Line

Today’s NVIDIA quarter is more than just another set of numbers – it is a mood test for the entire AI boom. If Jensen Huang can exceed the already high expectations for revenue, margins, and outlook, the stock could end its sideways phase and lead the sector once again. For investors, NVIDIA remains a key stock whose performance in the coming quarters will significantly determine whether AI fantasy can be translated into sustainable profit growth.

Related Sources

- NVIDIA Corporation (NVDA) on Yahoo Finance (Yahoo Finance)

- Nvidia Heads Into Q4 Earnings With Vera Rubin Launch, China Chip Approvals, Meta Partnership (Benzinga)

- Options traders price Nvidia’s smallest post‑earnings swing in three years (Reuters)

- Principal Financial Group Inc. Increases Position in NVIDIA Corporation (MarketBeat)