Is the Occidental Petroleum Oil Market sell-off just war-risk premium fading or the start of a deeper reset in U.S. energy stocks?

Is the Iran peace talk rally hurting OXY now?

The sharp move lower in OXY reflects a broader rotation on Wall Street as investors price in a potential end to open hostilities with Iran. U.S. President Donald Trump signaled that a resolution could come within two to three weeks, while Iranian President Masoud Pezeshkian indicated Tehran is ready to halt the war in exchange for formal security guarantees. Those comments sent WTI crude down roughly 2% to about $100 per barrel, pressuring large-cap U.S. oil names in pre-market trading.

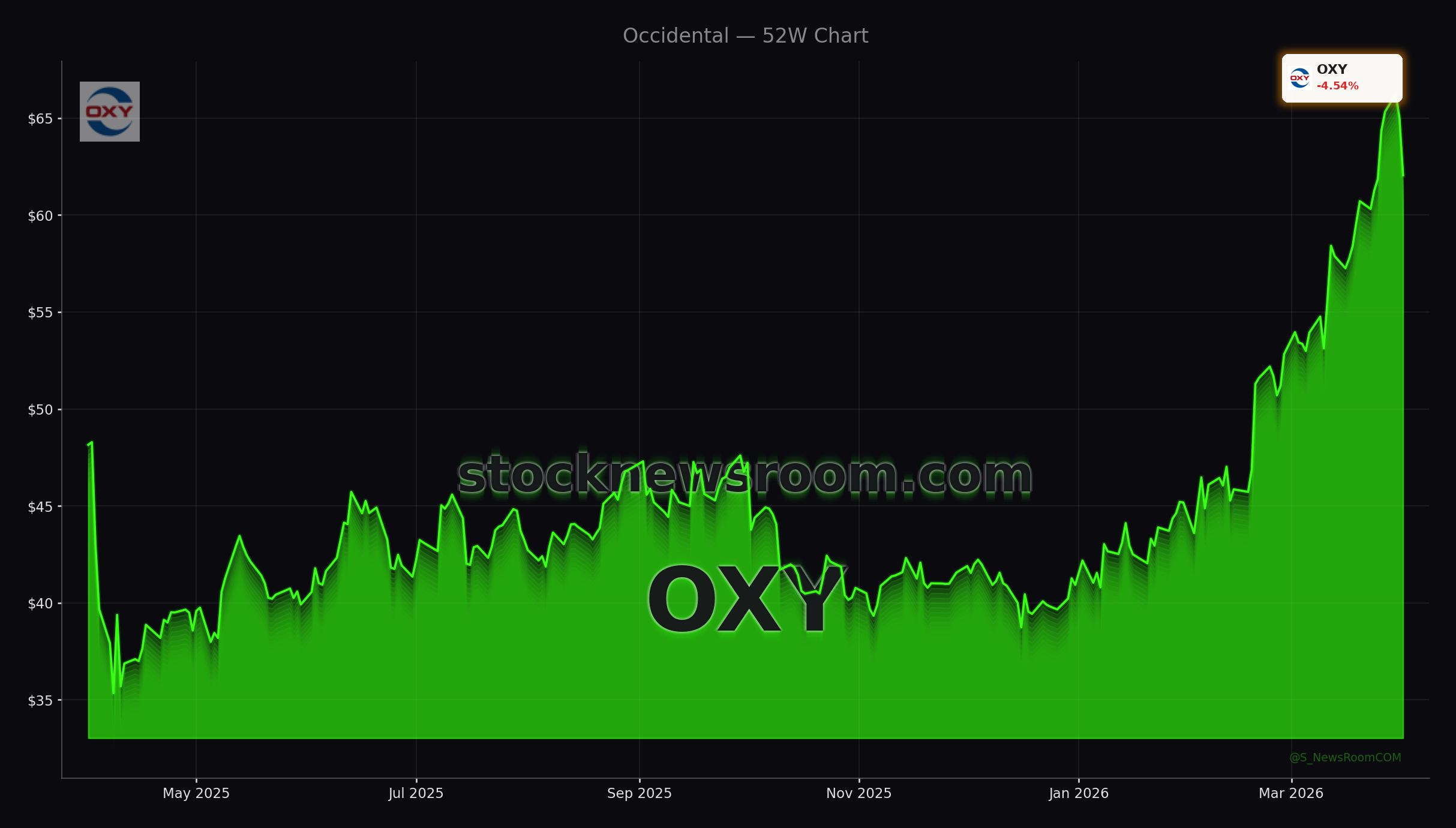

Occidental Petroleum Corporation fell as much as 3.5% in early moves, trading in lockstep with declines in peers like Exxon Mobil and Chevron. The stock had previously benefited from a powerful war-driven rally in March, with energy names among the few S&P 500 sectors posting double-digit gains while the broader market struggled. OXY itself has recently traded near its 52-week highs, putting today’s pullback into context as a correction rather than a collapse.

The Occidental Petroleum Oil Market debate now turns from pure geopolitical risk to how quickly supply and demand can normalize if shipping lanes through the Strait of Hormuz and Bab el-Mandeb remain open. Any sustained de-escalation would likely cap the war premium in crude, but it could also extend the cyclical upswing if global growth holds and inventories stay tight.

How is Occidental positioned in the current oil map?

From a strategic standpoint, Occidental Petroleum Corporation is relatively insulated from the most vulnerable Middle Eastern chokepoints. Roughly 84% of its production comes from the United States, primarily in the Permian Basin and other onshore plays. The company also has assets in Algeria, Oman, and the UAE, but its exposure to the Persian Gulf and Red Sea shipping lanes is limited compared with some state producers and Middle Eastern majors.

This geographic mix is critical to understanding the Occidental Petroleum Oil Market story. If Bab el-Mandeb or the Strait of Hormuz were to face renewed disruption, tanker flows could be heavily constrained, potentially lifting global prices even as physical supply is rerouted. In such a scenario, OXY’s largely domestic production profile could command a premium, as barrels produced and sold within North America avoid the most acute logistical risks.

Even under a de-escalation scenario, OXY has room to maneuver. Management has indicated the ability to ramp U.S. drilling activity to capture periods of higher pricing. That optionality is especially relevant for American investors focused on companies that can toggle capital spending up or down faster than state-controlled producers. Compared with integrated giants like Exxon Mobil or Chevron, Occidental is more of a pure play on upstream and U.S. liquids, with a smaller downstream footprint and a chemicals business (OxyChem) that Berkshire Hathaway helped monetize, strengthening the balance sheet.

What are analysts and Buffett signaling on valuation?

On the research side, Citigroup recently lifted its price target on OXY from $45 to $67 while maintaining a neutral rating, underscoring how the rally has already pulled the stock closer to updated fair-value estimates. Other analyst services highlight Occidental among stocks trading near 52-week highs with potential for further upside, supported by rising earnings estimates as crude prices remained elevated through Q1 2026.

Value-focused investors are also watching Warren Buffett’s Berkshire Hathaway, which has built substantial positions in both Chevron and Occidental Petroleum Corporation. By early 2026, those two oil bets were worth roughly $30.5 billion combined and had become some of Berkshire’s best-performing investments this year. Berkshire has also previously acquired OxyChem, allowing Occidental to reduce leverage and refocus on its core energy operations, a move that many on Wall Street see as de-risking the equity story.

While today’s drop reflects near-term sentiment tied to headlines out of the Middle East, the longer-term thesis many U.S. investors follow is more about disciplined capital returns, debt reduction, and exposure to structurally tight oil markets than about day-to-day commodity moves.

How does OXY stack up against U.S. energy peers?

In the context of the S&P 500 and the broader energy complex, OXY has lagged some high-flying tech names such as NVIDIA and Apple, but within the energy sector it has been a notable outperformer during the Iran war phase. Some research pieces argue that certain high-yield energy stocks were left behind during the initial surge and might now offer attractive income plus upside, placing Occidental in the conversation for yield-focused portfolios.

Many U.S. asset managers currently prefer domestic oil and gas producers like Occidental, Chevron, and Tesla-unrelated traditional energy plays over European majors such as Shell or BP, citing more shareholder-friendly capital allocation and regulatory environments. With crude still elevated despite the recent pullback, OXY’s ability to scale U.S. production and its relatively modest direct exposure to contested waterways continue to differentiate it in the Occidental Petroleum Oil Market landscape.