Is the latest Oracle Forecast betting too heavily on an AI cloud boom just as the stock slides sharply again?

Does the Oracle Forecast ignore today’s selloff?

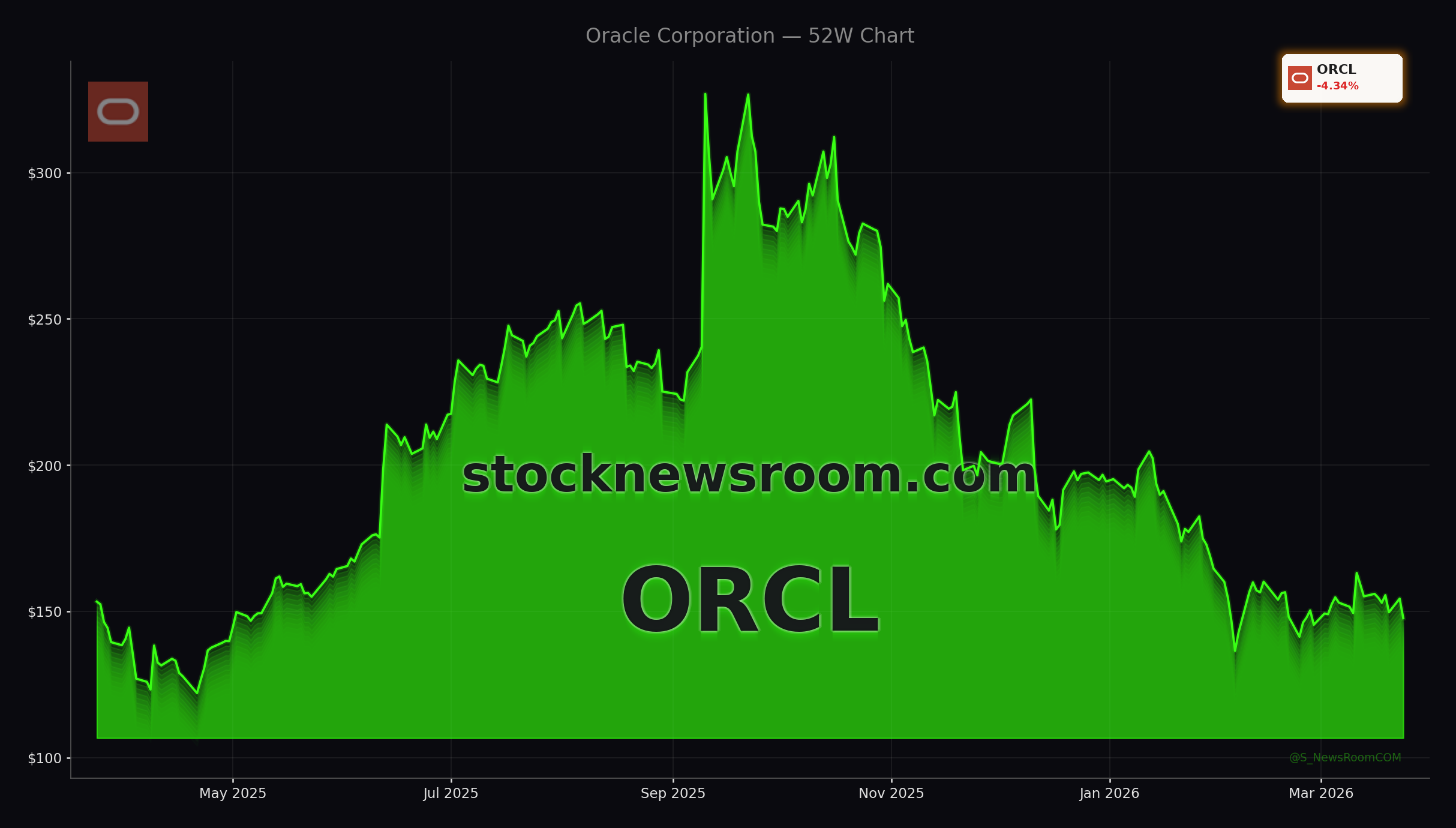

Oracle Corporation (ORCL) closed around $148.07 on Tuesday, down more than 4% from the prior session and roughly 24% year-to-date, as software names weighed on the S&P 500 and NASDAQ. The stock trades well below its 52-week high near $345, underlining how sentiment has cooled even as AI hype dominates Wall Street. Yet the consensus 12‑month target still sits near $249, implying substantial upside if the next Oracle Forecast plays out.

The latest catalyst is Bank of America’s Tal Liani, who reinstated coverage with a Buy rating and a $200 price target. That implies roughly 35% upside from today’s levels and pegs Oracle as one of the key infrastructure beneficiaries of the AI investment cycle alongside hyperscalers and chip leaders like NVIDIA. Liani’s call is more conservative than the Street average but stands out because it is grounded primarily in contracted revenue already on Oracle’s books.

At the same time, short‑term trading is being buffeted by competitive headlines. Oracle shares came under pressure after reports that Amazon is building its own AI agent tools to automate sales and business development workflows, stoking fears that cloud giants will crowd the field just as Oracle pushes deeper into agentic AI.

How does AI infrastructure shape the Oracle Forecast?

The bullish case behind the Oracle Forecast revolves around Oracle’s cloud infrastructure and AI build‑out. In its most recent quarter, cloud infrastructure revenue jumped 84% year over year to $4.89 billion, a growth rate that puts Oracle in the top tier of large‑cap software and infrastructure names. Management has repeatedly emphasized that AI‑driven demand for compute still exceeds available capacity, pushing the company into an aggressive expansion cycle.

The headline number for long‑term investors is Oracle’s remaining performance obligations (RPO), which reached an extraordinary $553 billion, up 325% year over year. CEO Safra Catz has indicated that most of the revenue in Oracle’s five‑year internal outlook is already embedded in this backlog, including a multi‑year roadmap that could take Oracle Cloud Infrastructure (OCI) to more than $100 billion in annual revenue by the end of the decade.

This contracted backlog is heavily tied to AI workloads, including large training clusters for leading models and long‑dated capacity commitments from enterprise customers. If Oracle can turn that RPO into recognized revenue while maintaining high growth in Infrastructure‑as‑a‑Service, the $200 Oracle Forecast becomes much easier to justify in a typical S&P 500 growth framework.

Is Oracle’s AI agent push enough against Big Tech rivals?

Beyond raw infrastructure, Oracle is leaning into AI at the application and database layers, which could diversify growth and improve margins. The company just rolled out 22 new Fusion Agentic Applications embedded in its Fusion Cloud suite, an upgraded Oracle AI Agent Studio, and new agentic AI features for its database platform. These tools are designed to let enterprises deploy autonomous agents that can reason over real‑time data, orchestrate workflows and deliver measurable business outcomes, pushing beyond simple copilots.

That move puts Oracle into a direct feature race with cloud and SaaS peers. Amazon is developing its own AI agent platform, and Microsoft, Apple and others are racing to embed generative AI and agents across their ecosystems. Oracle’s multicloud positioning is a partial hedge: its databases now run natively inside the clouds of Amazon, Google and Microsoft, and multicloud database revenue has surged more than 500% year over year. For U.S. investors, that means Oracle can benefit from AI adoption even when workloads technically sit on a rival cloud.

Still, tech volatility is reminding the market that AI is not a one‑way trade. Salesforce and other software leaders slid roughly 4% or more in the latest session, and Oracle’s drop shows it is not immune to sentiment shocks when investors question whether AI tools could disrupt established SaaS models or compress pricing power.

Can balance sheet risks derail the Oracle Forecast?

The biggest challenge to the bullish Oracle Forecast lies in cash flow and leverage. To meet AI demand that currently outstrips supply, Oracle has embarked on a roughly $50 billion capex program for fiscal 2026, focused on data centers, GPUs and networking. That surge in investment has pushed trailing free cash flow to around negative $24.7 billion, while non‑current debt has climbed to roughly $125 billion with interest expense rising more than 30% year over year.

Legal overhang adds another layer of risk. Several law firms, including Portnoy Law and Howard G. Smith, have launched class action suits tied to disclosures around Oracle’s massive cloud contract with OpenAI and its plans to raise tens of billions in debt for AI infrastructure. While such actions are common in large‑cap tech and may take years to resolve, they increase headline risk and could constrain how aggressively Oracle communicates about future contracts.

Even so, institutional appetite for AI infrastructure remains strong. Commentators on Schwab’s network have highlighted Oracle alongside Microsoft and CoreWeave as key beneficiaries as AI compute demand shifts from theoretical to tangible. Traders on CNBC’s “Final Trades” segment have also called Oracle undervalued after its strong recent quarter, suggesting that some on Wall Street see the selloff as an opportunity.

Related Coverage

For a deeper dive into how recent quarterly numbers are reshaping sentiment, investors can read “Oracle Earnings Record: Can Its AI Cloud Boom Last?”, which explores whether blockbuster AI cloud deals signal a sustainable new era or a stress test for the balance sheet. For context on sector‑wide volatility, “The Trade Desk controversy: -7.5% plunge shocks investors” looks at how shifting digital ad dynamics and AI fears are hitting other high‑growth tech names.

Most of the revenue in this five-year forecast is already booked in our reported remaining performance obligations.— Safra Catz, CEO of Oracle Corporation

Ultimately, the Oracle Forecast to $200 hinges on three levers: sustaining 40%+ cloud growth, converting its $553 billion backlog into revenue and turning today’s heavy capex into positive free cash flow. If Oracle executes on those fronts while defending share against hyperscale rivals, the stock can re‑rate higher in U.S. portfolios; the next few quarters of AI infrastructure ramp‑up will show whether that optimistic Oracle Forecast is on track or needs to be revised.