Can the expanded Palantir Bain Partnership justify Palantir’s sky‑high AI valuation just as the stock slides nearly 5%?

What does the Bain deal change for Palantir?

The core of the expanded Palantir Bain Partnership is simple: Bain brings strategic and industry consulting muscle; Palantir supplies the enterprise AI infrastructure. Bain confirmed it is extending and deepening its lead management consulting alliance with Palantir to meet rapidly growing client demand for AI transformation. The firms will jointly deliver end‑to‑end AI use cases, from strategy design through full operational rollout, using Palantir’s AIP and Foundry platforms and Palantir’s Forward-Deployed Engineers embedded at clients.

These platforms are already used by major multinationals to run real-time, AI-driven operations. By scaling the partnership, Bain aims to make Palantir’s enterprise AI stack a default option for large organizations seeking data-driven decision-making, cost efficiencies, and productivity gains. For Palantir, that effectively adds a global, blue‑chip consulting salesforce on top of its own go‑to‑market teams.

How big could this be for revenue and margins?

Wall Street will get its next hard datapoint on May 4, 2026, when Palantir is expected to report quarterly earnings. Consensus currently calls for EPS of $0.26, up from $0.13 a year earlier, and revenue of about $1.54 billion versus $883.86 million year over year. Those estimates imply rapid top-line growth and scaling profitability, and the enlarged Palantir Bain Partnership is likely one reason analysts feel comfortable modeling continued momentum in commercial AI adoption.

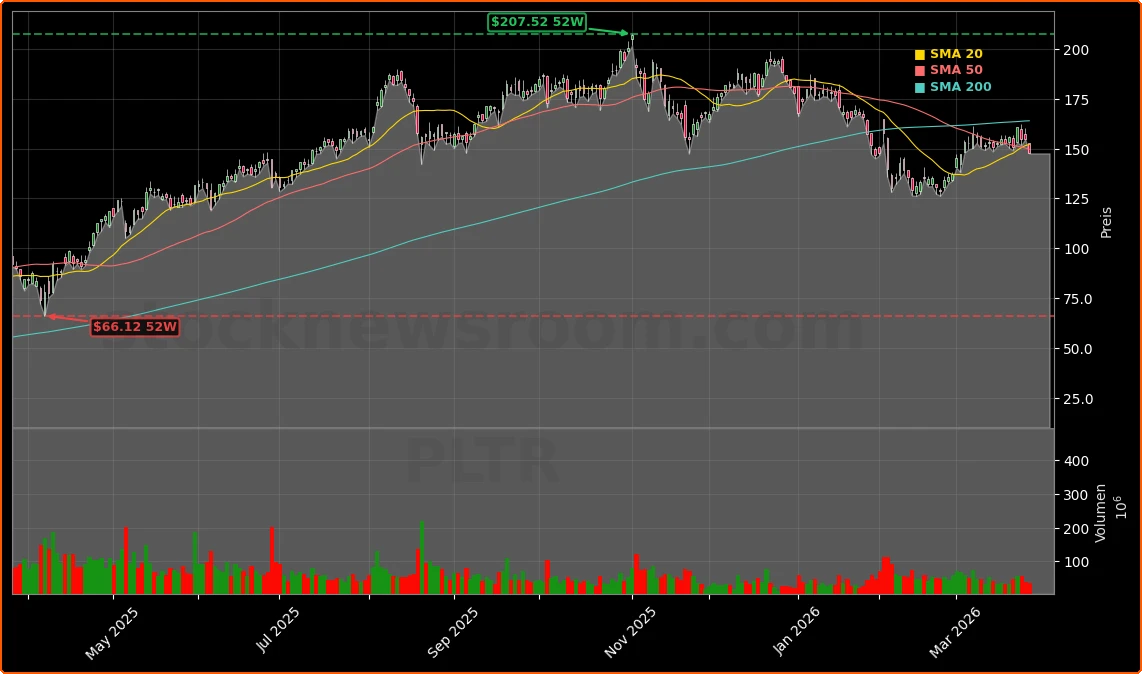

The stock, however, already reflects a lot of good news. At roughly $147.84, Palantir trades at an estimated P/E near 246x, far above most software peers and even above many high‑growth AI names. While some recent commentary suggests the stock may be in a corrective phase after a massive run from the mid‑20s to well above $100, the Bain expansion adds a clear argument that Palantir’s addressable market is still broadening. The risk is that execution has to remain nearly flawless to support this kind of multiple.

How does Palantir stack up versus other AI leaders?

For U.S. investors, the Palantir Bain Partnership sits within a broader AI re‑rating across the NASDAQ. AI chip leader NVIDIA and cloud-focused giants like Amazon dominate the infrastructure layer, while Palantir competes at the enterprise software and decision-intelligence tier. Recent comparisons have even framed Palantir as relatively “cheap” on a price‑to‑sales basis next to smaller, early‑stage quantum names, despite Palantir itself trading at a lofty P/S around the 90x area.

Independent analysis of the enterprise AI race highlights Palantir’s differentiated position: deep U.S. government relationships, rapidly growing commercial revenue, and a debt‑free balance sheet with substantial cash. At the same time, competition is intensifying, from hyperscalers such as Microsoft and Alphabet to specialist software platforms. Commentary from Seeking Alpha underscores that Palantir’s old narrative as a niche defense analytics shop is giving way to one of broad-based enterprise AI infrastructure, with U.S. commercial revenue now outgrowing government by more than 2x and management guiding for over $3.1 billion in revenue by FY 2026.

What signals are analysts sending on PLTR?

Despite Thursday’s roughly 4.6% decline from a previous close of $154.46, analyst sentiment remains firmly positive. The average Wall Street price target stands near $195.23, with several high‑profile calls reinforcing the bull case. Rosenblatt Securities reiterates a Buy rating with a $200 target, UBS also rates the stock Buy and recently lifted its target to $200, and Wedbush maintains an Outperform rating with one of the highest targets on the Street at $230.

Other research shops take a more balanced view, noting that while Palantir is emerging as a central enterprise AI platform, its valuation leaves little margin for error. Zacks, for example, highlights both strengths – such as accelerating commercial adoption and sticky government contracts – and challenges including rich pricing and competitive pressure. Still, the latest analyst activity suggests that the market sees the expanded Palantir Bain Partnership, along with new deals in sectors like defense and financial services, as incremental support for long‑term growth.

What other growth levers are in play?

Beyond consulting-led deployments, Palantir is pushing industry‑specific platforms that could benefit from the Bain alliance. A recent agreement with Moder to build an AI‑powered mortgage operations platform for Freedom Mortgage blends Palantir’s data and AI capabilities with domain expertise to automate complex, rules‑based workflows. That kind of vertical solution is exactly the type of repeatable, high‑value use case Bain can help scale across its client base.

Separately, Palantir is expanding its role in defense and industrial AI. A broadened collaboration with GE Aerospace applies Palantir tools to the U.S. Air Force and GE’s production system to address supply bottlenecks and boost efficiency, reinforcing the company’s relevance in mission‑critical environments. Other initiatives, including AI‑driven surveillance and compliance tools for prediction market platform Polymarket, show how Palantir is moving deeper into financial and digital-asset risk use cases.

Even as chipmakers and megacap tech names weighed on the S&P 500 and NASDAQ this week, software‑centric AI names like Palantir, Apple and select cloud players have drawn interest from investors looking for the next phase of AI upside once hardware demand normalizes. Market strategists on Schwab Network recently argued that the AI theme is temporarily on hold due to macro uncertainty but likely to resume with a fresh wave of software‑driven innovation, a backdrop that would clearly favor Palantir if it can keep executing.

Related Coverage

For a closer look at how Palantir’s recent numbers intersect with its volatile share price, read our earnings-focused piece “Palantir Earnings: -4.0% Plunge After Record-Breaking Q4”, which examines whether blockbuster growth can sustain today’s valuation. Investors interested in how AI consulting and platform strategies compare across the sector may also want to review “Salesforce Agentic Strategy +1.7% Surge on AI Deals”, where we analyze how Salesforce’s government-focused AI push stacks up against rivals in the race for enterprise AI dominance.

AI demands business transformation, not just technology implementation, and that’s precisely what makes the Bain and Palantir partnership so powerful.— Christophe De Vusser, Worldwide Managing Partner, Bain & Company

In sum, the expanded Palantir Bain Partnership strengthens Palantir’s distribution and deepens its role as a core enterprise AI supplier, even as the stock trades at a demanding multiple after an extraordinary run. For U.S. investors, the deal reinforces the company’s long‑term growth story but also raises the stakes on execution heading into the May earnings report. The next quarters will show whether this partnership converts into durable, high‑margin revenue capable of supporting Palantir’s premium valuation.