Can blockbuster Palantir Earnings and surging AI demand justify the stock’s rich valuation as the share price suddenly reverses course?

Is the Palantir Earnings rally running into resistance?

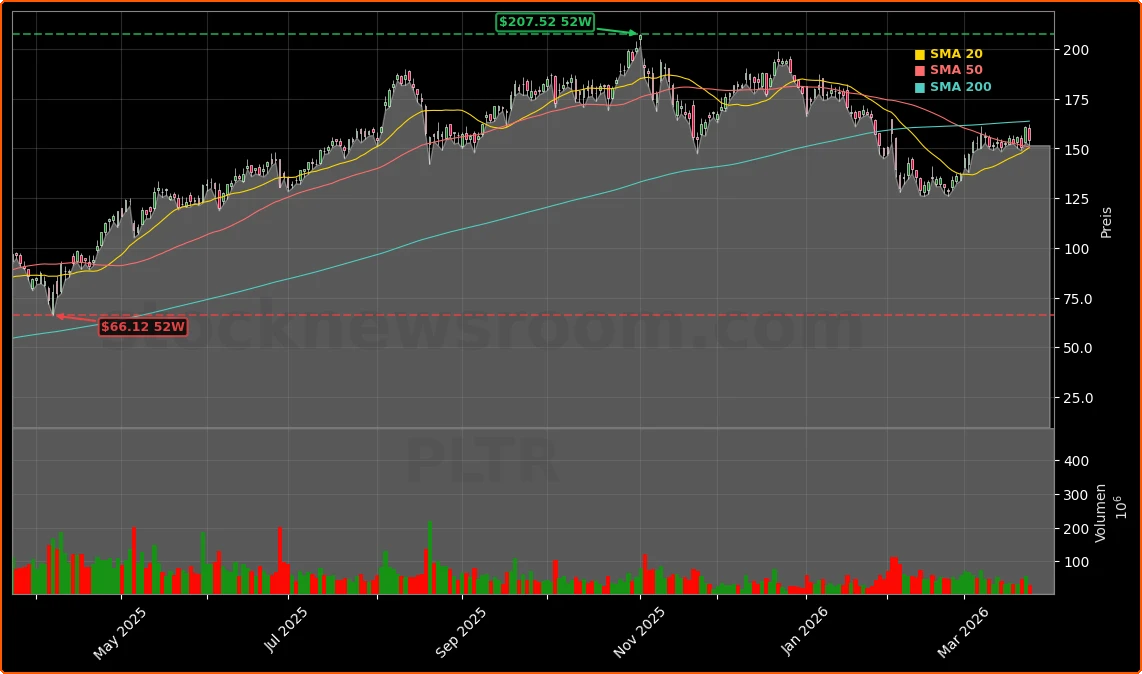

The latest slide in Palantir shares comes after an extended run that left the stock highly sensitive to macro shocks and sentiment swings. At roughly $154.50 in Tuesday afternoon trading (ET), PLTR is giving back part of a powerful multi-month move that still leaves the stock up strongly over the past year, even after a recent consolidation. Technical traders point to the $150 region as an important support zone, with the 200-day moving average and the $164–$165 band acting as a key resistance area in the short term.

The market action is occurring against the backdrop of stellar Palantir Earnings from Q4 2025. Revenue of $1.406 billion grew 70% year over year and beat consensus by nearly 6%, while free cash flow surged to $791 million. Management highlighted a Rule of 40 score of 127%, signaling an unusual blend of high growth and profitability for a software company at Palantir’s scale. Yet high-multiple names tend to be hit hardest when fear rises, and PLTR is proving no exception.

What did Palantir Earnings reveal about AI demand?

Beneath the headline numbers, the composition of Palantir Earnings is what excites many growth investors. U.S. commercial revenue jumped 137% year over year to $507 million in Q4 2025, underscoring how quickly enterprises are adopting Palantir’s AI platforms such as Gotham and Foundry. U.S. government revenue, long the company’s backbone, rose 66% to $570 million, helped by contracts like the Pentagon’s Maven AI program of record, which cements Palantir as a core component of U.S. defense infrastructure.

Management is leaning into this momentum with aggressive guidance. For 2026, Palantir is targeting roughly $7.2 billion in total revenue, implying about 61% year-over-year growth. Within that, U.S. commercial revenue is guided to exceed $3.1 billion, more than doubling from 2025 levels. The company argues that AI-related capital expenditures across industries have not slowed, and that as projects move from pilot to production, they should translate into substantial incremental revenue.

This narrative aligns with the broader AI boom led by names like NVIDIA and large cloud providers. However, unlike many pure software peers, Palantir is already converting AI enthusiasm into large-scale, cash-generative deployments—one reason the stock has historically commanded a premium valuation compared with more mature tech leaders such as Apple.

How are regulators and analysts shaping the story?

Beyond Palantir Earnings, recent contract wins and regulatory scrutiny are shaping perceptions. In the UK, Britain’s Financial Conduct Authority defended its decision to award an AI systems contract to Palantir before lawmakers, stressing that the company will not gain access to sensitive regulatory intelligence. The episode highlights the balance Palantir must strike between lucrative government deals and public concerns over data privacy and surveillance.

On Wall Street, analysts remain broadly constructive but increasingly vocal about valuation risk. Truist Securities recently reiterated a Buy rating on Palantir Technologies Inc. with a price target of $223 after meetings with senior management, arguing that Palantir is emerging as the AI operating system layer for both corporations and governments. UBS also upgraded Palantir to Buy from Neutral, setting a $180 price target and calling the prior share price weakness an attractive entry point, particularly as businesses accelerate AI adoption following due diligence with partners and customers.

At the same time, some research houses highlight that a stock priced for perfection, like Palantir, can be more vulnerable during broad tech selloffs. Zacks Investment Research has noted intense investor interest in PLTR, urging traders to assess both the robust earnings trajectory and the risks stemming from its elevated multiples and sensitivity to shifting expectations.

Does the pullback change the AI investment case?

For U.S. investors comparing AI exposures across portfolios, Palantir sits in a different bucket than mega-cap platform plays such as Tesla or NVIDIA. Palantir’s edge lies in high-stakes data integration, decision intelligence and agentic AI applied to defense, finance, healthcare and increasingly to regulated industries like financial supervision. The recent FCA deal in the UK and expanding Pentagon contracts underscore that Palantir is not merely pitching pilots; it is embedding deeply into mission-critical workflows.

Still, prominent skeptics exist. High-profile investor Michael Burry has reportedly shorted the stock, arguing that a fair value might be far below current levels. Critics point to a history of rich valuation, heavy reliance on government spending and ethical controversies surrounding surveillance and warfare technology. For them, the combination of a premium price tag and geopolitical risk keeps PLTR firmly in the high-volatility camp.

Short-term trading dynamics also matter. Market-wide fear gauges such as the VIX have spiked in recent weeks, and media coverage has highlighted how high-growth tech names—including Palantir and space-related peers like Rocket Lab—are reacting sharply to war headlines and macro uncertainty. In this context, even strong Palantir Earnings are not always enough to offset de-risking flows when investors are reducing exposure to richly valued AI stories.

Related Coverage

Investors interested in how Palantir is pushing deeper into financial services should read Palantir Mortgage Platform Boom: AI Shock For Mortgage Lenders, which explores how a new mortgage platform partnership could open another major commercial growth avenue. For broader tech-sector context, SAP Forecast Warning as JPMorgan Downgrade Triggers Crash analyzes how a legacy software giant’s guidance cut and downgrade can ripple through valuations across the whole enterprise software and AI landscape, offering useful comparison points for Palantir’s own risk-reward profile.

We are an n of 1, and these numbers prove it.— Alex Karp, CEO of Palantir Technologies Inc.

Palantir Earnings have clearly validated the company’s position as one of the few AI players turning massive data and machine learning investments into rapid growth and strong free cash flow. For long-term investors, the mix of government contract visibility, commercial acceleration and supportive analyst commentary from firms like Truist and UBS keeps the bullish case compelling, even if near-term volatility remains high. The next set of quarterly results and execution against the ambitious 2026 revenue targets will show whether this latest pullback is a buying opportunity or an early warning that expectations have run ahead of reality.