Can the Palantir Maven Program’s new Pentagon status really justify one of the richest AI valuations in market history?

How big is the Pentagon win for Palantir?

Deputy Secretary of Defense Steve Feinberg has directed that Palantir’s Maven digital battle‑management suite become a formal program of record, shifting oversight to the Pentagon’s Chief Digital and Artificial Intelligence Office and assigning future contracting to the U.S. Army. In practical terms, that designation means the Palantir Maven Program is no longer a discretionary experiment, but a funded, baseline capability meant to spread across all branches of the U.S. military.

Maven’s core functions – intelligence fusion, automated target recognition, battlespace awareness and decision support – sit squarely at the center of modern drone and missile warfare in Ukraine and the U.S./Israel conflict with Iran. As battlefield commanders lean more heavily on AI‑driven targeting and sensor fusion, Palantir’s software becomes deeply embedded in day‑to‑day operations, making it politically and operationally difficult to rip out.

For shareholders, that integration translates into higher visibility on multi‑year license, support and upgrade streams funded directly from the base defense budget rather than ad‑hoc programs. It also positions Palantir as a front‑runner for complementary initiatives such as the Trump administration’s proposed “Golden Dome” air and missile defense shield, where a common data and targeting layer will be critical.

What does this mean for Palantir’s growth profile?

Even before the Palantir Maven Program upgrade, government work was the company’s deepest moat. The U.S. federal segment has long been a growth engine, with Palantir’s platforms handling intelligence, counterterrorism, and logistics for agencies from the CIA to the Department of Defense. Maven’s elevation takes that relationship a step further: instead of winning one‑off battlefield contracts, Palantir is now at the heart of how the Pentagon wants to operationalize AI across domains.

At the same time, management has pushed aggressively into commercial markets via its AI Platform (AIP) and Foundry, landing enterprise wins in health care, financial services and insurance. A notable example is an underwriting partnership in which AIG integrates Palantir’s Foundry to drive data‑driven risk analysis, highlighting how defense‑grade data tooling can migrate into traditional industries.

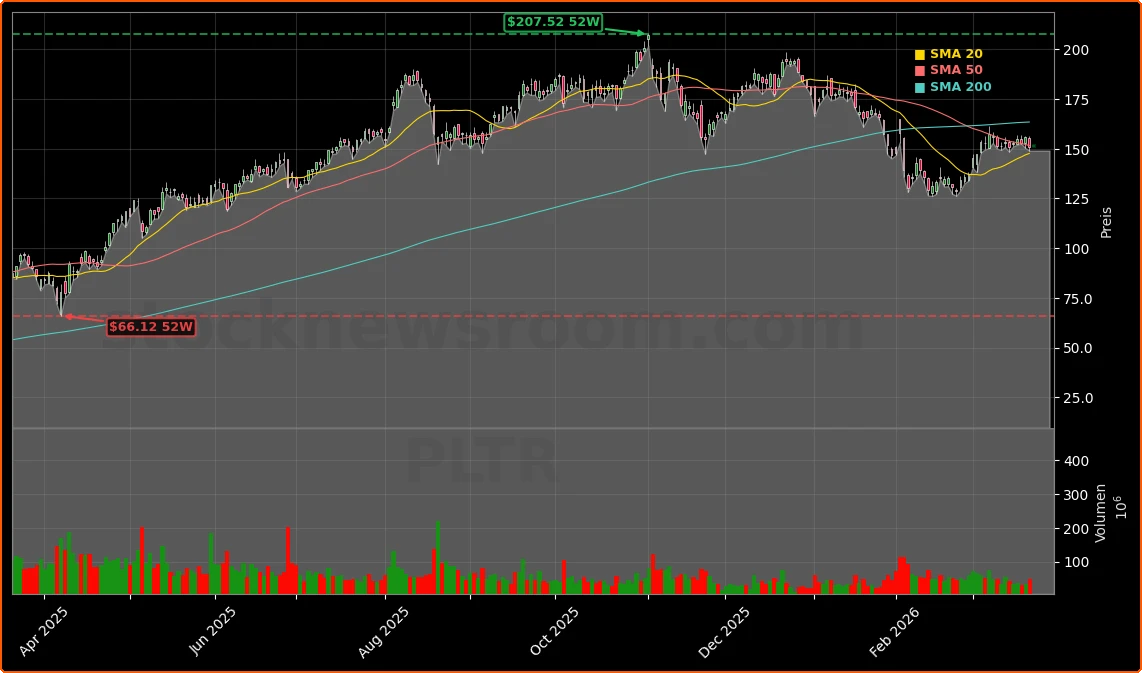

Wall Street is rewarding that execution. PLTR gained 167% in 2023, 340% in 2024 and 135% in 2025. Even after sliding about 15% year‑to‑date and closing Friday at $150.68 (down 3.21% on the day, with after‑hours trading at $151.96), Palantir still carries one of the strongest technical profiles on the market, with an IBD Composite Rating of 94 out of 99 and a solid B Accumulation/Distribution score indicating ongoing institutional interest.

Can valuation stay this high for Palantir?

Palantir’s stock now trades at roughly 87 times trailing sales, with a market cap near $370 billion on about $4.5 billion of annual revenue, making it the most expensive name in the S&P 500 by price‑to‑sales. Historical data on the index is sobering: out of more than 200 companies that have ever traded above 25 times sales, only a small minority managed to outperform the market over 3‑, 10‑ and 20‑year windows. At valuation levels north of 80 times sales, the bar for sustaining outperformance is “in the stratosphere.”

That disconnect fuels persistent skepticism from valuation‑sensitive analysts at firms like Citigroup and RBC Capital, who point out that even if Palantir doubled revenue tomorrow, the stock would still sit among the most richly priced in S&P 500 history. The bear case argues that as hyperscalers and enterprise giants pour billions into AI – think NVIDIA at the chip layer, Apple building on‑device models, or Microsoft and Google in cloud AI – Palantir’s ability to sustain 40%–50% top‑line growth will inevitably moderate.

Bulls counter with the company’s differentiated ontology layer, which Morgan Stanley recently highlighted as a lasting edge because it creates a “digital twin” of complex organizations and dramatically accelerates deployment of new AI workflows. They also emphasize that defense and intelligence workloads are structurally less price‑sensitive and far stickier than typical SaaS deployments, giving Palantir more room to grow into its multiple than most software names have enjoyed historically.

How does Palantir stack up against AI peers?

On Wall Street, Palantir is increasingly grouped with high‑beta AI winners rather than with legacy defense primes. Investors who once chased younger defense‑AI firms like BigBear.ai are now gravitating to Palantir as a more scaled, better capitalized alternative. Broad market commentators have even highlighted PLTR alongside momentum names such as Tesla as AI‑levered plays that have shrugged off bouts of macro volatility.

For long‑only U.S. investors building AI exposure, Palantir sits in a distinct bucket from chipmakers like NVIDIA or consumer platforms like Apple. It is essentially an application‑layer defense and enterprise software pure play whose fortunes hinge on two questions: first, how large the long‑term defense AI budget becomes as conflicts in Europe and the Middle East re‑shape procurement; and second, whether commercial adoption of AIP and Foundry can scale into a revenue base commensurate with an S&P 500 mega‑cap.

Trading near its 50‑day and 200‑day moving averages after the recent pullback, PLTR is no longer in free‑fall, but its premium leaves little room for execution missteps, policy backlash, or delays in commercial ramp‑up.

Related coverage: where else is Palantir pushing AI?

Investors who want to understand Palantir’s broader AI ambitions beyond the battlefield should look at its push into financial services and housing. One detailed breakdown is available in “Palantir Mortgage Platform Boom: AI Shock For Mortgage Lenders”, which explores how a new mortgage analytics platform built with Moder could turn the complex, regulated U.S. home‑lending market into Palantir’s next major growth engine.

Sector context also matters. A separate deep‑dive, “The Trade Desk AI Strategy: -74% Plunge and AI Bet”, shows how another high‑growth ad‑tech name is leaning into AI after a severe share price correction. Comparing Palantir’s premium valuation and government‑anchored moat with The Trade Desk’s more cyclical advertising exposure helps investors calibrate risk and reward across very different AI business models.

Bottom line, the Palantir Maven Program upgrade cements Palantir as a central AI supplier to the U.S. military and adds meaningful durability to its government revenue stream. For U.S. portfolios, that makes PLTR one of the clearest pure‑play defense‑AI equities, but also one of the market’s most demanding valuations. The next few quarters of Maven deployment and commercial AI wins will show whether the Palantir Maven Program can generate enough growth and cash flow to justify its lofty place atop the S&P 500’s pricing ladder.