Are Palo Alto Networks Acquisitions building an unbeatable AI‑security platform or just masking growing risks in the core business?

How are Palo Alto Networks Acquisitions shaping the stock?

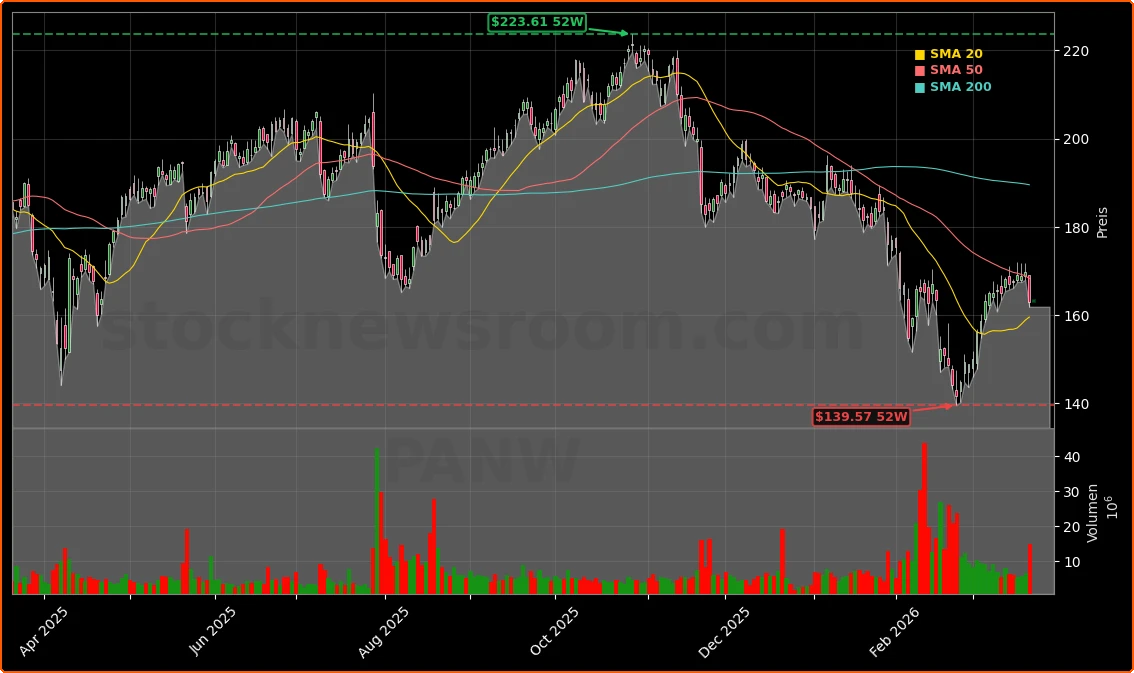

Palo Alto Networks, Inc. (PANW) closed Friday at $162.95, down about 4% from the prior session and modestly above after-hours levels around $163.50. The stock remains well below its 52‑week high, so the latest move is a consolidation rather than a breakout, even as the company leans hard into AI-driven growth. Institutional interest has stayed robust: MassMutual Private Wealth & Trust boosted its PANW stake by more than 260% in Q4, and Allworth Financial LP lifted its holdings by nearly 47%, helping push institutional ownership close to 80%.

Analysts broadly see long-term upside. MarketBeat data show an average “Moderate Buy” rating from more than 40 Wall Street firms and a consensus 12‑month price target above $210, implying meaningful upside from current levels. That optimism, however, rests heavily on whether the latest wave of Palo Alto Networks Acquisitions can add enough revenue growth and product depth to offset integration costs and pressure on earnings per share.

What does Protect AI bring to Palo Alto Networks?

The first major AI-security deal in this cycle was Protect AI, acquired in July 2025. Founded in 2022, Protect AI marketed itself as a full life‑cycle security solution for generative AI applications and machine learning models. The technology is designed to secure model development pipelines, training data, inference endpoints, and monitoring, areas that increasingly worry enterprises deploying large language models from providers that run on chips from companies like NVIDIA.

Palo Alto Networks plans to weave Protect AI into its Prisma AI Risk & Security (AIRS) platform, creating a broader AI security fabric that can be sold across its global customer base. Management argues that enterprises do not want point tools for every step of the AI pipeline, but rather a unified platform that can scale across cloud providers and on‑premise environments. If executed well, this acquisition can increase average deal sizes and attach rates as customers standardize AI defenses with one vendor.

Why was Chronosphere a strategic purchase?

Chronosphere, acquired in January 2026, adds cloud‑native observability and monitoring capabilities. Since launching in 2019, it has positioned itself as a way for developers and operations teams to detect and resolve application and infrastructure issues before they escalate. For Palo Alto Networks, the rationale is clear: the more telemetry it can ingest from apps, infrastructure and AI systems, the better its security analytics and automated responses can become.

By integrating Chronosphere into its cloud security portfolio, Palo Alto Networks aims to give customers real‑time insight into performance, anomalies and potential threats in complex Kubernetes and microservices environments. That could make its platform more competitive against observability players and larger security suites from rivals that, like Apple in consumer devices, try to lock users into a tightly integrated ecosystem. For investors, the Chronosphere deal underlines that Palo Alto Networks Acquisitions are not just about headline AI buzzwords, but also about deeper data and visibility layers that can support long‑term recurring revenue.

How does CyberArk change the competitive landscape?

The most visible of the recent Palo Alto Networks Acquisitions is CyberArk, a former public company specializing in identity security and privileged access management. CyberArk generated roughly $1.3 billion in revenue in 2025 but remained loss‑making on an operating basis. Palo Alto Networks intends to keep CyberArk’s platform available as a stand‑alone offering while tightly integrating its credential, session and privilege controls into the broader product stack.

Strategically, this pushes PANW deeper into an identity segment often associated with rivals like Okta and Microsoft. As AI agents and machine-to-machine communications proliferate, securing every identity — human, machine and autonomous agent — becomes a core pillar of enterprise security. This move could help Palo Alto Networks compete more directly for zero-trust and identity budgets, a space where some analysts currently see an edge for Okta in the near term. The trade-off is that absorbing a large, previously independent platform will likely weigh on margins and complicate integration over the next several quarters.

Is the valuation justified by growth prospects?

Palo Alto Networks reported about $1.1 billion in net income in fiscal 2025 and continues to post strong top-line growth, with its latest quarter beating consensus EPS and revenue expectations. Even so, the stock trades at a forward price-to-earnings ratio in the mid‑40s, well above the broader S&P 500 and higher than some cybersecurity peers. Research firms note that acquisition-related costs, equity dilution and integration risk could pressure earnings, a concern already reflected in recent share volatility and technical signals pointing to downside risk toward the $158 support area.

On the other hand, the addressable market is expanding rapidly. Industry forecasts see global cybersecurity spending rising from a little over $200 billion in 2025 to close to $700 billion by 2034, driven by cloud migration, generative AI, and a growing attack surface from connected devices and autonomous systems, including vehicles from names like Tesla. If Palo Alto Networks successfully integrates Protect AI, Chronosphere and CyberArk, it could emerge as one of the most comprehensive security platforms for the AI era.

Our customers are moving quickly to adopt AI and are asking for a partner who can secure their entire AI ecosystem at scale.— Anand Oswal, EVP Network Security at Palo Alto Networks

For U.S. investors, the key issue is timing. The current dip may offer an entry point for those comfortable with short‑term earnings volatility and integration risk. With Wall Street still largely positive and institutional money increasing exposure, the Palo Alto Networks Acquisitions strategy positions the company to capture a larger slice of AI‑driven cybersecurity demand. The next few quarters will show whether that bet can translate into sustained revenue acceleration, margin resilience and renewed share price momentum on the NASDAQ.