Is the latest Palo Alto Networks CEO Purchase a bold $10 million conviction call or just noise in an AI‑shaken cyber market?

Why does this Palo Alto Networks CEO Purchase matter now?

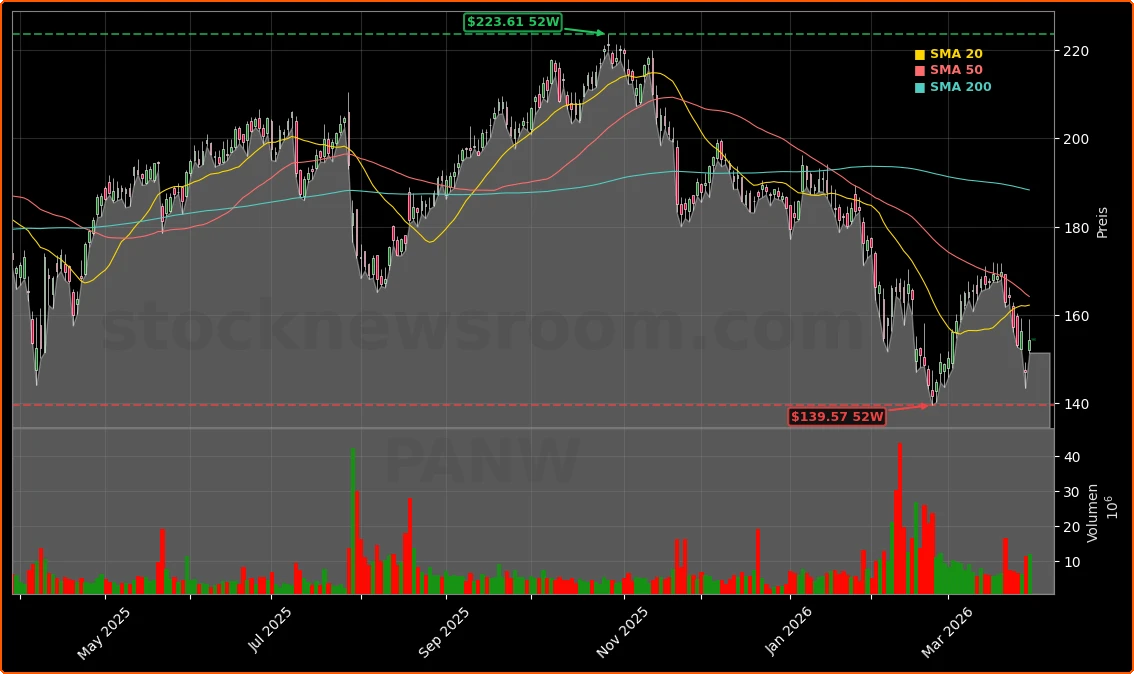

Timing is everything with insider buying, and the latest Palo Alto Networks CEO Purchase comes at an especially fragile moment for software and cybersecurity valuations on Wall Street. Palo Alto Networks stock has been hit hard in 2026, sliding about 15% year to date and trading roughly 30% below its all‑time closing high of $221.38 from October 28, 2025. Monday’s close at $154.35, with a modest uptick to about $154.50 in after‑hours trading, still leaves the stock well under its 52‑week high of $223.61 and only about 9–10% above its 52‑week low.

Against that backdrop, the company disclosed that CEO Nikesh Arora bought 68,085 shares on March 27 at prices between roughly $146.46 and $147.48, committing about $10 million of his own capital. It is his first open‑market purchase since November 2019 and adds about 6.6% to his direct stake. The announcement helped spark a roughly 5–6% rally on Monday, putting Palo Alto among the top gainers in both the S&P 500 and the Nasdaq 100.

Insider buying on this scale is relatively rare for mega‑cap software names and is often interpreted as a vote of confidence that the current share price undervalues long‑term prospects. For a sector grappling with fears that rapidly improving AI models could upend legacy business models, having the CEO step in as a large buyer stands out.

How is AI reshaping sentiment on Palo Alto Networks?

The Palo Alto Networks CEO Purchase lands squarely in the middle of a volatile debate: is AI a threat to cybersecurity vendors or their greatest growth catalyst in a decade? The most recent wave of selling in cyber stocks was triggered by new information around Anthropic’s upcoming Claude Mythos model and earlier AI tools capable of scanning code for vulnerabilities. Traders briefly extrapolated this into a world where AI systems could automate and commoditize core security functions, putting pressure on companies like Palo Alto Networks, CrowdStrike, Okta and Zscaler.

On Friday, PANW fell around 6% intraday before the insider buying disclosure helped stabilize sentiment. By Monday, the stock clawed back nearly all of those losses, and peers such as CrowdStrike and Okta were up 3–4% as investors reassessed the actual competitive threat. A key pushback came from Bernstein analyst Peter Weed, who argued that Anthropic is not entering the cybersecurity software business and that more capable AI models are being hardened against misuse rather than built to displace dedicated security platforms.

Arora has been vocal about this point. On the company’s Q2 FY2026 earnings call, he emphasized that as AI spreads across the enterprise, it “expands the attack surface area” and creates new classes of risk. In his view, more AI equals more infrastructure, more machine‑to‑machine activity, and therefore more need for consolidated, intelligent security platforms. His blog post on Monday went a step further, calling this period the industry’s “most consequential moment” and urging AI labs and cybersecurity firms to work together rather than operate at cross purposes.

What exactly did the Palo Alto Networks CEO buy?

Details of the transaction matter for investors parsing the Palo Alto Networks CEO Purchase as a signal. A Form 4 filed with the SEC shows that on March 27, Arora bought 100 shares at $147.48 and 67,985 shares at an average price of about $146.87, totaling 68,085 shares and roughly $10 million in value. Following the transaction, he directly owns more than 340,000 shares, with additional indirect holdings through investment entities and an annuity trust.

Importantly, Arora’s prior SEC filings have been dominated by stock sales, often tied to exercising options and covering tax obligations on vested restricted stock units. That pattern is common among Silicon Valley executives but can be a red flag for some investors. A large, discretionary open‑market purchase breaks that pattern and hints that the CEO sees an attractive risk‑reward profile at current levels, especially given that PANW is down roughly 20–30% from its late‑2025 highs even as fundamentals have remained solid.

Valuation, however, is not trivial. Even after the latest drop, the stock still trades at premium multiples—around 33 times free cash flow and more than 90 times trailing earnings by some estimates, with consensus long‑term EPS growth projections near the low‑teens percentage range. That disconnect has led some commentators to warn that Palo Alto could be priced for perfection. Arora is effectively signaling that the Street underestimates either the growth trajectory or the durability of margins as the platform strategy matures.

How strong are Palo Alto Networks’ fundamentals?

Recent results help explain why the insider purchase was welcomed by Wall Street. In Q2 FY2026, Palo Alto Networks reported revenue of $2.594 billion, up about 14.9% year over year and ahead of expectations. Non‑GAAP EPS of $1.03 beat consensus estimates around $0.94, while net income jumped more than 60% year over year to roughly $432 million. Non‑GAAP operating margin held above 30% for a third consecutive quarter at 30.3%, underscoring healthy operating leverage even as the company continues to invest heavily in AI and platform expansion.

The growth engine remains its Next‑Generation Security portfolio, with annual recurring revenue (ARR) climbing to $6.3 billion, up 33% from a year earlier. Management expects NGS ARR to reach between $8.52 billion and $8.62 billion for the full year, implying 53–54% growth—a striking acceleration versus headline revenue. Remaining performance obligations stand around $16 billion, up more than 20% year over year, providing solid visibility into future top‑line trends.

Cash and equivalents of about $4.2 billion give the company ample balance sheet flexibility, which it has been using aggressively. Recent deals include the acquisition of Israeli identity‑security specialist CyberArk and the purchase of AI observability platform Chronosphere for more than $3.3 billion, both aimed at deepening its platform coverage from identity to telemetry. That strategy puts Palo Alto in more direct competition with both pure‑play security vendors like CrowdStrike and broader cloud ecosystems from NVIDIA, Apple and others that are embedding security and observability deeper into their stacks.

What are analysts saying about Palo Alto Networks?

Sell‑side sentiment remains broadly positive despite this year’s correction. Of roughly 56 analysts covering the stock, more than 40 rate Palo Alto a “Buy” or “Strong Buy,” while only a small handful carry “Sell” ratings. Consensus 12‑month price targets cluster around $205–$210, implying substantial upside from Monday’s close if the company executes on its growth outlook and AI investments.

Institutional research shops have been quick to frame the Palo Alto Networks CEO Purchase as a confidence booster. Baird, for example, described the $10 million buy as a “very strong” signal in a market that has arguably overreacted to AI headlines. Meanwhile, Trivariate Research and others have highlighted Palo Alto as one of the higher‑quality tech names that may look optically expensive but still offer compelling long‑term earnings power, particularly versus slower‑growth “value trap” software stocks.

At the same time, some firms urge caution on valuation. Commentary from platforms such as The Motley Fool underscores that Palo Alto trades at rich multiples relative to its expected five‑year EPS growth in the low teens, suggesting less margin for error if AI spending cycles or enterprise IT budgets slow. Investors will be watching Q3 guidance closely; management is projecting revenue growth to accelerate to roughly 28–29%, a sharp jump from Q2’s 15%. If that step‑up materializes, it would help validate the bullish stance behind Arora’s purchase.

How does this affect the broader cybersecurity sector?

The impact of the Palo Alto Networks CEO Purchase has spilled over into the wider cyber complex. On Monday, major security names including CrowdStrike, Okta, Fortinet and Zscaler all traded higher, clawing back some of last week’s AI‑driven losses. The sector had already been under pressure from a broader software selloff tied to fears that AI could automate significant portions of application and infrastructure management.

Yet cybersecurity is one of the few software categories where AI may be structurally additive. As AI models grow more powerful, they not only become potential tools for attackers but also generate new workloads and data flows that must be monitored, segmented and secured across clouds and edge environments. Palo Alto’s platformization bet—consolidating point solutions into integrated suites spanning network, cloud, identity and observability—is aimed squarely at this complexity problem.

Competitively, Palo Alto continues to square off against fast‑growing endpoint and XDR players like CrowdStrike, identity specialists such as Okta, and cloud‑security‑first vendors including Zscaler. Large platform players, from hyperscalers to AI chip leaders like NVIDIA, are also embedding more security primitives into their offerings. For US investors constructing tech portfolios, the key question is whether Palo Alto can maintain enough innovation velocity and cross‑sell momentum to justify its valuation premium versus this increasingly crowded field.

Palo Alto Networks CEO Purchase: signal or noise for investors?

For portfolio managers, the main task is to interpret whether the latest Palo Alto Networks CEO Purchase is a durable inflection point or just a short‑term sentiment boost. Historically, sizeable insider buys by top executives have correlated with above‑average forward returns in many S&P 500 names, particularly when they occur after drawdowns rather than at all‑time highs. In this case, Arora is stepping in after a roughly 20–30% decline from peak levels, while underlying demand indicators like NGS ARR and remaining performance obligations remain robust.

Still, the stock is not cheap on traditional metrics, and investors need to be comfortable underwriting both sustained double‑digit growth and a successful integration of recent acquisitions. Margin guidance for FY2026 was nudged lower, partly due to integration costs and higher memory and storage expenses, reminding the market that building a broad, AI‑ready platform is capital intensive. Execution missteps or a slowdown in AI‑driven security spending could quickly re‑open the valuation debate.

For now, the CEO’s checkbook aligns with the bullish view that AI is a net positive for cybersecurity. If enterprises indeed treat AI as mission‑critical infrastructure, demand for highly automated, cloud‑delivered security may look more like a utility than a discretionary line item—an attractive backdrop for a scaled platform leader like Palo Alto Networks.

Related Coverage

Investors looking for more context on Palo Alto’s strategy can dig deeper into its dealmaking and AI positioning. Our earlier analysis, “Palo Alto Networks Acquisitions: -4% Crash or Opportunity?”, examines whether recent moves in identity security and observability are building an unbeatable AI‑security platform or simply masking emerging risks in the core firewall and SaaS business. Together with the latest insider buying, that piece helps frame how much of the long‑term AI upside is already priced into PANW shares and where future surprises could come from.

The stakes are high. The window to act is open, and we need to act swiftly with intent, together.— Nikesh Arora, CEO of Palo Alto Networks

In conclusion, the latest Palo Alto Networks CEO Purchase underscores Nikesh Arora’s conviction that AI will enlarge, not erode, the company’s opportunity set. For US investors, the move strengthens the bullish case for Palo Alto Networks as a core cybersecurity holding, albeit one that still carries valuation and execution risks. The next few quarters of AI‑driven deals, platform wins and margin trends will determine whether this $10 million insider bet turns into a new leg higher for PANW or just a brief respite in a volatile AI‑era market.