Is the Plug Power Turnaround finally moving from hype to hard numbers as margins flip positive and hydrogen meets the AI power boom?

Is Plug Power finally changing the narrative?

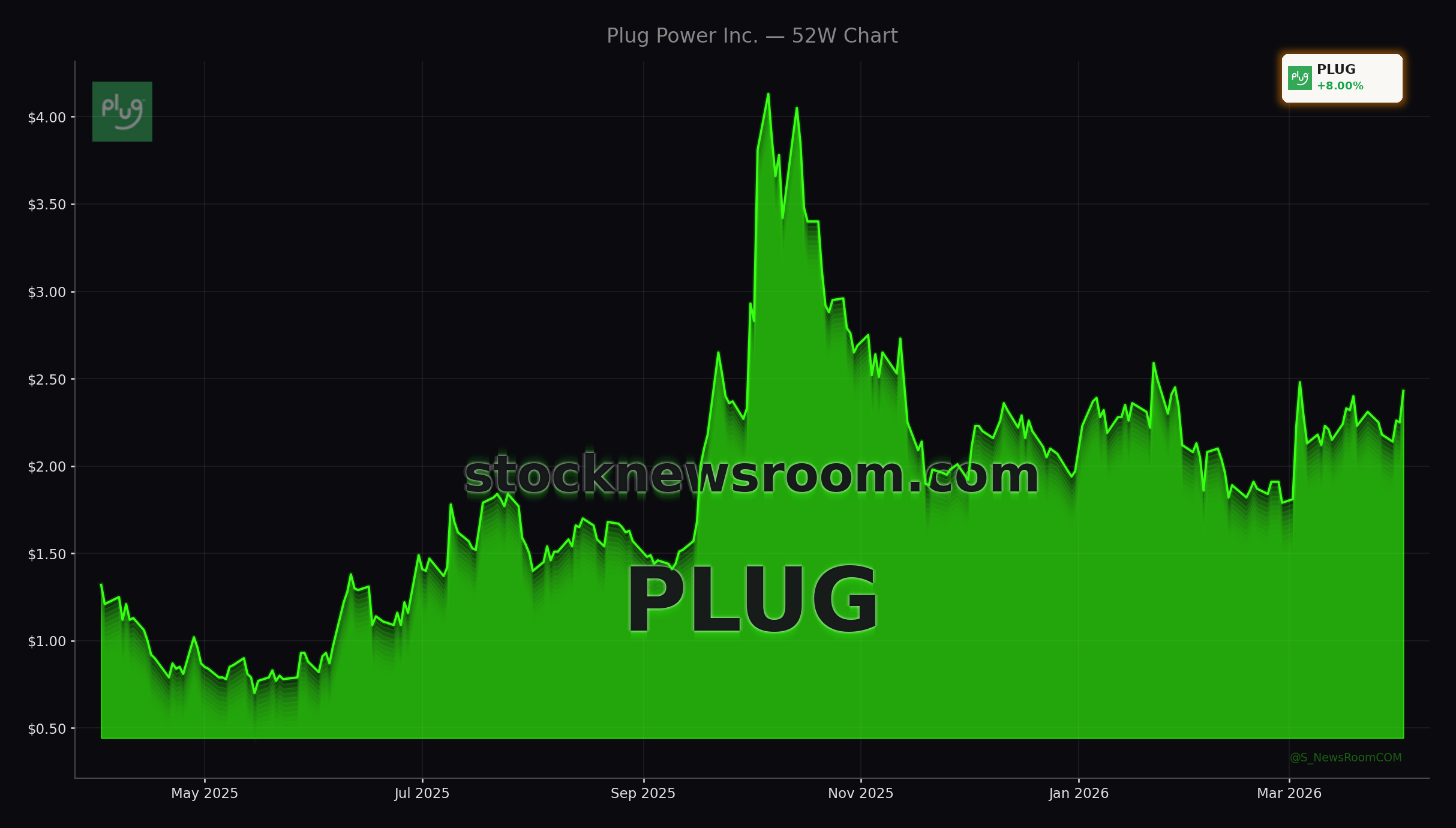

Wall Street has spent years watching Plug Power destroy shareholder value; the stock trades nearly 99% below its reverse-split-adjusted IPO level despite intermittent hype cycles around hydrogen. Today’s bounce to about $2.44, following a 24% gain over the past month, reflects growing belief that this time the Plug Power Turnaround might rest on real operational progress rather than story alone. The company reported Q4 2025 revenue of $225.22 million, up 17.6% year over year and ahead of consensus, but the real milestone was a swing to a positive gross margin of 2.4% from a brutal -122.5% in Q4 2024.

New CEO Jose Luis Crespo has mapped out a profitability road map that targets positive EBITDAS by Q4 2026, positive operating income by the end of 2027, and full profitability by 2028. These timelines remain aggressive, yet for the first time in years Plug Power isn’t losing money on every unit sold. For growth-oriented U.S. investors who already own AI winners like NVIDIA or mega-cap growth names such as Apple, the stock offers a speculative way to add hydrogen exposure that could benefit from the same data-center buildout driving tech multiples higher.

How strong is the operational Plug Power Turnaround?

The Plug Power Turnaround is being driven by a mix of higher volumes, pricing, and cost-cutting under the company’s “Project Quantum Leap” initiative. Management has been trimming manufacturing costs and restructuring operations after a weak 2024, when revenue fell 29% and net losses widened. As demand for hydrogen projects restarted in 2025, Plug Power’s revenue returned to growth, rising 13% for the year and setting the stage for analysts to pencil in an 18% compound annual growth rate through 2028 to about $1.2 billion in sales.

To tackle its chronic cash burn – full-year 2025 operating cash flow was about -$536 million and the accumulated deficit stands near $8.2 billion – Plug Power is executing a capital-release plan targeting over $275 million in asset sales, restricted cash releases, and expense reductions in the first half of 2026. Closing those transactions on time will be a crucial test of whether the Plug Power Turnaround can move from margin repair to balance sheet stabilization. With an enterprise value around $3.7 billion, the stock trades at roughly five times this year’s expected sales, a level that could expand sharply in a hotter risk-on market if execution improves.

Can AI data centers supercharge Plug Power’s hydrogen pivot?

Beyond the internal fixes, the more compelling angle for U.S. investors is Plug Power’s attempt to reposition itself at the junction of green hydrogen and AI-driven power demand. Management is targeting hydrogen-fueled electricity assets that can support AI and cloud data centers through the PJM Interconnection grid, effectively pitching hydrogen as a flexible, low-carbon backup or supplementary source for energy-hungry server farms. While NVIDIA and other chipmakers capture most of the AI headlines, that buildout requires enormous amounts of reliable power, creating an opening for alternative energy suppliers.

Plug Power is simultaneously expanding its global electrolyzer footprint. The company just secured a Front-End Engineering Design contract to supply a 275 MW GenEco PEM electrolyzer system for Hy2gen’s “Courant” low-carbon ammonia and explosives project in Baie-Comeau, Québec. The Canadian facility will use low-carbon electricity from Hydro-Québec to produce renewable ammonia and ammonium nitrate for the mining industry, underscoring Plug Power’s role as a partner for industrial decarbonization. Combined with an $8 billion global sales funnel spanning Europe, Australia, and North America, these large-scale projects give the Plug Power Turnaround a more substantial foundation than past cycles built mainly on warehouse fuel-cell deployments.

What are the legal and macro risks for Plug Power investors?

The bullish Plug Power Turnaround story still competes with a formidable bear case. Multiple securities class actions have been filed in U.S. courts, alleging that Plug Power misled investors about the likelihood of receiving a $1.66 billion Department of Energy loan guarantee and its capacity to build hydrogen production facilities at scale. Law firms including Pomerantz LLP, the Law Offices of Frank R. Cruz, Rosen Law Firm, Faruqi & Faruqi, and Bronstein, Gewirtz & Grossman are all seeking lead plaintiffs ahead of an April 3, 2026 deadline, keeping legal risk front and center for institutional buyers.

On the macro side, Plug Power has recently benefited from falling U.S. Treasury yields, which tend to boost long-duration growth stocks by lowering the discount rate on future cash flows. Hydrogen names have also caught a bid as investors look for ways to play rising global energy demand beyond traditional oil and gas majors like Exxon Mobil or integrated renewables players that compete with Tesla’s energy segment. Yet over a five-year horizon Plug Power shares are still down roughly 93%, and the stock remains a high-beta, high-volatility component in any U.S. portfolio.

Related Coverage

For a deeper dive into whether the first positive gross margin can truly ignite a durable Plug Power Turnaround, readers can review our earlier analysis in “Plug Power Turnaround: -2.7% Shock After First Margin Boost”, which examines Wall Street’s initial skepticism after the margin inflection. Investors comparing hydrogen to traditional energy exposure may also want to read “ExxonMobil Plunge -5.9%: War Risk Reset or LNG Upside?”, which discusses how shifting war risk premiums and LNG dynamics are reshaping views on Big Oil relative to energy-transition plays.

By leveraging our strong commercial foundation, advancing cost-efficiency initiatives, and capitalizing on our more than $8 billion global sales funnel, we are converting operational momentum into sustainable financial performance.— Jose Luis Crespo, CEO of Plug Power

In the end, the Plug Power Turnaround now rests on more than just hope: the company has delivered its first positive gross margin, secured major electrolyzer projects, and outlined a credible path toward AI data-center demand. For U.S. investors comfortable with elevated risk, the stock offers leveraged exposure to both the hydrogen theme and the broader power needs of the AI era. The next key catalysts will be successful completion of the $275 million asset monetization plan and continued margin improvement, which will determine whether Plug Power can turn today’s bounce into a sustained recovery.