Is the Plug Power Turnaround finally real, or just another head-fake in one of Wall Street’s most volatile clean-energy stories?

Is Plug Power really at an inflection point?

For years, Plug Power has been a classic high-beta clean energy name on the NASDAQ: huge addressable market, heavy losses, and recurring dilution. That narrative is changing at the operating level. In Q4 2025, the company posted a positive gross margin of 2.4%, a dramatic swing from negative 122.5% a year earlier. Management has called this a meaningful milestone that signals an inflection in how its hydrogen production, fuel cell and electrolyzer platform scales.

The move into positive gross margin territory was driven by lower service costs, better efficiency in the hydrogen production network and scale benefits as the installed base grew. Plug Power has now deployed more than 72,000 fuel cell systems across over 275 fueling stations, generating about $710 million in 2025 revenue, including $225.2 million in Q4 alone. The numbers don’t make Plug profitable yet, but they anchor the emerging Plug Power Turnaround narrative in hard data instead of just future promises.

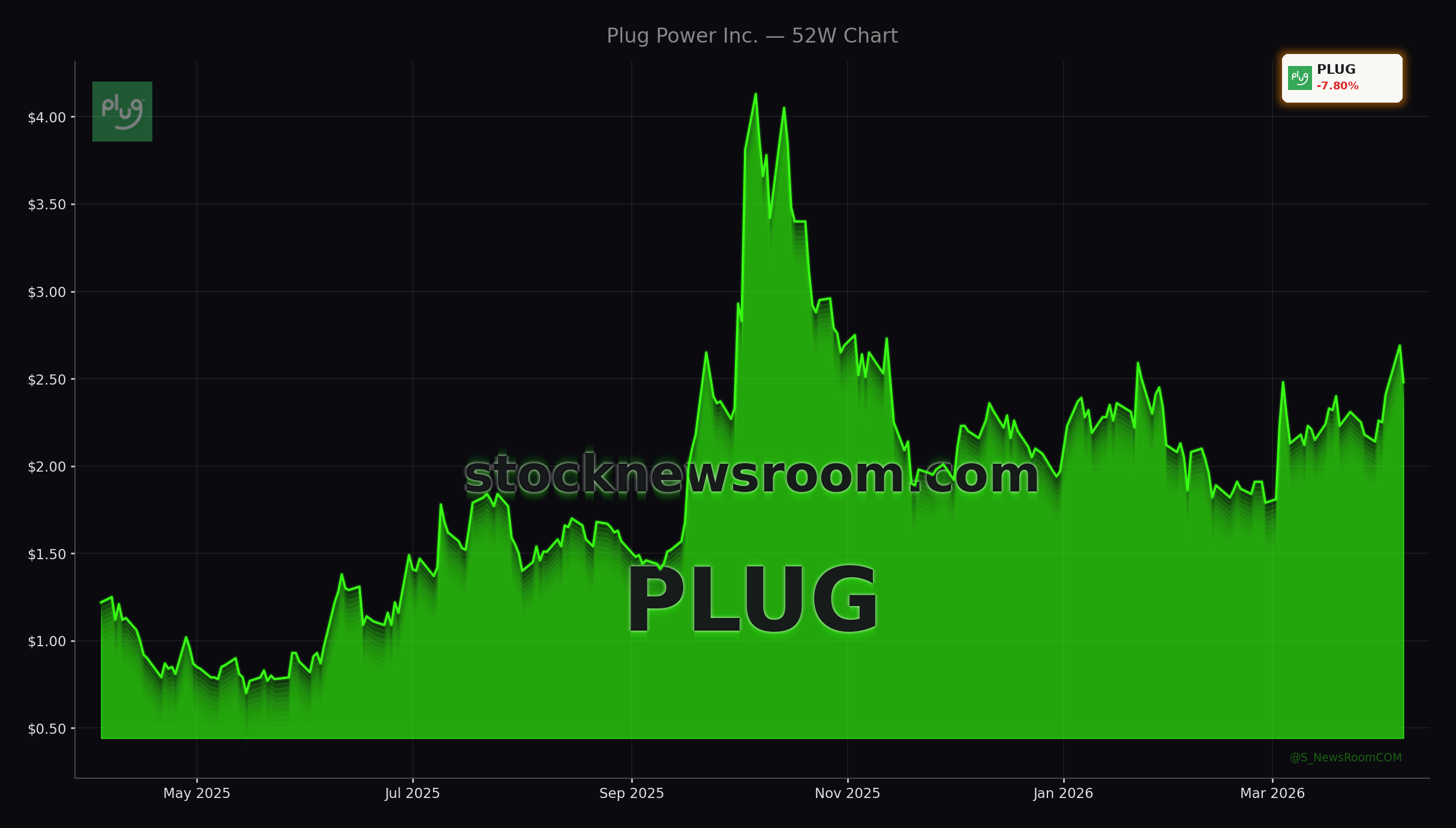

Wall Street’s reaction remains cautious. PLUG has rallied sharply off its late‑2025 lows but continues to lag broader clean‑tech plays and high‑growth leaders like NVIDIA and Tesla. At $2.44, it is far from any new high, underscoring that many institutional investors still want to see multiple quarters of consistent execution before re‑rating the stock.

How solid is Plug Power’s liquidity plan?

Balance sheet risk has been the biggest overhang for the stock. Plug Power ended 2025 with roughly $368.5 million in unrestricted cash, not a comfortable cushion for a capital‑intensive manufacturer that has historically burned cash. To extend its runway, the company signed a definitive agreement with Stream Data Centers to sell its Project Gateway site and associated electrical infrastructure for at least $132.5 million. This is part of a broader program aiming to unlock more than $275 million via asset sales, release of restricted cash and reduced maintenance costs.

Management now expects this liquidity, together with lower capex and improving margins, to fund operations through 2026 and reduce the risk of near‑term equity issuance. That is a crucial piece of the Plug Power Turnaround for U.S. investors who have been diluted repeatedly over the last cycle.

However, the legal backdrop is a reminder that the risk profile is still elevated. A class action securities lawsuit filed by Levi & Korsinsky alleges misleading statements about Department of Energy funding and hydrogen plant build‑outs. While such cases can take years to resolve, they add uncertainty around potential settlement costs and management distraction, two factors that conservative investors in the S&P 500 and large‑cap energy names generally seek to avoid.

What does the new Plug Power strategy change?

Strategically, the company is trying to pivot from “growth at all costs” to disciplined commercialization. New CEO Jose Luis Crespo has laid out a multi‑year roadmap: positive EBITDA by 2026, positive operating income in 2027 and full profitability by 2028. Importantly, Plug Power says roughly 80% of its expected 2026 revenue is already visible, supported by its installed base and contracted project pipeline.

The latest catalyst for sentiment came from Canada. Plug Power won a front‑end engineering design and 275‑megawatt GenEco PEM electrolyzer award for Hy2gen’s Courant green hydrogen and ammonia project in Quebec, one of the largest electrolyzer deals in its history. Market reaction on Wall Street was immediate, with PLUG shares popping double digits when the contract was announced, as traders reassessed order momentum in the electrolyzer segment.

Major banks like RBC Capital Markets are now engaging more actively with management; Plug Power is participating in an RBC non‑deal roadshow in Canada to explain its path to profitability to institutional investors. The tone from research desks remains mixed, with a consensus “Hold” stance and widely dispersed price targets, reflecting both the upside of a successful Plug Power Turnaround and the downside of execution or funding missteps.

How does Plug Power stack up in the hydrogen race?

For U.S. investors constructing diversified portfolios alongside mega‑caps like Apple and NVIDIA, Plug Power sits firmly in the speculative bucket. Unlike oil and gas giants such as Exxon Mobil or Chevron, Plug offers no dividend and no stable free cash flow stream. Instead, it is a high‑volatility levered play on green hydrogen adoption, logistics decarbonization and industrial ammonia demand.

On the positive side, the Quebec electrolyzer award and other large projects in North America and Europe show that Plug remains a relevant technology provider as the hydrogen economy slowly scales. The shift to positive gross margin and more disciplined capex also moves the story a step closer to what mainstream Wall Street investors expect from industrial growth names.

On the negative side, the accumulated deficit is substantial, the class action lawsuit is a risk factor, and there is still no GAAP profitability timeline shorter than 2028. In a NASDAQ environment where profitable growth companies and AI infrastructure champions like Tesla often command the lion’s share of capital, Plug Power must now prove that its improving metrics are durable, not just cyclical.

Related Coverage

Investors following the hydrogen theme may want to revisit how the margin story started to shift earlier this month. An in‑depth look at the first gross margin inflection and market reaction is available in “Plug Power Turnaround +8.4%: First Margin Rally Shock”, which dissects whether the move from deeply negative to slightly positive margins can sustain a longer‑term re‑rating. For a broader energy backdrop, the recent volatility in traditional oil and gas also matters: “ExxonMobil Plunge -5.9%: War Risk Reset or LNG Upside?” explores how shifting war‑risk premiums and LNG dynamics could influence capital flows between fossil fuel majors and emerging clean‑energy plays like Plug Power.

Ultimately, the Plug Power Turnaround hinges on three pillars coming together: sustaining positive gross margins, executing the liquidity and asset‑sale plan without fresh dilution, and delivering on the Crespo team’s profitability roadmap. If those pieces align, PLUG could evolve from a trading vehicle into a credible long‑term hydrogen platform in U.S. portfolios. The next few quarters of orders, margin trends and cash flow will be decisive in showing whether this turnaround can finally stick for Wall Street investors.