Is the Realty Income Dividend Strategy still a true defensive income anchor in a higher-for-longer rate world?

Is Realty Income Corporation still a defensive anchor?

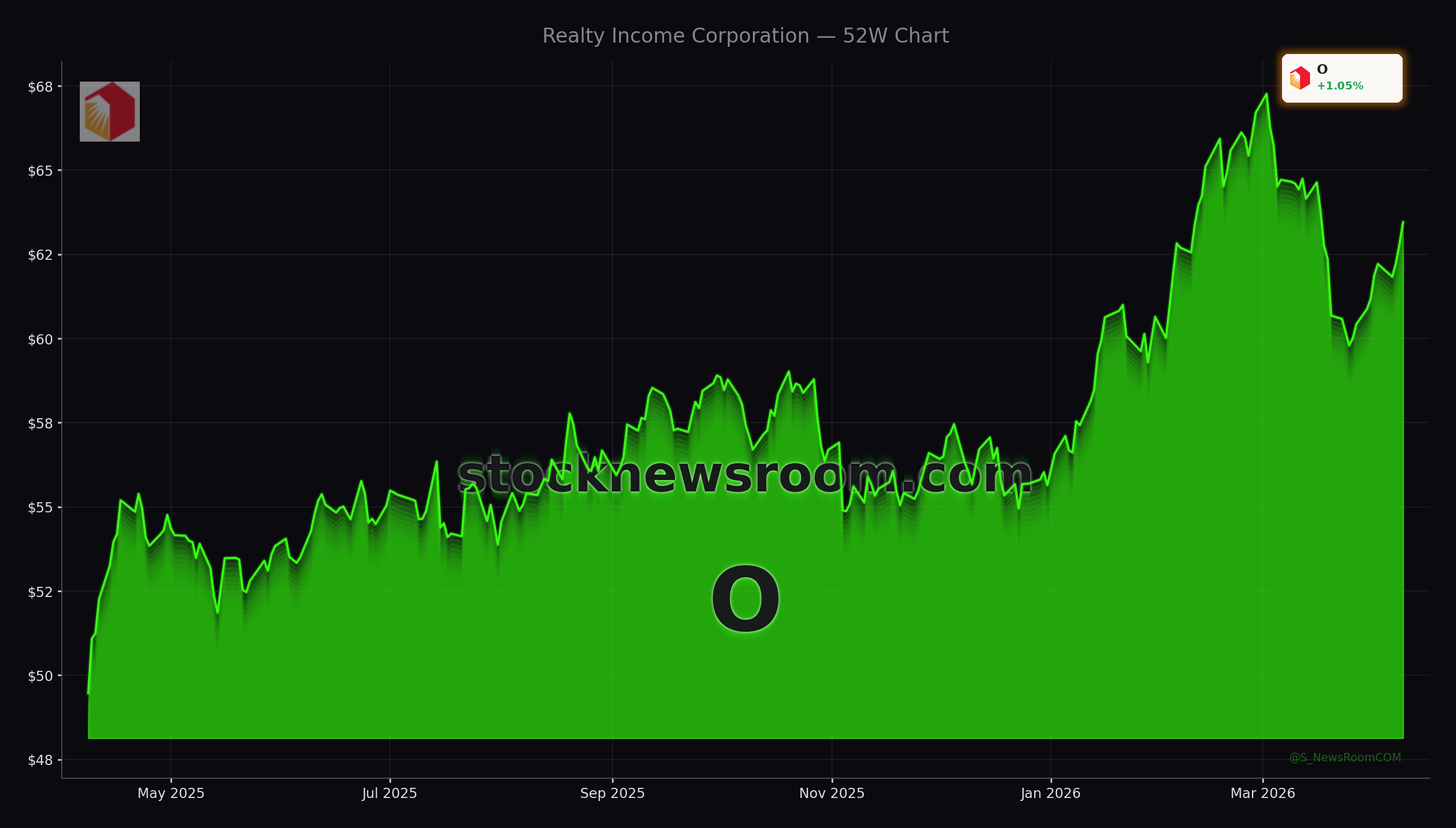

Realty Income Corporation brands itself as “The Monthly Dividend Company” for a reason: it has paid and increased its dividend annually for more than three decades, with over 114 consecutive quarterly hikes. At today’s price near $63.45, the forward yield of roughly 5% positions O as a high-yield alternative to Treasuries and investment-grade corporate bonds. Unlike fixed coupons, however, the Realty Income Dividend Strategy aims for slow but steady payout growth, historically around 3.8% to 4.2% annually over the long term.

The underlying business model is classic triple-net leasing. Tenants, not the REIT, carry most property-level costs such as taxes, insurance, and maintenance. That structure helps stabilize margins and cash flow, which is crucial when management targets a growing monthly dividend. Realty Income focuses heavily on sale-leaseback deals, acquiring properties from operating companies that then sign long-term leases with built-in rent escalators. The result is a largely contractual, inflation-linked revenue stream that has historically held up better than the broader S&P 500 during drawdowns.

Critically for the Realty Income Dividend Strategy, dividend coverage remains solid. In 2025, the REIT generated about $4.28 in adjusted funds from operations (AFFO) per share and paid $3.24 per share in dividends, implying a payout ratio near 76%. That leaves a buffer to absorb vacancies, refinancing costs, or modest acquisition missteps without putting the monthly dividend at acute risk.

How does Realty Income Dividend Strategy manage rate risk?

Higher-for-longer interest rates have been the main headwind for REITs. To support its acquisition-driven growth while managing that risk, Realty Income Corporation recently completed an $800 million offering of 4.750% senior unsecured notes due 2033. The new long-dated, fixed-rate debt extends the company’s maturity profile and locks in funding costs, which is central to keeping the Realty Income Dividend Strategy predictable for income investors.

The bond sale, underwritten by a syndicate of large investment banks, was received as a sign that credit markets remain comfortable with the REIT’s leverage and asset quality. TipRanks notes that Wall Street’s average rating on O is a “Hold” with a consensus price target around $66.39, while at least one analyst on that platform currently carries a Buy rating with a $70 target. That implies modest upside from current levels, on top of the 5%+ cash yield.

Nonetheless, income-focused shareholders should monitor leverage and interest coverage carefully. Each new debt issue layers in fixed obligations that must be met before equity holders get their monthly check. If acquisition yields compress or financing costs rise further, the spread that fuels AFFO growth could narrow, capping future dividend increases.

How does Realty Income compare to other income REITs?

Within the net-lease space, Realty Income sits alongside peers such as W. P. Carey and Getty Realty, which also pursue long-term, single-tenant leases. Realty Income’s portfolio is more retail-heavy, with about 80% of rent coming from single-tenant retail properties like grocery and convenience stores and discount chains, including tenants similar in profile to Dollar General and 7-Eleven. The balance comes from industrial assets and specialized properties such as casinos and data centers.

That focus on service-oriented, value-driven retail has historically proven resilient through economic cycles. It contrasts with peers that tilt more heavily toward industrial warehouses or gas stations. For broad income diversification, many investors pair Realty Income with pipelines like Enterprise Products Partners or consumer staples giants such as Procter & Gamble, and even large-cap tech dividend payers like Apple or NVIDIA. In that context, O functions as the real estate sleeve within a multi-asset, yield-oriented portfolio.

From a market-performance angle, Realty Income has behaved more defensively than the S&P 500, with historically smaller drawdowns during corrections. That low-volatility profile is a core selling point of the Realty Income Dividend Strategy for retirees and conservative investors who prioritize stable cash flow over aggressive capital gains.

What should investors watch next for Realty Income?

The latest insider developments have added a new layer for investors to watch. Executive Vice President Michelle Bushore recently sold a sizable block of shares and is expected to leave the company later this year, raising questions around management continuity and long-term capital allocation. At the same time, Realty Income has maintained its cadence of small, regular dividend hikes and continues to pursue external growth via acquisitions and funding partnerships, including a recent financing relationship with Apollo.

Institutional interest remains robust. Sound Income Strategies LLC, a yield-focused asset manager, recently increased its position in O by more than 8%, now holding over 350,000 shares worth roughly $21.7 million. That move underscores continued demand from professional income managers seeking a blend of monthly distributions and moderate growth. For the Realty Income Dividend Strategy to keep working, management must execute on three fronts: disciplined acquisitions, careful leverage management, and consistent, AFFO-backed dividend growth.

Related Coverage

Investors cautious about concentration risk in REITs may want to review the more skeptical take outlined in “Realty Income Dividend Strategy Warning for Income Investors”. That analysis explores how higher interest rates and ambitious growth plans could pressure payout safety and valuation. Together with the current article, it offers a more balanced view of the opportunities and risks surrounding Realty Income’s popular monthly dividend model.

In summary, the Realty Income Dividend Strategy still offers a compelling mix of a 5%+ yield, monthly payouts, and a long record of steady increases, supported by contractual triple-net cash flows. For long-term income investors on Wall Street and beyond, O can remain a core holding as long as management keeps balancing acquisition growth with prudent leverage and conservative payout ratios. The next few quarters of funding activity, portfolio deals, and dividend moves will show whether Realty Income can extend its run as one of the market’s most reliable cash-flow engines.