Is the Realty Income Dividend Strategy still a safe income anchor when higher rates and new growth bets collide?

Is Realty Income Dividend Strategy built for higher rates?

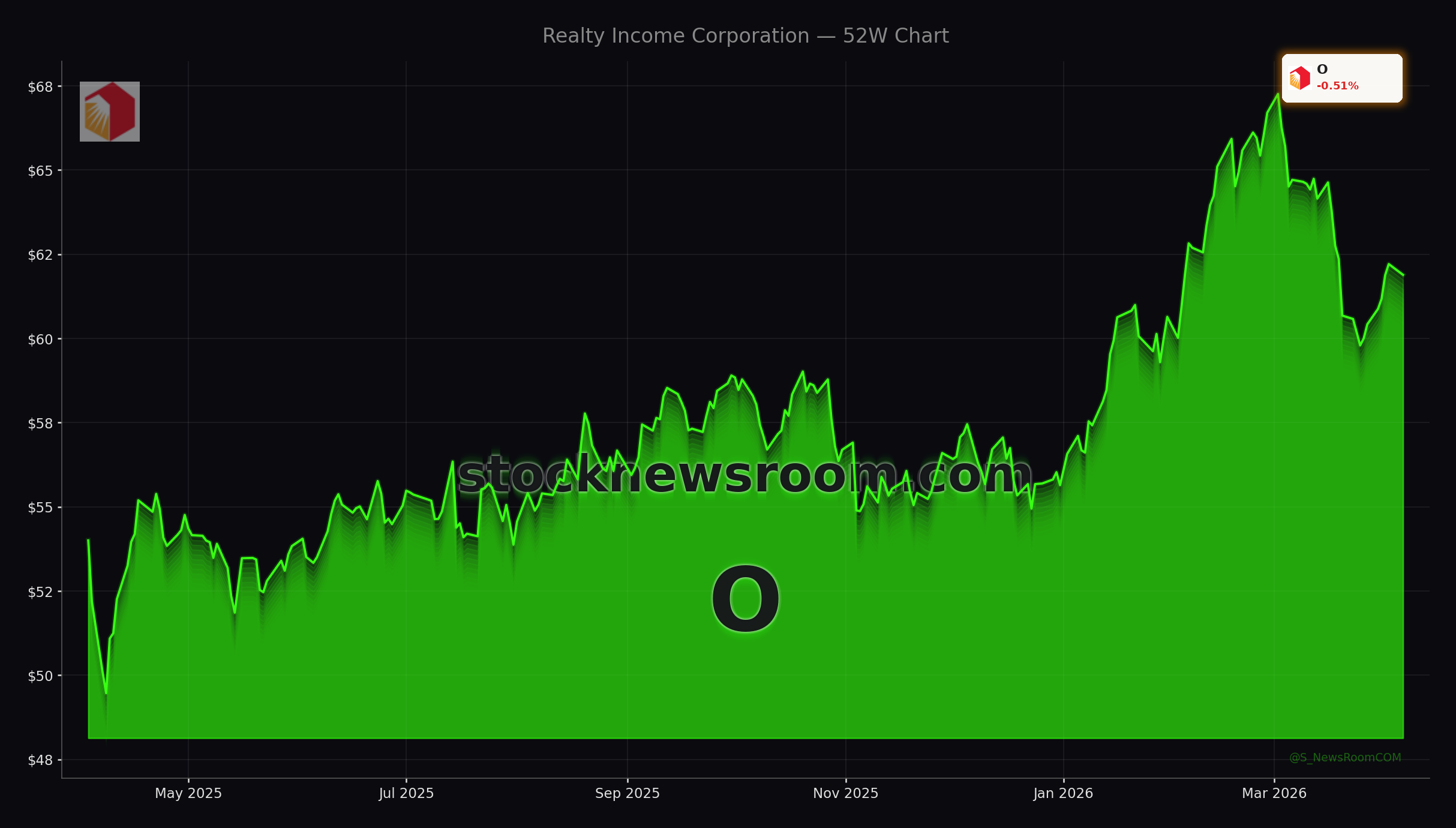

On Wall Street, real estate investment trusts have been pressured by tighter Federal Reserve policy, and Realty Income Corporation is no exception. At roughly $62 per share, the stock sits at a discount to some fair value estimates that place intrinsic value closer to the low $70s, leaving a potential upside window if rates stabilize or begin to fall. Yet the Realty Income Dividend Strategy does not rely solely on multiple expansion; it is anchored in a conservative payout policy, durable leases and steady acquisition-driven growth.

The REIT distributes about 75% of its adjusted funds from operations (FFO) as dividends. That leaves a meaningful buffer to reinvest retained cash into new properties while maintaining a monthly dividend that currently translates into an annualized payout near $3.25 per share and a yield above 5%. For investors comparing income options across the S&P 500, that yield sits well above the broader index and even ahead of many traditional dividend stalwarts like Apple or consumer staples giants.

Structurally, Realty Income’s portfolio is designed to weather economic cycles. It focuses on long-term net leases, where tenants – often investment-grade operators in grocery, convenience, pharmacy, industrial and gaming – cover taxes, insurance and maintenance. That arrangement stabilizes margins and supports the Realty Income Dividend Strategy by keeping property-level cash flows predictable even when cost inflation rises.

How does Realty Income stack up against other income plays?

For U.S. investors, Realty Income competes not just with other equity REITs but also with bond funds, utilities and high-yield blue chips like Tesla bond proxies or mega-cap tech dividend payers such as NVIDIA. While those growth names offer capital appreciation potential, they typically yield far less and lack the monthly cash cadence that appeals to retirees and income funds.

Within real estate, Realty Income is frequently grouped with net-lease peers and infrastructure income vehicles. Analysts have highlighted the REIT alongside global infrastructure partnerships that also deliver 5%+ yields and mid- to high-single-digit FFO growth. The differentiator for the Realty Income Dividend Strategy is its combination of scale – thousands of properties and a global footprint – and the branding power of being known as “The Monthly Dividend Company.” That branding is backed by substance: 669 consecutive monthly dividends and 31–32 straight years of annual dividend growth, including increases in each of the past 114 quarters.

Valuation remains a talking point on Wall Street. Equity research platforms recently pointed out that the shares trade at a high earnings multiple on GAAP metrics, reflecting depressed accounting earnings compared with cash-based FFO. Some models suggest the stock is modestly undervalued versus long-term fair value, but the elevated P/E has kept more aggressive growth investors on the sidelines. For income-first buyers, however, the focus remains squarely on the stability and growability of the quarterly and monthly checks.

What fuels future growth for Realty Income Corporation?

A critical pillar of the Realty Income Dividend Strategy is growth beyond traditional U.S. stand-alone retail. Management estimates a roughly $14 trillion addressable market in North America and Europe for net-leaseable real estate, providing a long runway for disciplined acquisitions. Recent moves include further expansion into Europe and Mexico and the addition of data centers as a new vertical, a segment that also benefits from secular AI and cloud demand that supports long-term rental growth.

Partnerships and alternative capital channels are another growth engine. Realty Income has entered joint ventures with large institutional partners, including a $1 billion vehicle with Apollo, and recently issued about $800 million of unsecured notes. These structures allow the company to scale acquisitions without over-levering its own balance sheet, while fee income and minority stakes can enhance returns. The REIT’s balance sheet remains among the strongest in the sector, supporting an investment-grade profile and relatively low funding costs compared to smaller competitors.

Income investors want to know if this growth converts into continued dividend expansion. Historically, Realty Income has raised its dividend at an annual compound rate of roughly 4.2% since its 1994 listing. Recent bumps have been smaller but steady, with the latest increase lifting the monthly payout to about $0.2705 per share. If FFO growth continues in the mid-single digits through international expansion and data center exposure, that pace of dividend growth appears sustainable, reinforcing confidence in the Realty Income Dividend Strategy.

Is the Realty Income Dividend Strategy still attractive now?

As of Monday’s session, the share price dip of around 0.55% leaves the yield comfortably above 5%, which screens favorably against U.S. Treasury yields that have recently hovered in the mid-4% range. The trade-off for investors is interest-rate sensitivity: if long-term yields push meaningfully higher, REIT valuations could compress further. Conversely, any dovish shift from the Fed or clearer visibility on rate cuts could unlock a re-rating for high-quality income names like Realty Income.

Wall Street commentary remains broadly constructive, with many income-oriented managers treating the stock as a “buy and hold forever” candidate rather than a trading vehicle. While detailed price targets from major banks such as Goldman Sachs or Morgan Stanley have not dominated recent headlines, independent valuation work suggests room for moderate upside alongside the reliable cash component. For diversified portfolios that already hold growth leaders like Apple or NVIDIA, adding a dedicated monthly payer can help balance volatility and support systematic withdrawal plans in retirement.

Ultimately, the Realty Income Dividend Strategy hinges on three levers: disciplined acquisitions across a vast global market, conservative financing underpinned by an investment-grade balance sheet, and a shareholder policy that prioritizes incremental, recurring dividend growth. For U.S. and international investors looking to build or reinforce an income sleeve, those pillars make the case that The Monthly Dividend Company can remain a cornerstone holding.