Can the Rigetti Quantum Strategy turn a 108‑qubit tech leap into profits before its sky‑high valuation runs out of time?

How does Rigetti Computing fit into Wall Street’s quantum bet?

Quantum computing remains one of the most speculative corners of the technology market, and Rigetti Computing, Inc. has become one of its purest plays. The company designs and fabricates its own superconducting quantum chips, builds full systems, and offers cloud access via its Rigetti Quantum Cloud Services and Amazon Braket, Amazon Web Services’ quantum platform. That vertical integration is central to the Rigetti Quantum Strategy: move faster than larger rivals by controlling the full stack, from hardware to programming language.

Despite that ambition, RGTI’s fundamentals look fragile. The company generated just $7.1 million in revenue in 2025, a 34% decline from the prior year, while running total operating expenses of $86.7 million and a GAAP net loss of $216.2 million. Yet the stock still commands a market capitalization around $4.7 billion, implying an eye‑watering trailing price‑to‑sales multiple of more than 600. For comparison, NVIDIA — a cornerstone of the AI boom in the S&P 500 — trades at a far lower sales multiple while delivering massive profits and cash flow.

What does the new 108‑qubit system really change?

The technological centerpiece of the Rigetti Quantum Strategy is the new Cepheus‑1‑108Q system, billed as the industry’s largest multichip quantum computer. It triples the qubit count of Rigetti’s prior 36‑qubit Cepheus machine and adopts a modular, chiplet‑based architecture designed to scale.

The system reportedly reaches 108 qubits and achieves 99.9% gate fidelity, meaning roughly one error per 1,000 quantum operations. That is a meaningful benchmark in a field where qubits are notoriously unstable and error‑prone, and it positions Rigetti to tackle larger, more complex workloads in areas such as optimization, materials science, and cryptography. Cepheus‑1‑108Q is already accessible via Rigetti’s own cloud platform and Amazon Braket, offering developers hands‑on access to the company’s latest quantum processing unit (QPU).

However, 99.9% fidelity is still not enough to solve many real‑world commercial problems, especially those requiring long, deep quantum circuits. The next challenge for the Rigetti Quantum Strategy is not only scaling qubits, but also pushing error rates down further and demonstrating clear, repeatable advantages over classical systems operated by cloud leaders like Apple’s rivals in big tech and AI‑accelerated data centers powered by NVIDIA and others.

Are analysts buying into Rigetti’s valuation?

Despite the weak current fundamentals, several Wall Street firms remain optimistic. Cantor Fitzgerald recently reiterated its Buy rating on RGTI and raised its price target to $30, more than double today’s price. Mizuho also maintains an Outperform rating, even after trimming its target from $43 to $33 as it reassessed the broader quantum sector and the escalating race for logical — error‑corrected — qubits.

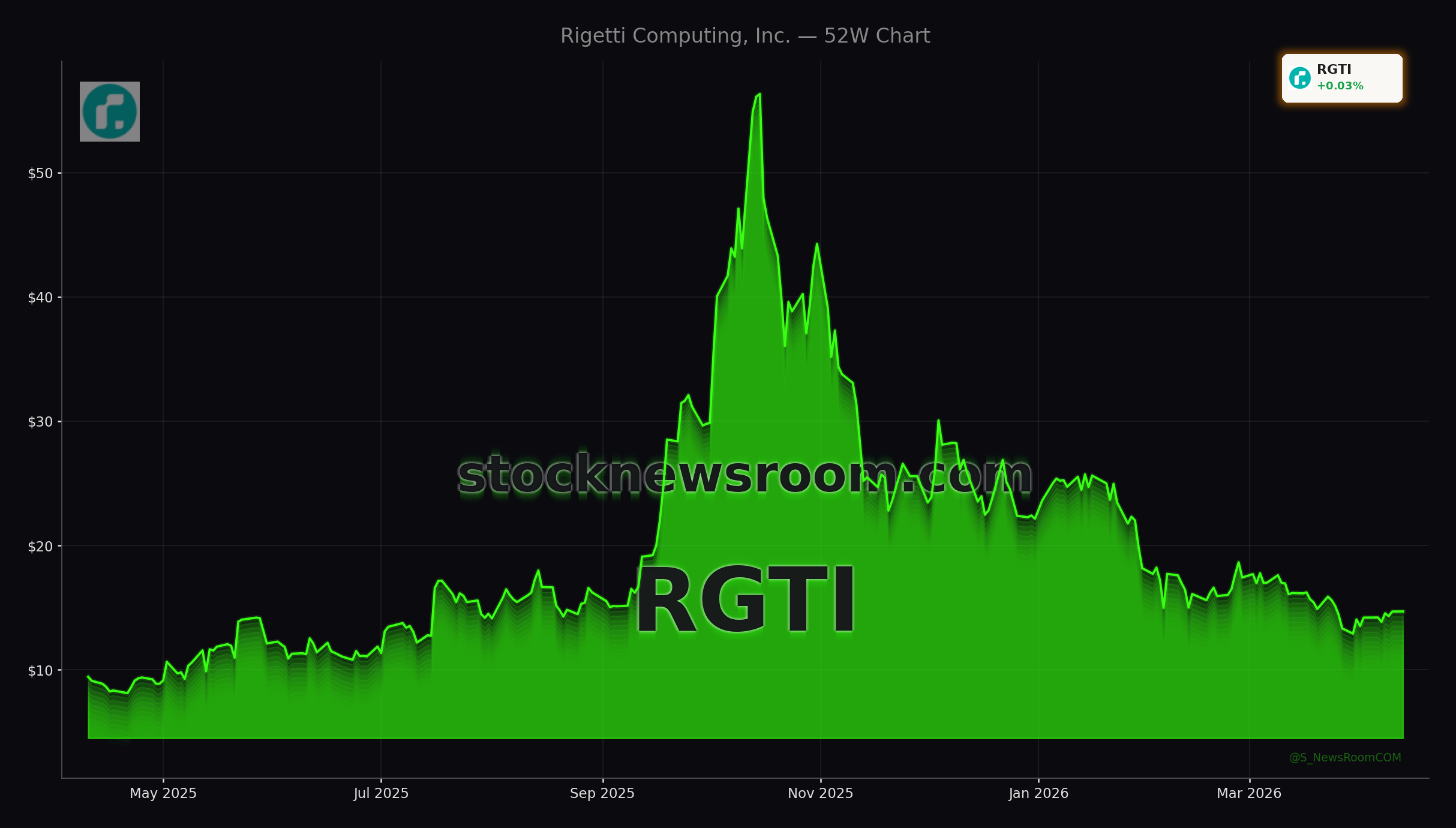

Other research shops paint a mixed picture. Some technical services give RGTI a low trend rating, noting that the stock has underperformed many semiconductor peers and remains volatile, even after a recent bounce. One analysis highlights a consolidation zone with support near $13.31 and resistance around $14.69, suggesting traders are still debating the next move. Meanwhile, broker consensus sits around a “Moderate Buy” with an average target near the low‑$30s, implying substantial upside but also embedding significant execution risk.

On the ownership side, institutional investors hold roughly a third of the float, with large managers like Vanguard among the top shareholders. Insider selling in recent months has raised eyebrows, as executives and directors have taken some chips off the table while the company is still deeply unprofitable.

Is Rigetti Quantum Strategy sustainable financially?

Financial sustainability is the core risk in the Rigetti Quantum Strategy. With only $7.1 million in 2025 revenue and more than $86 million in operating expenses, Rigetti is a classic pre‑scale, high‑burn R&D story. The bright spot is liquidity: the company ended 2025 with $589.8 million in cash and equivalents, giving it a multi‑year runway to invest in product development, build partnerships, and seek higher‑value contracts, including potential on‑premises deployments.

Wall Street currently expects revenue to more than triple to about $22.5 million in 2026. Even on that forecast, RGTI would still trade at a forward price‑to‑sales ratio above 200 — an extreme valuation compared with most Nasdaq technology names and far richer than large‑cap innovators like Tesla or NVIDIA. Mathematically, the stock would have to fall over 90% from current levels to trade at a valuation multiple closer to mature, profitable chipmakers in the S&P 500.

For U.S. investors, RGTI therefore sits firmly in the speculative bucket alongside other early‑stage quantum players. Success would likely require Rigetti to prove that Cepheus‑1‑108Q and its successors can unlock commercial use cases that justify premium pricing and durable demand. Failure to do so could leave shareholders exposed to a sharp repricing if sentiment turns and the market prioritizes cash flow over long‑dated promises.

Related Coverage

Investors who want a deeper dive into Rigetti’s recent performance can read Rigetti Computing Earnings -3.0%: Quantum Hype Faces Valuation Warning, which dissects how quarterly numbers highlight the gap between technological milestones and monetization. For a broader view of how market cycles and capital intensity impact chip and compute plays, Micron AI Memory Boom: -1.8% Dip as $100B Bet Surges looks at whether the AI memory upcycle marks a new structural phase for semiconductor demand.

In the end, the Rigetti Quantum Strategy combines world‑class engineering ambition with one of the most stretched valuations on Wall Street. For aggressive, long‑term investors comfortable with binary outcomes, RGTI offers pure exposure to potential quantum disruption, but conservative portfolios may prefer to watch from the sidelines until revenue traction and margins catch up with the story.