Can a profit surprise and new adtech alliances turn the latest Roku Forecast into a long-term streaming comeback story?

How is Roku reshaping expectations on Wall Street?

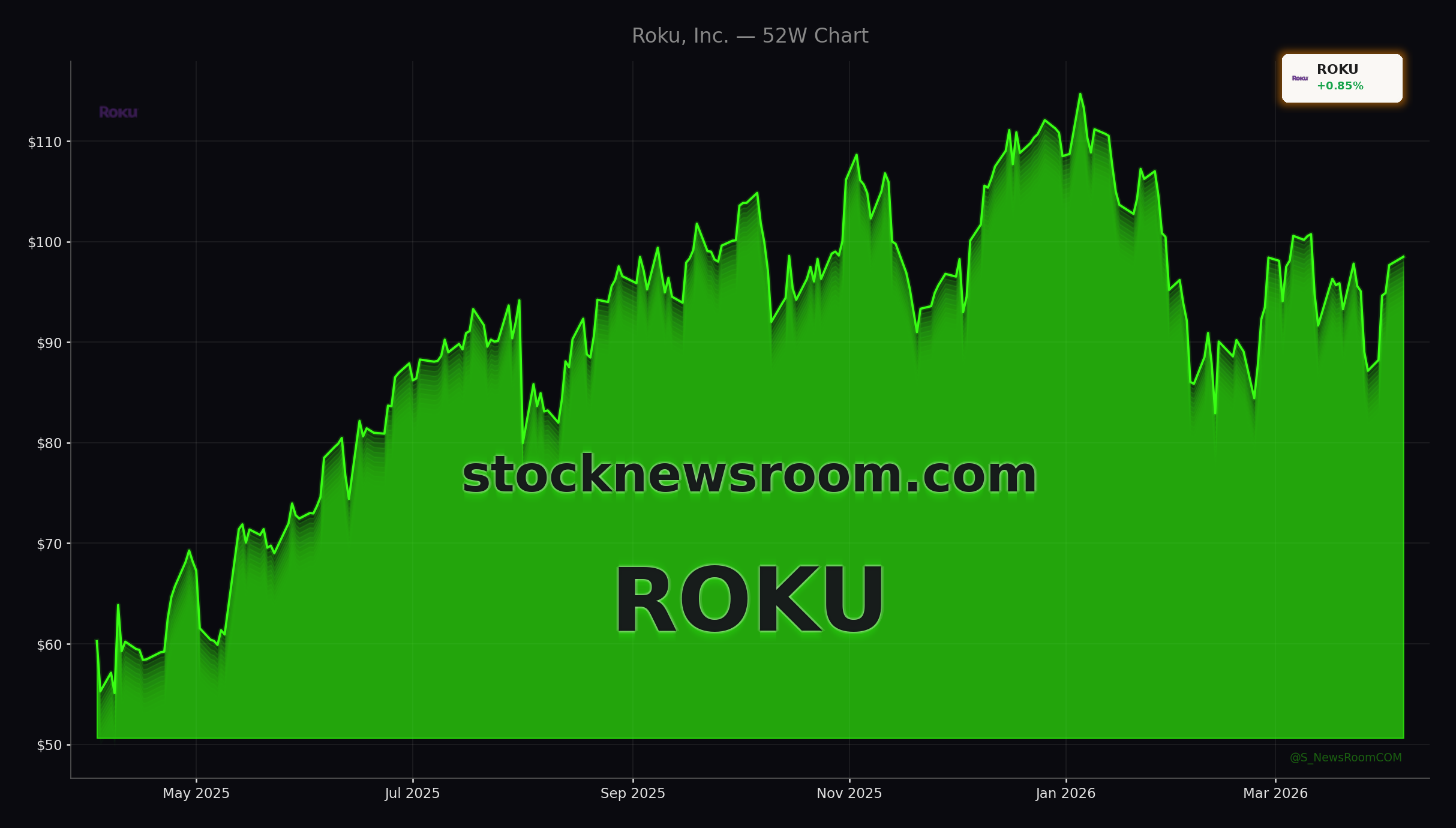

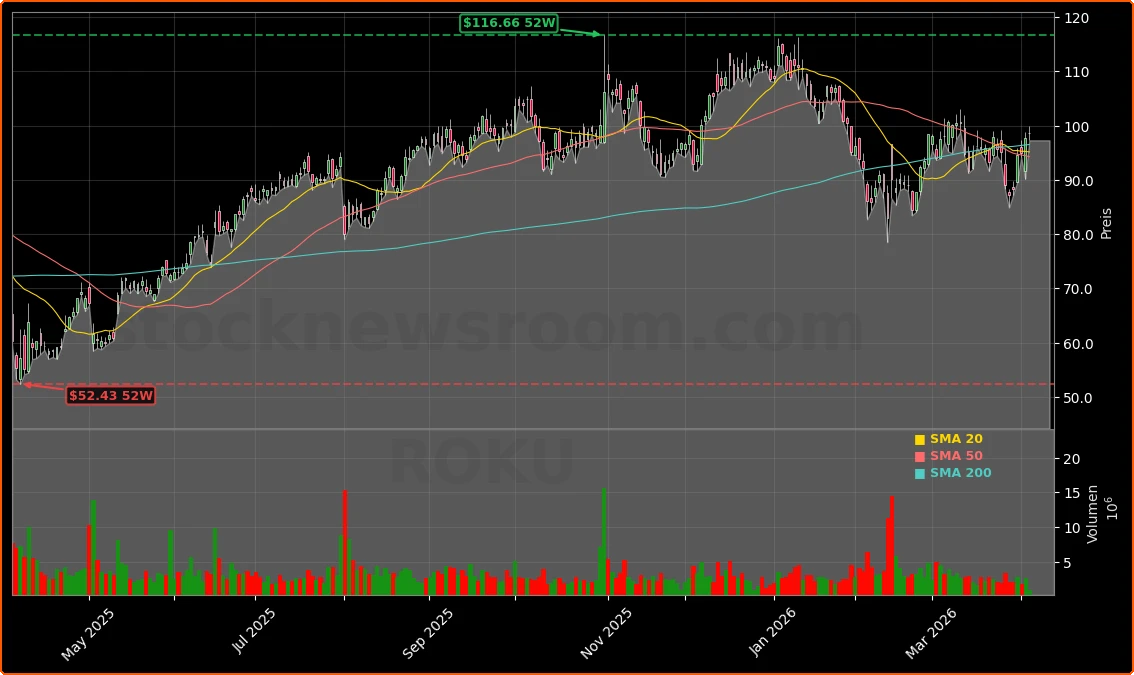

Roku stock has climbed roughly 38% over the past 12 months, handily beating the broader S&P 500 and NASDAQ benchmarks, even though shares remain well below their 2021 peak. The move has been driven less by hype and more by fundamentals: double-digit revenue growth, a surprise return to profitability, and stronger free cash flow.

The latest catalyst for the improving Roku Forecast is another price target hike. Baird analyst Vikram Kesavabhotla lifted his target from $110 to $120, implying more than 20% upside from current levels. That follows earlier optimism from Citizens, which boosted its target to $160, citing Roku’s dominant connected TV operating system footprint in roughly half of U.S. living rooms.

These calls stand out at a time when many growth and ad-driven names on NASDAQ are seeing reductions in targets as investors brace for slower consumer spending and tougher advertising comparables. Roku, by contrast, has delivered 11 consecutive quarters of double-digit top-line growth since going public and has begun converting that scale into earnings leverage.

In its most recent quarter, the company generated about $80 million in net income — double the level it had initially guided — and more than doubled free cash flow for the year. Management now projects that net income could triple by 2026, a key pillar for any medium-term Roku Forecast focused on cash generation rather than just user growth.

Roku Forecast: Can adtech deals drive the next leg up?

For streaming investors, a crucial part of the Roku Forecast centers on advertising technology and partnerships. Roku has historically been viewed as a rival by larger platforms, but that narrative is shifting as the company becomes an indispensable gateway to connected TV (CTV) audiences.

Last summer, Roku struck an ad partnership with Amazon, giving the e-commerce and cloud giant broader access to Roku’s CTV ad inventory. More recently, Roku was named a launch partner for Alphabet’s Display & Video 360 demand-side platform, enabling advertisers to match first-party data with premium publisher inventory across Roku’s ecosystem. Rather than trying to outbuild every tool in-house, Roku is positioning itself as the high-engagement screen where major adtech stacks want presence.

The company’s own free, ad-supported service, The Roku Channel, has quietly become a star asset. It has risen into the top ranks of apps on Roku devices and is now described as the second most-watched ad-supported streaming service in the U.S., behind only YouTube. That scale gives Roku added pricing power with brands and agencies, which feeds directly into platform-margin expansion.

Other initiatives are also aimed at diversifying revenue. Roku is rolling out low-cost streaming service Howdy off-platform — including distribution via Amazon’s Prime Video and a standalone app — targeting incremental subscription and high-margin revenue while maintaining its focus on monetizing the home screen and CTV ad tools.

How does Roku stack up against mega-cap rivals?

A persistent bear case in any Roku Forecast is the competitive threat from tech titans. Roku is going up against Alphabet, Amazon, and even hardware-oriented rivals like Apple and NVIDIA-powered smart TV ecosystems, not to mention consumer brands such as Tesla that increasingly view in-car screens as media platforms. The concern: can a mid-cap pure-play platform sustainably defend share against balance sheets measured in the hundreds of billions?

So far, usage trends suggest Roku is holding its ground. Time spent on Roku’s platform rose about 15% year over year, with users now averaging roughly four hours per day. Active accounts exceed 90 million globally, giving advertisers reach that is difficult to replicate outside of YouTube and a handful of premium streamers. While hardware remains a lower-margin business and faces intense price competition, Roku’s strategic focus is clearly on the scalable, higher-margin platform and ad segment.

Investor sentiment is not uniformly bullish. Some commentators argue that Roku is spreading itself across devices, adtech, and content, which could dilute focus compared with more narrowly targeted software plays. There have also been modest insider sales in recent days by a director and the chief accounting officer under pre-arranged 10b5-1 plans, a data point that short-term traders may watch closely, even if such sales are common among tech executives.

Yet broader qualitative screens of U.S. high-growth tech stocks still place Roku in the “watch closely” bucket due to its combination of rapid revenue growth, meaningful insider ownership and an expanding international footprint. Discounted cash flow-based assessments from several research shops argue that the stock could be trading below intrinsic value if management delivers on its profitability roadmap.

What should investors watch in the next Roku Forecast?

Looking ahead, the next key checkpoints for the Roku Forecast will be whether the company can sustain double-digit platform revenue growth, continue delivering earnings beats, and deepen its integration into the broader CTV ad ecosystem.

Wall Street will pay close attention to engagement metrics on The Roku Channel, any further expansion of Howdy off-platform, and additional ad partnerships with major agencies or cloud providers. Macro-sensitive ad budgets remain a swing factor: if U.S. ad spending slows sharply, even a strong operator like Roku could see pressure on CPMs and campaign volumes.

From a valuation perspective, the stock has rebounded from its lows but remains far below its 2021 highs, which leaves room for multiple expansion if Roku proves it can be a durable cash-generative platform rather than just another cyclical ad play. Against the backdrop of a still-cautious NASDAQ, the evolving Roku Forecast will hinge on balancing growth with disciplined cost control and capital allocation.