Are improving Salzgitter Earnings and a shrinking loss enough to justify a turnaround bet in a shaky European steel cycle?

How did Salzgitter Earnings evolve in 2025?

Salzgitter AG (SZG.DE), one of Germany’s major steel producers, reported a significantly narrower net loss for fiscal 2025, highlighting tangible progress in its turnaround efforts. The company’s net loss shrank to around EUR 70–75 million, compared with more than EUR 350 million a year earlier, driven by lower depreciation and amortization and better performance in key business units. Earnings before interest and taxes (EBIT) swung to a positive result of roughly EUR 60 million after a substantial loss in the prior year, underscoring the early impact of restructuring and cost-cutting initiatives.

The improvement came even as revenue declined to EUR 8.98 billion from about EUR 10.0 billion, reflecting lower average steel prices and the deconsolidation of the stainless tubes group in the Steel Processing division. At the EBITDA level, the company generated just over EUR 375 million, down from more than EUR 440 million previously, indicating that margin pressures from weaker pricing and demand have not fully abated. Still, Salzgitter Earnings showed that the profit improvement program delivered more than EUR 120 million in additional cost savings, providing a buffer against the softer top line.

From a Wall Street perspective, these Salzgitter Earnings illustrate a classic late-cycle industrial story: improving efficiency and profitability off a depressed base, but still heavily exposed to macro volatility, especially in Europe. For U.S. investors accustomed to the scale and diversification of large-cap names like NVIDIA or Apple, Salzgitter represents a more cyclical, regionally focused bet tied directly to steel demand, energy prices and European industrial activity.

What is the outlook for Salzgitter Earnings in 2026?

Management has issued guidance for 2026 that points to a measured recovery rather than a rapid rebound. The company expects sales to rise to around EUR 9.5 billion as steel volumes stabilize and pricing gradually improves. For profitability, Salzgitter is targeting EBITDA VX of EUR 500 million to EUR 600 million and pre-tax earnings (EBT VX) between EUR 75 million and EUR 175 million. If achieved, those targets would mark a clear step-up from 2025 and signal that the turnaround is gaining traction.

However, executives remain cautious. Chief Executive Officer Gunnar Groebler has emphasized the drag from persistently high energy prices, weak industrial demand and growing uncertainty around global trade policies. The company continues to focus on rigorous cost cutting, restructuring and portfolio optimization, including the transformation of its trading activities and potential strategic moves such as increasing its stake in Hüttenwerke Krupp Mannesmann, which could strengthen its integrated steel value chain over time.

Dividend policy underscores this cautious optimism. Despite the 2025 loss, the management board has proposed an unchanged dividend of EUR 0.20 per share, signaling confidence in the company’s liquidity and medium-term prospects. For yield-focused investors, the payout remains modest, but it does provide some income while waiting to see whether the 2026 Salzgitter Earnings targets are attainable.

Why is the Salzgitter share price under pressure?

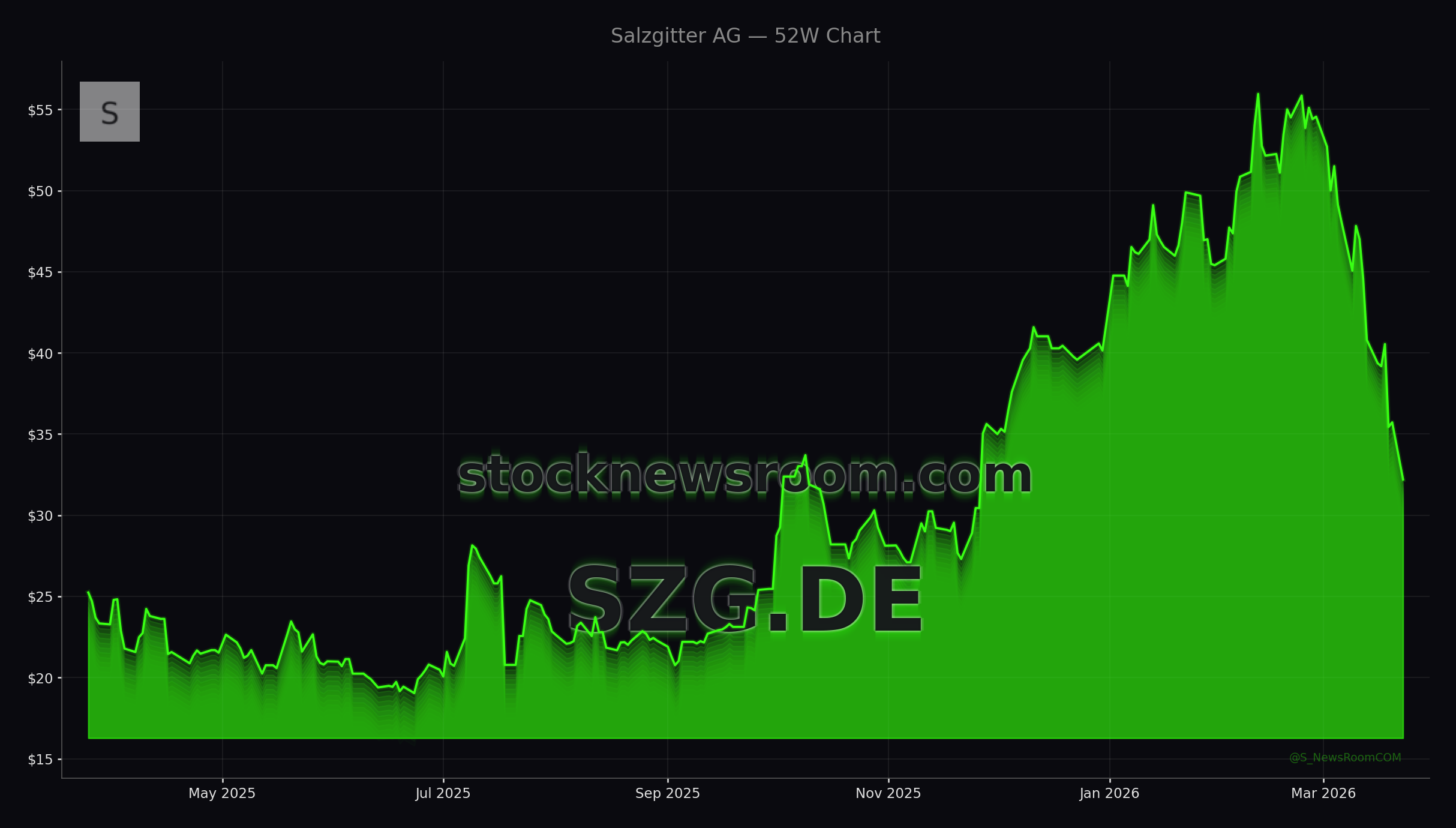

In the market, the reaction to the improved Salzgitter Earnings has been muted to negative. The stock recently traded around EUR 36.10, modestly higher than the previous close of EUR 35.68, but it has been volatile and, at times, sharply lower in recent sessions. Earlier trading saw intraday declines of around 7–9% as investors digested the guidance and weighed broader macro risks, especially the impact of conflict in the Middle East, elevated oil prices and concerns about European growth.

The broader basic resources sector in Europe has slid notably since the onset of the Iran-related conflict, with indexes such as the STOXX Europe 600 Basic Resources losing more than 15% in recent weeks. Salzgitter has underperformed even that weak backdrop, at one point shedding roughly 35% of its market value over the same stretch. Rising net debt and sizable capital requirements for its transformation program have added to investor concern, as has the company’s sensitivity to swings in energy and raw material costs.

Analysts remain cautious. JPMorgan, through analyst Dominic O’Kane, has reiterated an “Underweight” rating on the stock, pointing to higher-than-expected net leverage, significant investment needs and a still-conservative outlook for operating earnings relative to consensus. That stance contrasts with the more constructive views often seen for diversified U.S. and global peers such as Tesla in autos or NVIDIA in semiconductors, which are driven more by structural growth than by heavy cyclicality.

What do Salzgitter Earnings mean for U.S. investors?

For U.S.-based portfolios, Salzgitter offers targeted exposure to European steel and industrial demand, complementing positions in global miners and metals producers listed on the NYSE and NASDAQ. The latest Salzgitter Earnings indicate that management is executing on cost reductions and restructuring, yet the investment case remains tightly linked to the trajectory of European manufacturing, energy markets and geopolitical developments.

Compared with mega-cap U.S. names like Apple, Salzgitter is far smaller, less diversified and more volatile, but it can act as a levered play on a potential rebound in European construction, automotive and machinery demand. The steady, if low, dividend and improved 2025 results may appeal to contrarian value investors willing to accept higher risk in exchange for turnaround potential. Others may prefer to gain cyclical exposure through larger, more liquid global steel and mining companies or via sector ETFs that spread risk across multiple issuers.

Given the sustained economic weakness, energy prices at a high level, and growing uncertainty from trade policies, we are focusing on our own ability to take action.— Gunnar Groebler, CEO of Salzgitter AG

Ultimately, the key for investors will be whether 2026 guidance proves conservative and beatable, and whether management can balance capital-intensive transformation projects with disciplined balance sheet management. If macro headwinds ease and the company delivers on its targets, Salzgitter Earnings could mark the start of a more durable recovery. The coming quarters will show whether this German steelmaker can turn operational progress into sustained shareholder returns.