Is the SanDisk AI Infrastructure boom turning a once-cyclical memory name into one of Wall Street’s most coveted AI plays?

Is SanDisk AI Infrastructure driving the rally?

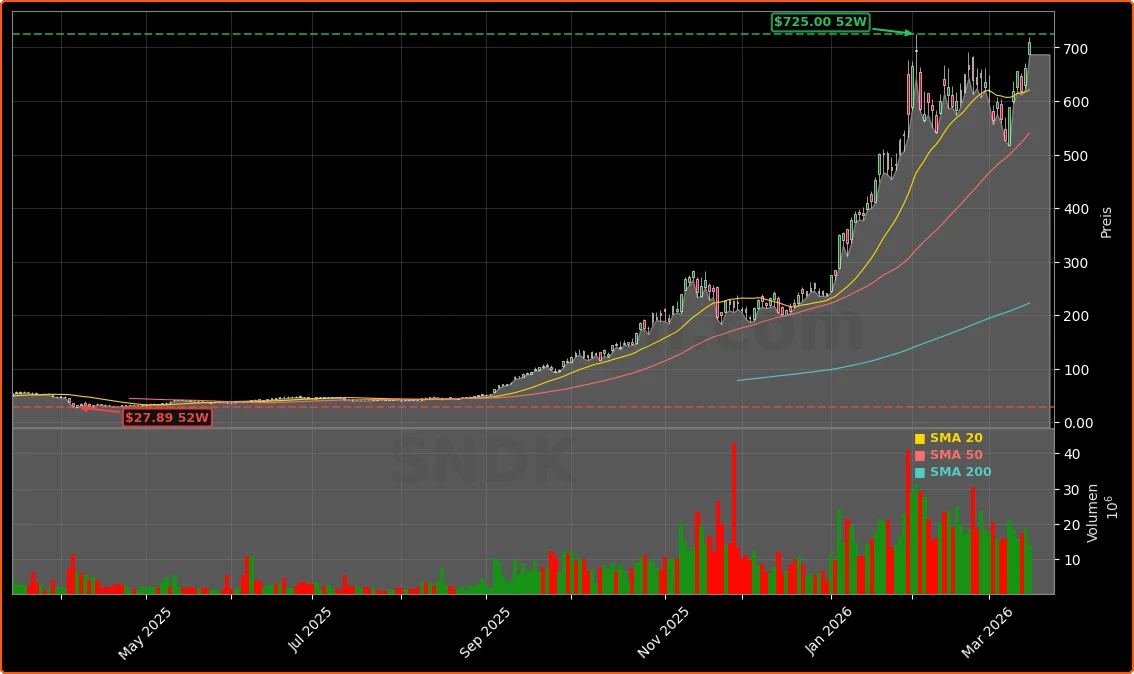

SanDisk shares climbed another 7.4% on Monday, closing at $710.60 versus a prior close of $659.59, as memory and broader AI‑infrastructure stocks led gains in the S&P 500 and Nasdaq. The move adds to a roughly 22% surge over the past week and a year‑to‑date gain above 200%, fueled by a rotation out of software into hardware and memory that directly supports SanDisk AI Infrastructure build‑outs.

SanDisk’s core thesis is straightforward: modern AI models from hyperscalers like NVIDIA’s key cloud partners need to store and retrieve massive datasets at extreme speeds. High‑performance NAND flash and enterprise SSDs are critical to that stack, and SanDisk is one of the few players with the scale to secure multi‑year, high‑volume supply deals. A recently announced $27 billion infrastructure commitment from cloud provider Nebius, anchored by Meta’s AI expansion, underscored to investors that the AI infrastructure supercycle remains intact.

As capital rotates into picks‑and‑shovels AI names, SanDisk now sits alongside Micron, Western Digital and Seagate as one of the strongest memory beneficiaries of the current build‑out phase.

How strong were SanDisk’s quarterly numbers?

For its fiscal Q2 2026, SanDisk reported revenue of $3.03 billion, up 61.2% year over year, driven primarily by data center SSD demand. Net income jumped roughly 672% to about $803 million as pricing and mix improved and utilization rates rose on already‑tight capacity. The data center segment alone grew 76% year over year, highlighting how central AI and cloud workloads have become to the company’s growth profile.

Management guided for a remarkably strong fiscal Q3, forecasting revenue of $4.4 billion to $4.8 billion and non‑GAAP EPS of $12 to $14. Gross margin is expected in a rich 65% to 67% range, levels more commonly associated with leading GPU and accelerator suppliers than with traditional memory manufacturers.

CEO David Goeckeler outlined a strategic pivot to multi‑year, take‑or‑pay style contracts with hyperscalers, effectively locking in utilization as SanDisk AI Infrastructure deployments ramp. The company’s manufacturing capacity is described as fully booked on long‑term agreements, giving unusual visibility in a normally cyclical memory market.

How does SanDisk compare to Micron and peers?

For U.S. investors used to thinking of Micron and Apple’s ecosystem suppliers as the primary memory plays, SanDisk’s run has been eye‑catching. Both Micron and SanDisk have benefited from tight DRAM and NAND supply, but SanDisk is more squarely leveraged to high‑performance NAND needed in AI‑optimized data centers and high‑throughput storage nodes.

Research shops highlight that SanDisk and Micron are up more than 1,200% over the past year in some windows, underscoring the magnitude of the memory trade. Yet SanDisk’s exposure to enterprise SSDs, hyperscaler storage tiers and emerging agentic‑AI workloads has led some analysts to argue it offers purer SanDisk AI Infrastructure leverage than more diversified chip names.

Nvidia’s upcoming GTC 2026 conference is another potential catalyst: Nvidia has teased a next‑generation AI memory hierarchy and rack‑scale designs that could increase NAND intensity per rack. If those architectures lean more heavily on QLC SSDs and high‑bandwidth flash tiers, SanDisk’s planned BiCS8‑based product ramp could see additional upside.

What is Wall Street’s view on SanDisk now?

Analyst sentiment remains broadly positive. The average Wall Street price target for SNDK sits around $718.78, implying modest further upside from Monday’s close. Several major houses, including firms tracked by MarketBeat and Zacks, rate the stock a “Moderate Buy” and emphasize its leading position in AI‑driven storage. While specific banks like Goldman Sachs or Morgan Stanley have not been highlighted with fresh target changes in the latest commentary, the consensus remains that SanDisk is a core beneficiary of long‑duration AI capex.

Bulls argue that with factories sold out on multi‑year deals and a clear roadmap in enterprise SSDs, SanDisk is positioned as a structural winner of the SanDisk AI Infrastructure wave. Skeptics counter that the stock already discounts a substantial portion of that growth. After a more than 200% YTD move, even minor disappointments in Q3 execution, pricing, or hyperscaler capex timing could trigger sharp pullbacks.

AI workloads don’t just need more compute; they need a step‑function increase in high‑performance storage, and SanDisk is one of the few players scaled to deliver it.

— David Goeckeler, SanDisk CEO

Conclusion

For diversified U.S. portfolios, that sets up a classic risk‑reward tradeoff: high conviction in secular AI infrastructure demand against elevated expectations and rich valuation multiples relative to historical memory cycles.

Further Reading

- SanDisk Corporation (SNDK) stock quote and news (Yahoo Finance)

- AI Workloads Raise Storage Demand: Is Sandisk Positioned to Benefit? (Zacks Investment Research)

- Sandisk: This Nvidia GTC 2026 Announcement Could Be A Game Changer (Seeking Alpha)

- Lumentum, SanDisk, and IREN Are All Rallying Today — Here’s the $27 Billion Reason Why (24/7 Wall Street)