Is the latest SanDisk Forecast signaling the start of a new AI memory super‑cycle or the peak of an extraordinary rally?

Is SanDisk’s AI rally entering a new phase?

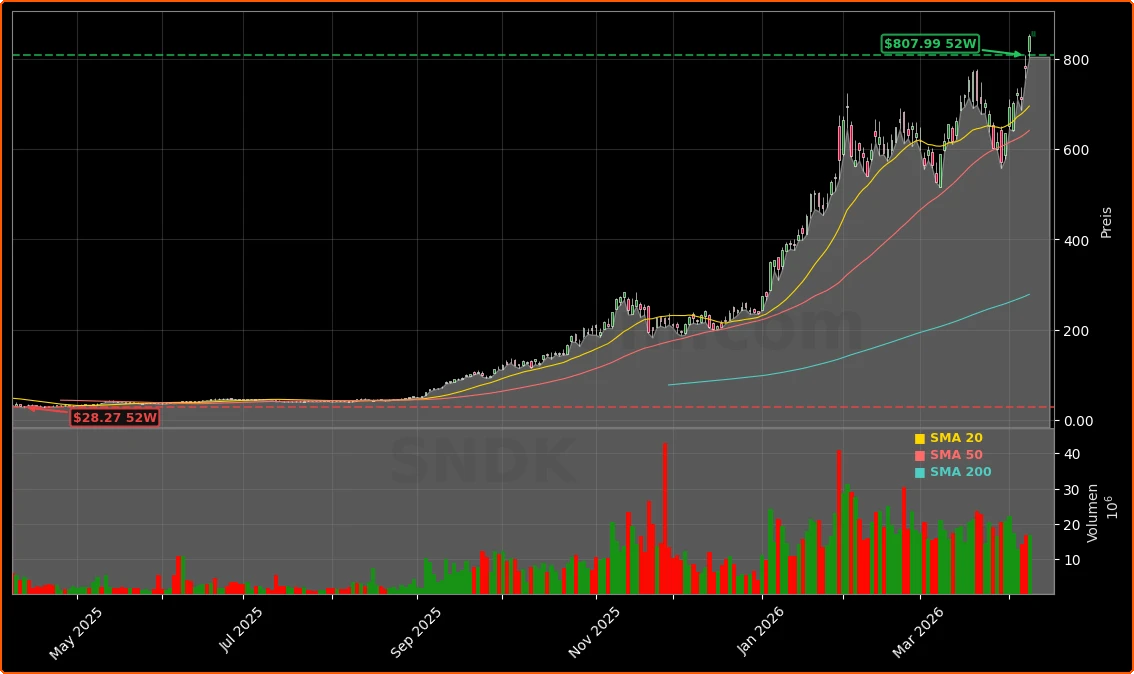

SanDisk (Western Digital) closed Thursday at $851.57, up 9.05% on the day, and traded at $861.36 (+1.15%) after hours, extending an extraordinary run that has seen the stock soar roughly 2,300% year over year. The move comes as the broader AI trade on the NASDAQ remains centered on compute leaders like NVIDIA, but memory has quietly become a second pillar of the theme. For SanDisk, the core driver is its position as a primary supplier of enterprise SSDs and NAND flash storage to hyperscale AI data centers, where model training and inference workloads demand enormous, high‑performance storage capacity.

Over the past year, SanDisk’s data‑center segment revenue climbed to about $440 million in its latest reported quarter, up 76% year over year, underscoring how tightly its growth is tied to the AI infrastructure cycle. A recent 10% price hike on NAND flash products, pushed through in the face of tight supply, highlights that the company is not only riding volume growth but also flexing pricing power in a market many analysts expect to remain structurally undersupplied into the late 2020s.

What does the new SanDisk Forecast from Bernstein imply?

Bernstein SocGen’s Mark C. Newman has become one of the loudest bullish voices on SanDisk. He lifted his base‑case price target by 25%, from $1,000 to a Street‑high $1,250, explicitly arguing that the market still underestimates both the earnings power and the durability of this memory up‑cycle. In his SanDisk Forecast, Newman values the stock on an average earnings framework across 2026–2029, projecting about $114 in annual EPS in the base case and applying an 11x multiple to reach the $1,250 target.

In an upside, or “blue‑sky,” scenario, Bernstein sees the possibility of SanDisk averaging closer to $224 per share in earnings if NAND prices remain elevated and AI‑driven volume growth persists. Under those conditions, the stock could justify a higher multiple and, in Newman’s view, potentially trade as high as $3,000. That would imply more than a three‑fold gain from current levels—an aggressive SanDisk Forecast that underscores how polarized expectations have become around the name.

How are other Wall Street firms positioning?

Bernstein’s call adds to a chorus of bullish views from major U.S. banks. Morgan Stanley recently raised its price target on SanDisk to $690 while reiterating a Buy rating, emphasizing that memory supply is now a critical bottleneck in AI buildouts and that customers are increasingly willing to pay upfront to secure capacity. Bank of America and Goldman Sachs have also issued Buy or Outperform ratings with targets around $900, even though the stock is already trading above the current consensus target, flagging elevated valuation risk.

Quant models are similarly constructive. SanDisk now tops Seeking Alpha’s large‑cap tech quant rankings, reflecting strong revisions, momentum, and profitability trends compared to peers on the S&P 500 and NASDAQ. At the same time, some research shops urge caution, pointing out that SanDisk has posted losses in each of the last three years and remains highly exposed to cyclical swings in NAND pricing, which historically have been brutal when supply finally catches up.

How does SanDisk compare with other AI winners?

For U.S. investors already heavily allocated to AI compute leaders like NVIDIA or platform plays such as Apple and Tesla, SanDisk offers a different but complementary exposure: memory and storage rather than GPUs or consumer hardware. Unlike diversified mega‑caps, SanDisk’s earnings trajectory is tightly leveraged to NAND and, increasingly, DRAM pricing. The company is pushing beyond pure NAND through a roughly $1 billion investment for a 3.9% stake in Nanya Technology, paired with a multi‑year DRAM supply agreement that positions it to better serve AI inference workloads.

SanDisk has also extended its Flash Ventures joint venture with Kioxia through 2034, locking in manufacturing capacity, and partnered with SK Hynix on High Bandwidth Flash solutions designed for next‑generation AI inference. These moves are intended to secure long‑term volume and technology roadmaps, distinguishing SanDisk from more commodity‑oriented memory suppliers and reinforcing the bullish SanDisk Forecast among institutions betting on a multi‑year AI infrastructure buildout.

What risks could derail the SanDisk Forecast?

The parabolic share‑price move itself is a key risk. After a 2,000%+ 52‑week gain and a year‑to‑date jump north of 200%, volatility is extreme; the stock has already seen nearly 10% single‑day swings. Any disappointment on earnings, NAND pricing, or AI capex budgets could trigger sharp corrections, especially with the share price now well above the current average analyst target. SanDisk’s next major catalyst is its fiscal Q3 2026 earnings report, scheduled for April 30 at 1:30 p.m. ET, where management has guided to $4.4–$4.8 billion in revenue, non‑GAAP EPS of $12–$14, and gross margins of 65%–67%.

Geopolitical and supply‑chain risks also loom large. SanDisk relies heavily on manufacturing partnerships in Asia, particularly its Kioxia joint venture, exposing it to trade policy shifts, tariffs, and regional tensions. On the technology side, recent talk of “peak memory” following efficiency breakthroughs like Google’s TurboQuant algorithm briefly rattled the sector, though many analysts argue Jevons Paradox will prevail—cheaper, more efficient memory usage ultimately expands total demand. Still, a rapid downturn in NAND prices would quickly compress margins and challenge the most optimistic SanDisk Forecast scenarios.

Related Coverage

Investors looking for a deeper dive into fundamentals and recent catalysts can review the latest earnings breakdown in SanDisk Earnings Surge +10.5% in Powerful AI Rally, which explores how the billion‑dollar Nanya deal and AI demand are reshaping the company’s growth profile. For a view across the broader tech landscape, our sector coverage in Zscaler Forecast -11.3% Crash: BTIG Warning vs Growth examines how sharply sentiment can turn even on high‑growth names, a reminder that SanDisk’s own trajectory could become more volatile if macro or sector‑specific headwinds emerge.

The current SanDisk Forecast reflects both the upside of AI‑driven memory demand and the fragility of a stock priced for continued perfection. For U.S. portfolios already benefitting from the AI trade, SanDisk offers high‑beta leverage to storage and memory—but with commensurate downside if the cycle turns. The upcoming April 30 earnings report will be the next key test of whether this momentum story can keep delivering the numbers needed to justify, or even extend, today’s aggressive expectations.