Is the latest JPMorgan downgrade just another dip in SAP’s cloud transition or a serious warning for long-term investors?

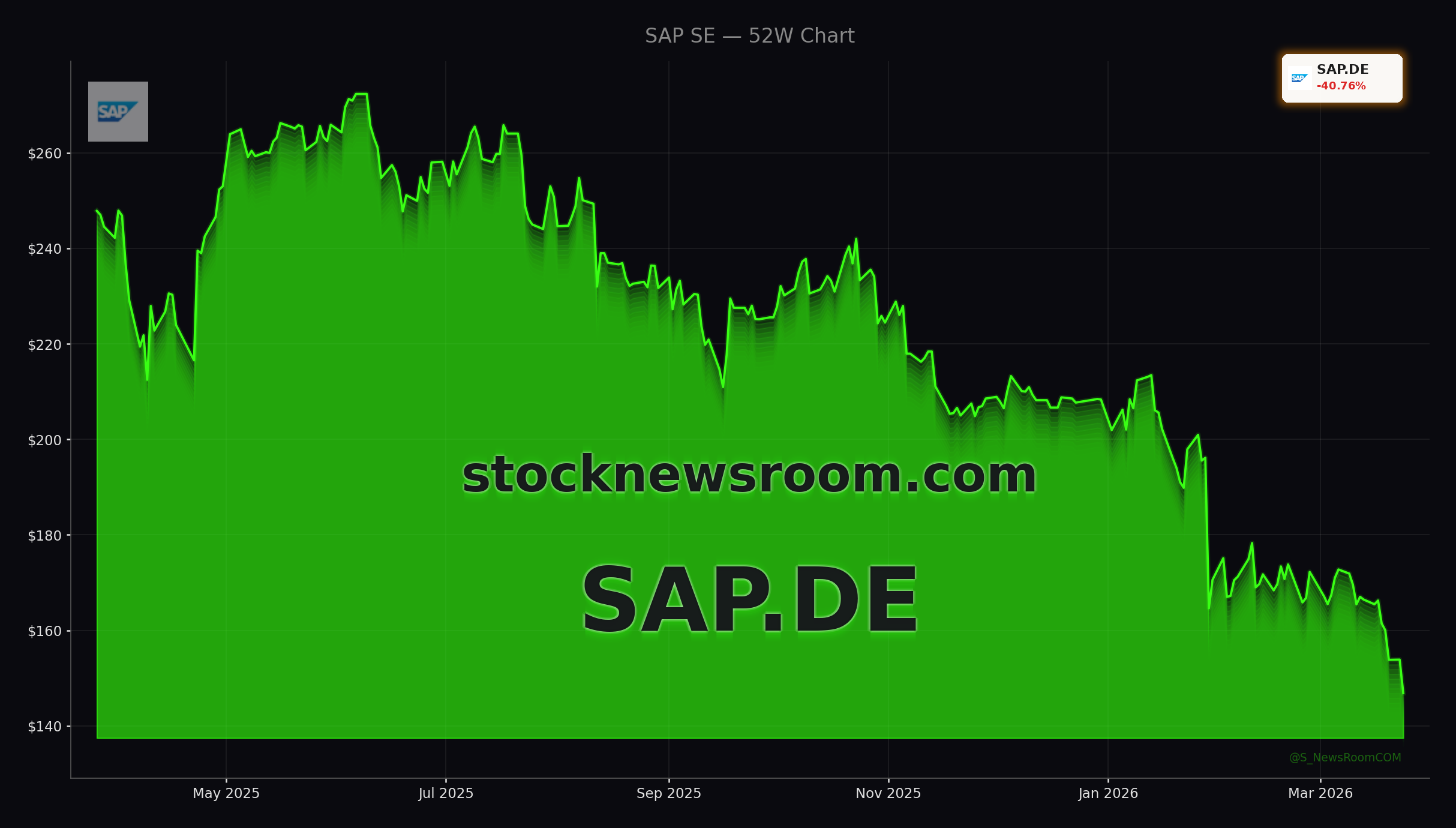

How severe is the SAP selloff?

SAP remains one of Europe’s largest technology names, but its latest slide is putting pressure on portfolios from Frankfurt to Wall Street. The stock recently traded at around $146.96, down roughly 4.5% on the day and almost 40% below its prior all‑time high, making it one of the weaker large‑cap software names so far in 2026. The decline stands in contrast to U.S. peers like NVIDIA and Apple, which remain much closer to their 52‑week highs and continue to benefit from strong AI‑driven narratives.

The latest leg lower was triggered by a high‑profile downgrade from JPMorgan, but it comes on top of weeks of underperformance following SAP’s softer 2026 cloud guidance and ongoing legal and AI‑execution concerns. Technical indicators have deteriorated as well: the stock has broken through key support levels near EUR 150 and is trading in oversold territory on several momentum measures, reinforcing a bearish short‑term tone similar to what some quantitative macro strategies have flagged for SAP on U.S. exchanges.

What did JPMorgan change in its SAP Forecast?

The core shock for the SAP Forecast came from JPMorgan analyst Toby Ogg, who cut his rating from Overweight to Neutral and reduced his price target from EUR 260 to EUR 175. Ogg no longer expects the previously anticipated acceleration in growth and margin expansion. Instead, he argues that SAP’s current cloud backlog is likely to decelerate as the migration base matures, while the shift toward a more usage‑based billing model could introduce greater earnings volatility.

Ogg also points to intensifying competition in AI and cloud, highlighting faster‑growing rivals in the generative AI space that are expanding annual recurring revenue aggressively. For U.S. investors used to robust top‑line trajectories from leaders like NVIDIA or hyperscale cloud platforms, the idea that SAP’s cloud and AI transition might deliver slower or choppier growth is a clear negative for the SAP Forecast in the near term.

How are other analysts resetting expectations?

JPMorgan’s move did not occur in isolation. Kepler Cheuvreux cut its SAP price target from EUR 240 to EUR 190 while maintaining a Buy rating, and Jefferies trimmed its target from EUR 290 to EUR 230, also sticking with a bullish stance. Despite these cuts, the average analyst target still sits around the mid‑EUR 200s, implying more than 50% upside from current levels if the SAP Forecast eventually stabilizes and the company executes on its strategy.

Quantitative and AI‑driven research platforms have started to diverge in their views. Some models now flag SAP as technically weak with elevated downside risk, while others focus on fundamentals such as solid cash flow and low leverage, assigning Buy ratings with one‑year targets well above EUR 250. This split underscores a key dilemma for international investors: trade the negative momentum and cloud concerns, or lean into long‑term valuation upside that assumes SAP’s AI and cloud pivot ultimately delivers.

Is SAP still investing for growth?

Despite the gloomier SAP Forecast, management continues to push strategic initiatives aimed at securing growth beyond the current reset. SAP has launched a Defense Innovation Hub in Munich to capitalize on rising global defense spending, aiming to integrate software, data and AI into interoperable systems for armed forces. The defense segment already contributes roughly 10% of revenue and is currently SAP’s fastest‑growing business line.

On the commercial side, SAP is pressing ahead with marquee cloud migrations, such as FC Bayern Munich’s move to RISE with SAP and SAP Cloud ERP, which is designed to provide real‑time analytics, improved data protection and AI‑powered tools for fan engagement and operations. These projects highlight how management wants to reposition the company as a cloud‑first, AI‑enabled platform, even as near‑term margins come under pressure from higher investment and slower‑than‑hoped cloud backlog growth.

What does this mean for U.S. portfolios?

For U.S. investors, SAP trades on both European exchanges and the NYSE, often serving as a diversification play alongside domestic software names like Tesla’s AI‑driven software efforts in automotive and energy or platform companies in the S&P 500. With the stock now at multi‑year lows and sentiment fragile, SAP has become a high‑beta expression of European tech risk, particularly around enterprise cloud and AI adoption.

The downgrade forces investors to decide whether SAP’s cloud and AI transition is a temporary earnings setback or a sign that the company will lag faster‑moving software rivals.— Senior equity strategist at a European investment bank

Valuation has compressed meaningfully: on some 2026 earnings estimates, SAP now trades at a low‑20s forward P/E, a discount to many U.S. software peers, though still at a premium to traditional value sectors. Short‑term traders are focused on whether support in the EUR 135–150 zone holds, while longer‑term investors are watching the next earnings report and updated guidance for signs that the SAP Forecast on cloud backlog, AI monetization and margin recovery is bottoming. Until clearer evidence of a turnaround emerges, the stock is likely to remain sensitive to further analyst revisions and macro risk‑off moves that hit global tech.