Can the latest Seagate Forecast justify a 327% rally and today’s 7.5% surge on the back of AI storage demand?

How is Seagate reshaping AI storage momentum?

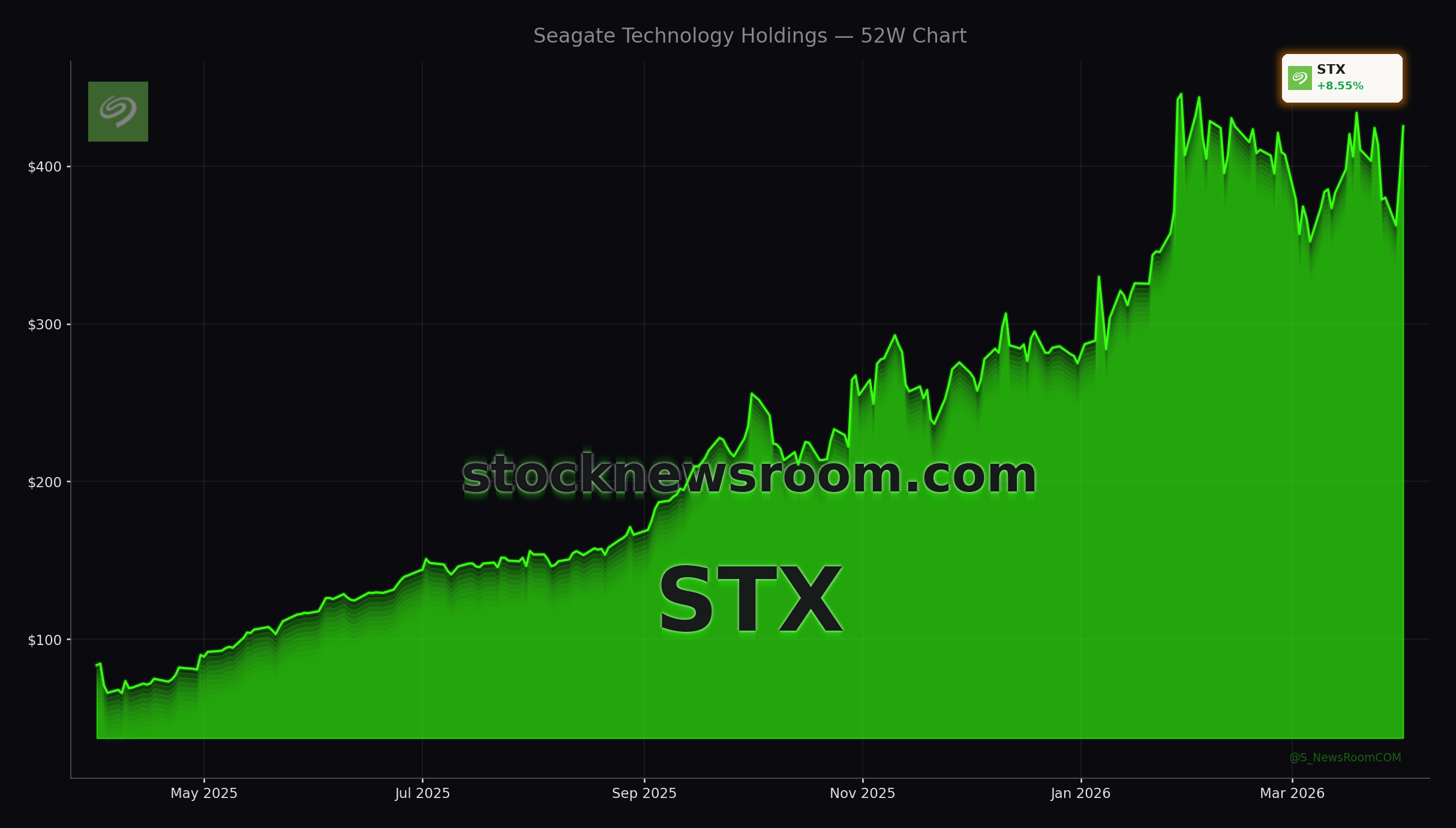

The Seagate Forecast comes against a backdrop of renewed strength in AI and chip infrastructure stocks, with hard‑disk rival Western Digital, Intel, Marvell Technology, Micron Technology, ARM, ASML, Applied Materials, KLA, Lam Research and Advanced Micro Devices all trading higher. Within this group, Seagate Technology Holdings plc stands out: the stock has rallied roughly 327% over the past year, driving its market capitalization to just under $83 billion.

Despite that surge, today’s move suggests the market believes the AI storage cycle still has room to run. Seagate’s nearline hard‑disk drives, including 32‑terabyte models, have become a key plank of capacity expansion for hyperscale data centers powering generative AI, cloud workloads and big‑data analytics. The company also sells SSDs, expansion desktop drives and high‑capacity external drives used in enterprise backup, gaming, personal storage and video surveillance.

For U.S. investors focused on the NASDAQ and S&P 500 technology complex, the Seagate Forecast underscores a theme: AI returns are broadening beyond GPU leaders like NVIDIA and into the storage stack that keeps those accelerators fed with data. That dynamic is supporting demand from private and public cloud operators and multicloud environments, including major customers such as AWS and IBM.

What does the Seagate Forecast say about earnings?

Seagate’s latest reported quarter, fiscal Q2 2026, set the foundation for the upgraded Seagate Forecast. Revenue came in at $2.83 billion, beating Wall Street expectations by about $80 million and rising 21.5% year over year. Non‑GAAP earnings per share of $3.11 topped consensus by $0.27, reflecting improving gross margins and disciplined capacity additions in the hard‑disk market.

Management paired the beat with positive guidance for fiscal Q3 2026, calling for further margin expansion and solid EPS growth as AI‑driven demand combines with higher‑capacity drives using HAMR (heat‑assisted magnetic recording) technology. Free cash flow has also strengthened, with one recent quarter generating a record $607 million in FCF. Seagate continues to return capital via a quarterly dividend of $0.74 per share, a notable income component for long‑term holders in a sector often driven by growth alone.

The company’s strategy emphasizes limiting unit growth while migrating customers to higher‑capacity drives measured in exabytes shipped. That approach aims to keep pricing firm and protect profitability even as hyperscalers ramp capex. For investors wary of memory’s historic boom‑bust cycles, this more disciplined supply backdrop is a key pillar of the bullish Seagate Forecast.

How are Wall Street analysts positioning on Seagate?

Analyst sentiment has turned decisively positive. JPMorgan’s Samik Chatterjee, one of Wall Street’s highest‑ranked analysts, recently initiated coverage with an Overweight rating and a $525 price target, implying about 25% upside from today’s $421 level. Chatterjee argues that structurally stronger nearline HDD demand, an oligopolistic industry structure and pricing tailwinds could drive meaningful upside to consensus estimates through 2027.

Bernstein is even more aggressive. The firm lifted its Seagate target from $500 to $620 while maintaining an Outperform rating, effectively signaling confidence that the stock can continue to climb despite its large prior gains. Other firms cited in recent filings and commentary place the average 12‑month target in the $450–$475 range, with an overall Strong Buy or Outperform consensus across 17 analysts (13 Buys, 4 Holds).

Not all valuation models agree, however. Research platform GuruFocus, using its proprietary GF Value metric, estimates a fair value closer to $170.54, which would imply substantial downside from current levels. The tension between bullish Street targets from JPMorgan and Bernstein and more cautious valuation frameworks shows that the Seagate Forecast is far from universally accepted, particularly after such a steep share‑price run.

How does Seagate compare with U.S. tech peers?

Compared with other U.S. technology names, Seagate is emerging as a pure‑play beneficiary of the storage layer of AI. While NVIDIA captures most of the GPU headlines and Apple and Tesla remain core holdings in many U.S. portfolios, Seagate offers a more targeted way to play the rising exabyte requirements of AI training and inference clusters. The company’s focus on high‑density HDDs and enterprise‑class SSDs positions it differently from DRAM and NAND manufacturers such as Micron and SanDisk, whose pricing can be more volatile.

We see significant upside to estimates from current levels with the HDD industry positioned to benefit both from strong demand stemming from hyperscaler capex plans as well as pricing tailwinds.— Samik Chatterjee, JPMorgan analyst

Institutional positioning reflects this shifting narrative. Affinity Wealth Management, for example, boosted its STX stake by 9.5% in Q4 to over 32,000 shares worth about $8.8 million, while other hedge funds have also adjusted exposures. At the same time, some investors have taken profits: Range Financial Group cut its STX holdings sharply, and corporate insiders have sold more than $44 million of stock in recent months. Those actions highlight that, even within a constructive Seagate Forecast, volatility and position trimming remain part of the story.