Is the semiconductor AI boom just the beginning for NVIDIA & Co. – or is the hype now tipping into dangerous overheating?

How Strongly Does NVIDIA Benefit from the Semiconductor AI Boom?

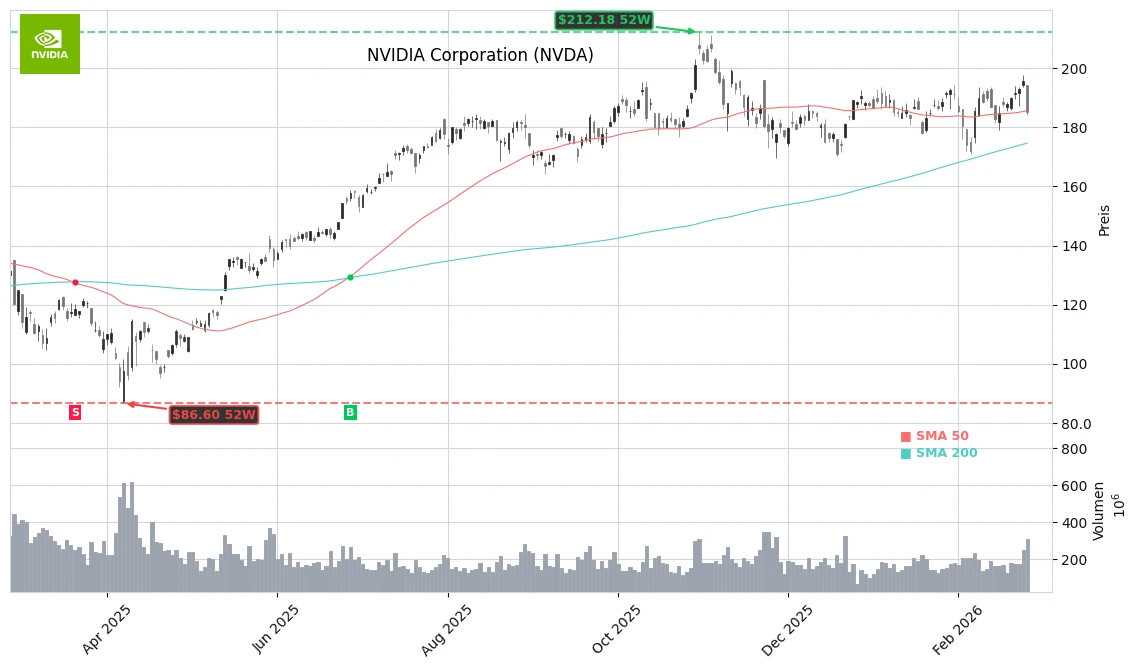

NVIDIA remains the symbol of the semiconductor AI boom. The company dominates the AI accelerator market with a share of up to 80–90%, driven by the massive expansion of data centers. Recent quarterly results showed a revenue increase of 73% and exceptional gross margins of around 75%, primarily fueled by the data center business. The net profit over the last twelve months is expected to total about $120B – a level that supports the valuation premium from an investor’s perspective.

Despite this growth, the market reacted cautiously after the fresh numbers. While NVIDIA exceeded expectations for earnings per share and provided a strong outlook, the stock only moved within the previously priced volatility range. This indicates an “overcrowded trade,” where high expectations are already factored into the price. Additionally, there are operational risks: demand for AI chips exceeds supply by a ratio of about 12 to 1, while there are ongoing shortages in High Bandwidth Memory (HBM) and packaging capacities.

Analysts like Morgan Stanley still refer to it as one of the cleanest “beat-and-raise” cycles in the industry and see NVIDIA as the core beneficiary of the semiconductor AI boom. At the same time, they warn of the high dependence on a few hyperscalers and the export restrictions for high-performance chips to China, such as with H200 systems.

How is AMD Positioning Itself in NVIDIA’s Shadow?

AMD is trying to gain market share from NVIDIA in the semiconductor AI boom through partnerships and tailored solutions. Collaborations like the recent deal with Nutanix, where AMD invests $150 million in stock and provides an additional $100 million for joint projects, highlight the strategic focus on data center and AI workloads. Furthermore, hyperscalers are increasingly working on their own ASIC solutions, where AMD could be a technology partner.

In the competition, not only raw computing power matters anymore, but especially energy efficiency, as the global power demand of AI data centers is growing rapidly. Here, AMD and also proprietary solutions from large cloud companies are trying to challenge NVIDIA. However, investors must consider that NVIDIA, due to its established software and ecosystem dominance, remains significantly ahead in the short term.

Citigroup and RBC Capital Markets point out in their assessments the large market potential for both providers but caution that valuation levels in the sector are increasingly being questioned cyclically. Pullbacks like the current price drop in NVIDIA and AMD could still offer attractive opportunities for long-term investors in the semiconductor AI boom.

What Role Do Intel, MU, AVGO, and IFX Play?

In addition to the obvious AI winners, attention is increasingly turning to the second tier in the semiconductor AI boom. Intel is working to regain ground in the AI data center market, while MU, as a memory specialist, benefits from the sharply rising memory prices. The scarcity of HBM memory chips makes suppliers in this segment key bottleneck managers in the industry.

AVGO (Broadcom) and equipment suppliers like Applied Materials secure the physical infrastructure of the new AI data centers with network and manufacturing solutions. Infineon (IFX) also benefits from electrification and increasing software integration in the automotive sector, where ever more powerful semiconductors are needed for driver assistance, infotainment, and, prospectively, autonomous driving.

The ETF SMH reflects this breadth of the sector and has risen by around 80% over the past twelve months, highlighting the enormous dynamics but also the valuation risk of the entire semiconductor AI boom.

Are Overheating and Geopolitical Headwinds Looming?

The industry is simultaneously facing structural and cyclical risks. Inventories have risen by over 110% in some cases, as manufacturers prepare for a sustained demand surge. Should the monetization of AI infrastructure at end customers proceed more slowly than hoped or an economic downturn occur, cancellations of data center projects could ensue.

Geopolitically, the restricted access to the Chinese market remains a central risk. U.S. export regulations for high-performance chips like H200 hinder growth, even though licenses with high tariffs are granted in individual cases. At the same time, U.S. policymakers increasingly demand that tech companies secure their energy supply for new AI data centers themselves to relieve the public grid.

Despite these uncertainties, the mix of massive CapEx budgets from hyperscalers, the shift to one-year product cycles, and the bottlenecks in the memory sector suggest that the semiconductor AI boom will shape the sector for several more years.

NVIDIA is the Michael Jordan of the semiconductor sector – but competition in the AI age will become tougher, not easier.

— Morgan Stanley Semiconductor Team

Bottom Line

The semiconductor AI boom is creating a historic special economic situation, from which NVIDIA, AMD, and specialized memory and infrastructure providers disproportionately benefit. For investors, this means that pullbacks in leading stocks can present opportunities but require a vigilant eye on valuation levels, memory shortages, and geopolitical risks. Those looking to capitalize on the semiconductor AI boom should focus on leading quality stocks while also keeping an eye on the increasing sector differentiation and potential regulatory pushes.

Related Sources

- NVIDIA earnings power AI chip sector rally (Reuters)

- Global AI data center capex forecast to surge (Bloomberg)

- High-bandwidth memory emerges as key AI bottleneck (Financial Times)

- Chip Industry and AI Infrastructure at Yahoo Finance (Yahoo Finance)