Can the new ServiceNow AI Partnership with DXC turn a sharp stock pullback into a long-term upside story for investors?

How big is the DXC–ServiceNow AI Partnership?

DXC Technology and ServiceNow, Inc. have signed a new multi-year deal that aims to move large enterprises from AI experiments to full-scale execution. DXC will adopt ServiceNow’s Core Business Suite across its Global Business Services organization, embedding agentic AI into finance, HR, procurement and other back-office workflows. As “Customer Zero,” DXC will be the first global enterprise to run these new capabilities end to end, using digital agents to cut manual work, surface real-time insights and proactively resolve issues across complex, multivendor environments.

The idea is simple but powerful for investors: DXC’s internal rollout will generate a library of validated AI use cases and automation blueprints that can be packaged and sold to its worldwide client base, all running on the ServiceNow AI Platform. That effectively turns the ServiceNow AI Partnership into a go-to-market accelerator, with DXC’s 1,800-plus ServiceNow consultants positioned to scale these patterns to other large enterprises under tight governance and security constraints.

What does this mean for ServiceNow’s moat?

AI is both the biggest risk and the biggest opportunity for ServiceNow. On one hand, agentic AI and large language models make it easier for new players to automate tickets, approvals and routine workflows that ServiceNow has historically monetized through its SaaS platform. Ready‑to‑use AI from players built around models from firms like NVIDIA-powered cloud providers or startups using OpenAI and Anthropic threatens to chip away at legacy cloud software incumbents.

On the other hand, ServiceNow operates deep inside enterprise environments, under stringent security and data-governance layers that are not easy to replicate. Replacing the platform wholesale is a multi-year, high-risk effort; and swapping out individual workflows erodes the integrated experience that customers value. The ServiceNow AI Partnership strategy, centered on DXC and a growing ecosystem of specialized partners, is meant to keep customers on the platform while upgrading them with AI rather than letting them drift toward point solutions.

ServiceNow is also shifting toward more usage-based billing to cushion the impact if AI reduces seat counts or automates lower-level roles. For long-term investors, that business-model flexibility is as important as any single AI feature release.

Analysts: 76%–80% upside despite volatility?

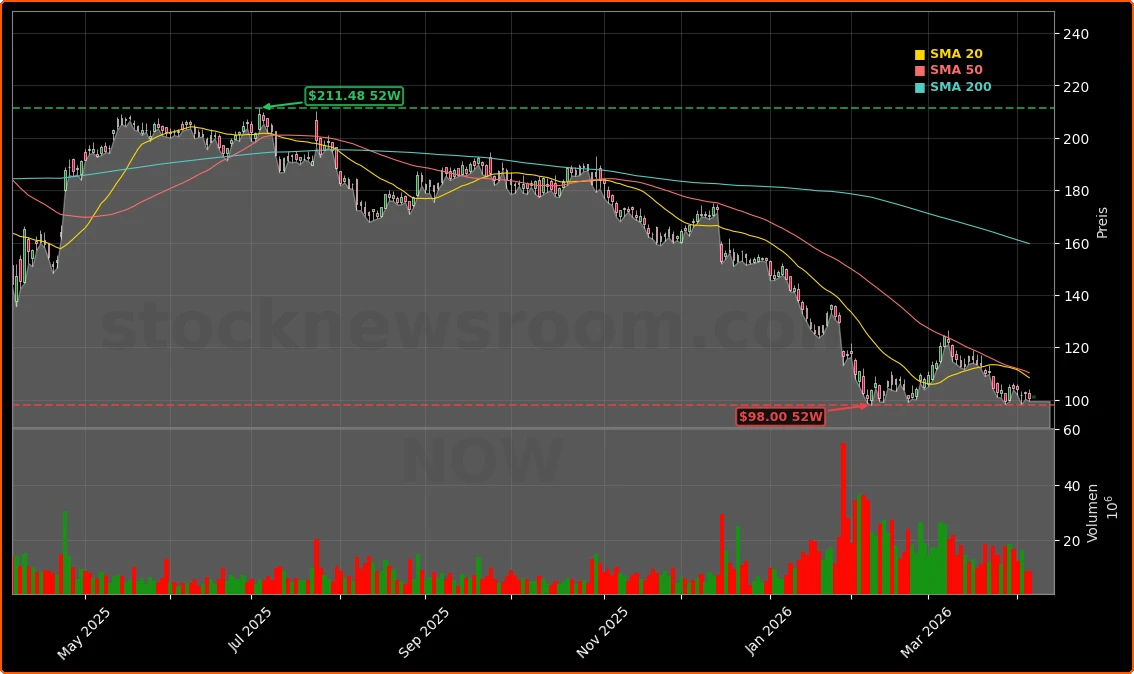

Despite the stock being about 56% below its peak, Wall Street remains broadly constructive. BTIG’s Allan Verkhovski reiterated a Buy rating on ServiceNow but trimmed his price target from $200 to $185, arguing that the 2026 subscription guidance currently offers limited upside and that consensus expectations for 2027–2028 might be too aggressive for this point in the cycle. MarketBeat data shows a broader analyst average around $185–$189, still implying roughly 80% upside to the current $100.55 share price.

Separately, a large group of analysts tracked by major financial data platforms remains overwhelmingly positive, with about nine out of ten ratings in the Buy camp and a median target near $180–$185. At today’s valuation, ServiceNow trades at under 25 times projected 2026 earnings, while profits are expected to grow around the mid‑20s percentage range annually over the next several years. That combination of growth and multiple compression underpins the bullish view that the ServiceNow AI Partnership approach can reignite the stock even if growth moderates from past highs.

Is the partner ecosystem another AI catalyst?

The DXC deal is not happening in isolation. ServiceNow’s partner community is expanding with AI-native players like Naitiv, a newly launched ServiceNow channel partner founded by veterans of Thirdera and insurance-industry specialists. Naitiv is targeting property and casualty insurance with agile, AI-enabled workflows on top of the ServiceNow platform, and has already acquired Inspira Systems and Cloudworks to accelerate that strategy. For ServiceNow shareholders, this illustrates how the platform can seed vertical AI solutions without the company shouldering all the domain-specific buildout itself.

Institutional investors appear to be using the sell-off to add exposure. Stock Yards Bank & Trust Co. lifted its ServiceNow stake by more than 2,500% in Q4 2025, while Portside Wealth Group boosted holdings over 400%, even as insiders have taken some profits. That split between insider selling and institutional buying is typical for high‑volatility tech names and suggests that professional money managers are betting that the ServiceNow AI Partnership roadmap will support durable earnings growth.

At the same time, enterprises face a broader debate about monitoring and productivity tools in the age of AI, including so‑called “bossware” that tracks remote employees. That discussion reinforces the value of platforms that can embed AI into workflows with strong governance and compliance—an area where ServiceNow positions itself against peers like Salesforce and against big‑tech platforms from Apple or Tesla that are pushing their own data and AI ecosystems.

Related Coverage

For a deeper dive into how this specific DXC agreement could turn short‑term share-price weakness into a longer‑term advantage, read ServiceNow AI Partnership: -1.8% Shock or New Upside Opportunity?, which unpacks the day’s move and market reaction in more detail. Investors tracking AI across the broader tech stack should also look at Advanced Micro Devices AI Strategy Boom Toward Tens of Billions, outlining how AMD’s data center push could complement software platforms like ServiceNow in AI‑heavy enterprise environments.

Putting ServiceNow’s Core Business Suite to work inside DXC allows us to prove what AI-powered operations look like in practice across complex, multivendor environments.— Russell Jukes, Chief Digital Information Officer, DXC Technology

In sum, the ServiceNow AI Partnership strategy—with DXC as Customer Zero and a growing circle of AI‑focused partners—positions the company to turn anxiety about agentic AI into a proof point for platform stickiness and usage-based growth. For U.S. and global investors, the combination of a beaten‑down share price, strong institutional interest and still‑bullish analyst targets makes the next few quarters of execution crucial. If ServiceNow can show that its AI partnerships translate into tangible revenue acceleration and durable margins, the stock has room to recover and potentially reward patient, long‑term shareholders.