Can the new Snap AR Partnership with Qualcomm rescue Snap’s risky hardware bet just as investors lose patience with the stock?

What does the Snap AR Partnership actually cover?

Snap Inc. has signed a multi‑year strategic agreement with Qualcomm Technologies to bring Snapdragon system‑on‑a‑chip solutions to future generations of Specs, the company’s upcoming AR eyewear. Specs, developed by Snap’s wholly owned subsidiary Specs Inc., are see‑through, standalone glasses designed to project digital objects into three‑dimensional physical space, powered by Snap OS and Snapdragon XR platforms. The goal of the Snap AR Partnership is to combine on‑device AI, low‑power compute, and advanced graphics so Specs can run context‑aware, privacy‑preserving applications directly on the glasses.

Both companies emphasize a long‑term roadmap alignment. Qualcomm sees the next era of computing as devices that understand what users see, hear, and say, while Snap aims to make computing more human and tightly integrated with the real world. For developers, the roadmap promises a scalable platform and predictable product cadence, backed by Lens Studio tools that already power AR experiences on Snapchat and other services.

How does this move fit Snap’s turnaround story?

The Snap AR Partnership lands as Snap tries to convince Wall Street it has a durable business model beyond viral messaging and ephemeral earnings. In the most recent full year, Snap’s revenue grew about 11%, and adjusted EBITDA improved by roughly 36%, while the net loss narrowed by about 34%. Analysts currently model continued progress through 2026 and 2027, with a slim profit projected around 2028 if execution stays on track.

Management’s strategy now leans on three monetization pillars: the free, ad‑supported Snapchat platform; the Snapchat+ subscription offering, which has reached roughly 24 million users; and the monetization of smaller content creators. Specs and the Snap AR Partnership add a fourth, higher‑risk lever — hardware‑enabled AR — that could create new revenue streams through devices, app stores, and premium AR experiences if adoption scales.

However, investors must balance that optionality with execution risk. Smart glasses remain a nascent category, and Snap has already spent billions on earlier Spectacles efforts that never broke out of niche status, especially as giants like Apple and NVIDIA invest heavily in their own AI and spatial computing ecosystems.

Why are activists skeptical of Specs?

Activist investor Irenic Capital Management, which holds about 2.5% of Snap’s Class A shares, has made the company a high‑profile campaign. Irenic argues that Snap could be worth roughly $35 billion, or at least $26.37 per share, far above today’s sub‑$5 quote, if management aggressively improves ad monetization with AI, cuts costs, buys back stock, and tightens governance. A controversial plank of Irenic’s plan is a call to spin off or even shut down the Specs business, which it estimates has consumed more than $3.5 billion over the years.

That stance puts the new Snap AR Partnership directly in the crosshairs. On one hand, aligning with Qualcomm could lower technology risk, improve time‑to‑market, and make Specs more compelling for developers, strengthening Snap’s negotiating position with shareholders. On the other, doubling down on AR hardware appears to run counter to Irenic’s capital‑discipline narrative. Given Snap’s dual‑class share structure and the voting control of co‑founder and CEO Evan Spiegel, activists have limited direct leverage, but the tension underscores how consequential this hardware bet has become for equity holders.

How does Snap stack up against U.S. tech rivals?

In AR and mixed reality, Snap is battling much larger players. Apple is pushing Vision Pro and a broader spatial computing ecosystem, while Meta Platforms continues to burn cash on Reality Labs and its Quest lineup. Chipmakers like NVIDIA and Qualcomm supply the compute backbone for these platforms, extracting value with far less consumer‑demand risk. Unlike Meta or Tesla, Snap is not in the S&P 500 and lacks the balance sheet of mega‑cap peers, making each capital allocation decision more critical.

On Wall Street, sentiment toward SNAP remains divided. Technical traders on platforms such as TradingView see the stock in a potential accumulation phase or early bullish reversal, but fundamental analysts remain cautious, pointing to still‑negative earnings, legal overhangs including investigations by law firms into past disclosures, and the volatility of digital ad markets. Some research shops, including ChartMill, highlight the stock’s weak profitability scores but acknowledge improving growth metrics and user engagement trends.

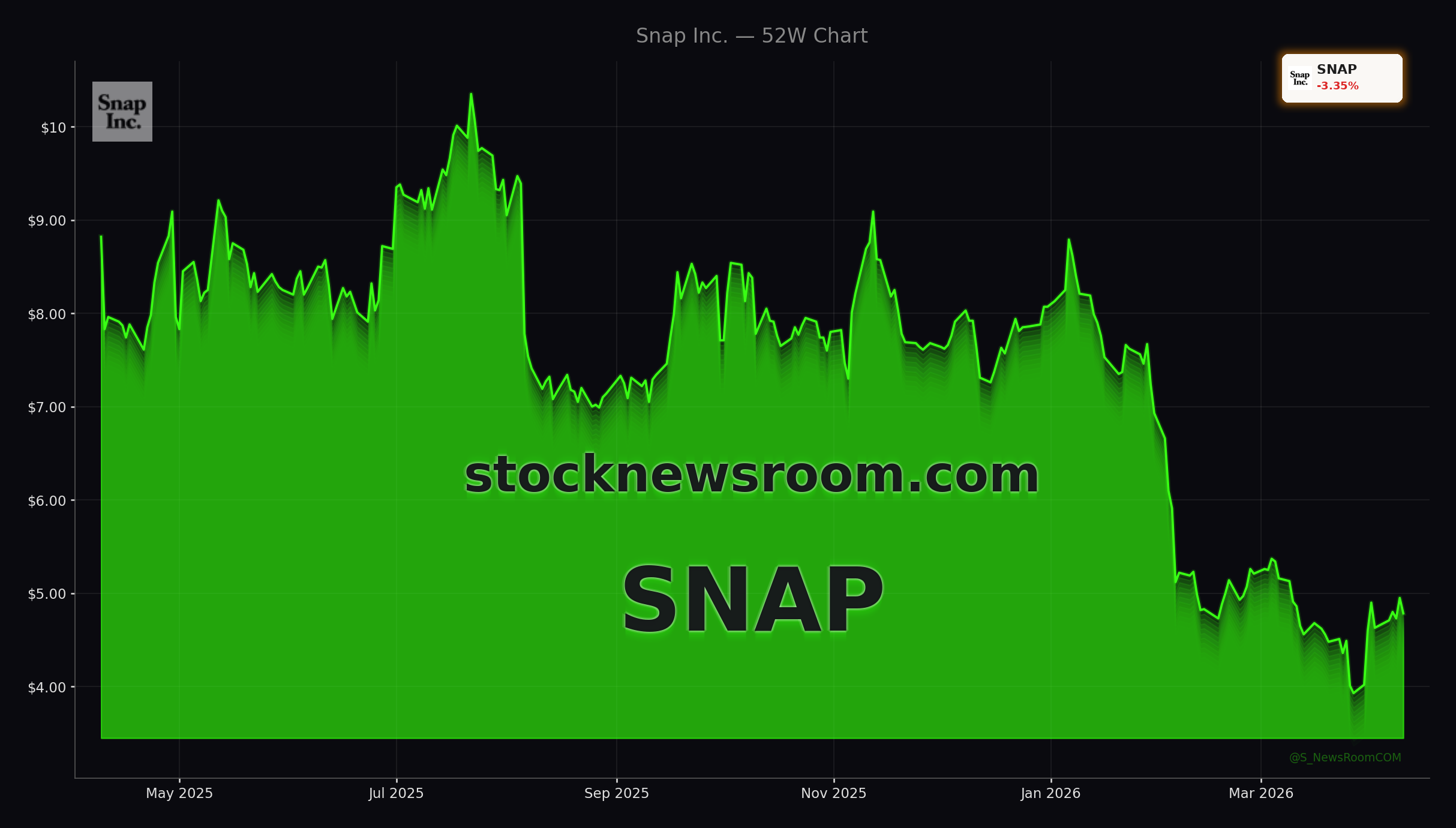

With shares down around 3.7% today to $4.76 and still far below their 52‑week high, the equity markets appear to be assigning little value to long‑dated AR hardware upside. That disconnect is exactly what both the Snap AR Partnership and activists like Irenic are attempting to close, albeit with very different playbooks.

Related Coverage: What about Snap’s regulatory risks?

Investors weighing the Snap AR Partnership should also consider regulatory headwinds. A recent deep dive on StockNewsroom, “Snap DSA Investigation -11.1% Crash Hits Snapchat Stock”, examines how an EU Digital Services Act probe triggered a sharp sell‑off and raised questions about platform safety and compliance costs. That piece highlights how regulatory shocks can quickly rerate SNAP’s valuation, even when fundamentals are improving. Any AR‑driven expansion of Snapchat’s ecosystem could draw additional scrutiny from U.S. and European regulators, amplifying both upside and downside for shareholders.

We believe the future of computing will be more human and grounded in the real world.— Evan Spiegel, co‑founder and CEO, Snap Inc.

In summary, the Snap AR Partnership with Qualcomm gives Snap a credible technology platform for its next‑generation Specs glasses, but it also magnifies the debate over hardware spending and strategic focus. For investors, SNAP remains a high‑risk, high‑reward name where small changes in execution, regulation, or user adoption can have outsized impact on valuation. The next few product launches and quarterly reports will show whether this AR push becomes a true growth engine or another costly experiment — but for now, the partnership keeps Snap firmly on the radar of growth‑oriented portfolios.