Is the Snowflake Lawsuit just legal noise, or the catalyst that finally forces investors to rethink this high-multiple cloud favorite?

Is Snowflake facing a perfect storm?

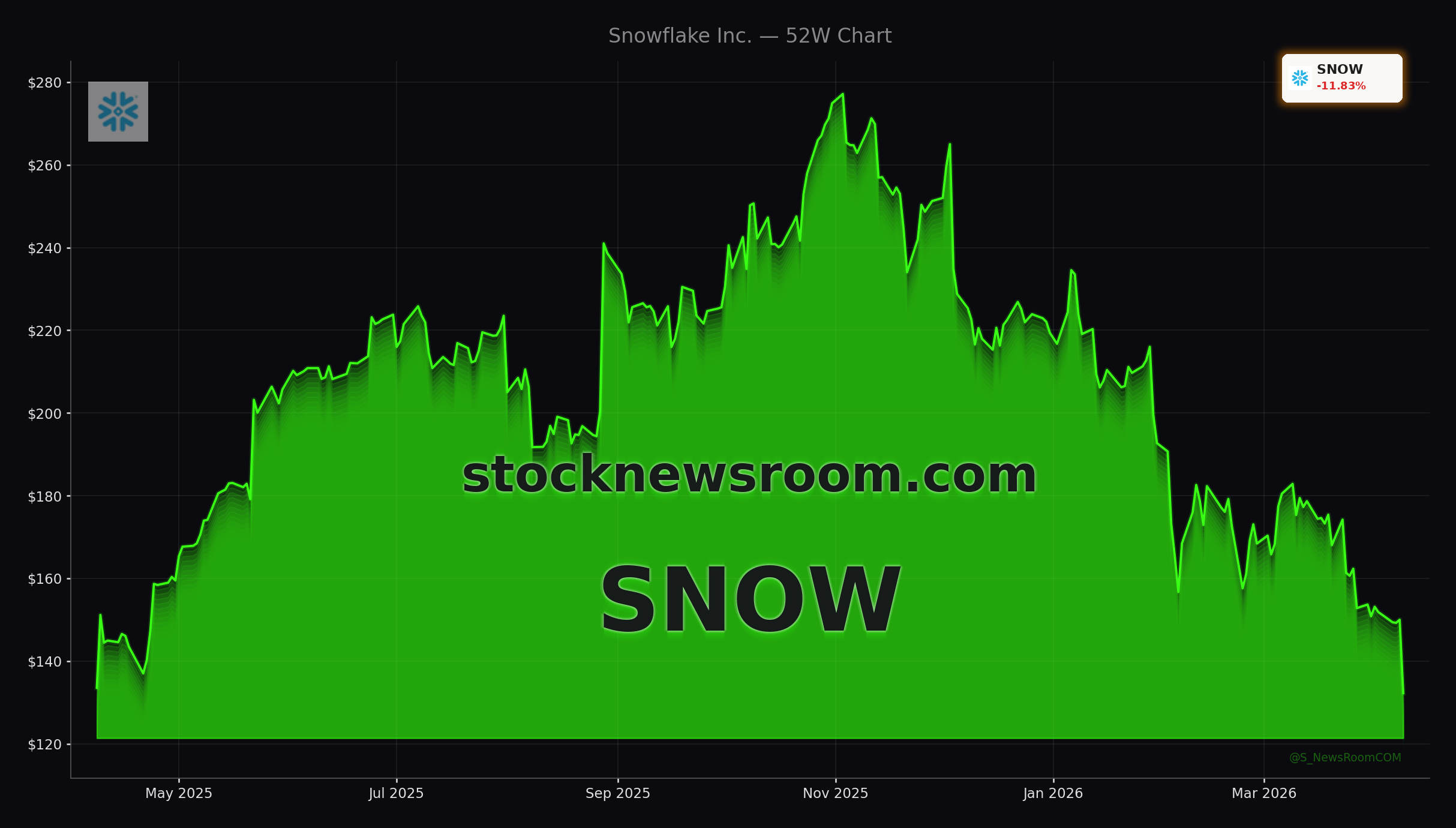

Snowflake Inc. Sammelklage und Insidertransaktionen are now front and center for U.S. tech investors. Snowflake (SNOW) closed at $132.24 on Thursday, down 11.83% from the prior $150.39 close, with after-hours trading slipping slightly to $132.00. The move comes as a series of securities fraud class actions pile up, all anchored around the same narrative: that Snowflake allegedly misled the market about how product efficiency gains and new storage pricing would hit consumption-based revenue.

The core Snowflake Lawsuit allegations span a class period from June 27, 2023, through the close of trading on February 28, 2024. Investors who bought within that window and suffered losses are being urged by multiple firms to seek lead-plaintiff status before the April 27, 2026 deadline. For portfolios heavily tilted to high-growth cloud and AI beneficiaries like NVIDIA or Apple, the episode is a stark reminder of the legal and execution risks that can lurk beneath premium valuations.

What exactly is the Snowflake Lawsuit about?

The various complaints accuse Snowflake and certain executives of violating federal securities laws by making overly optimistic or misleading statements about customer usage, product developments and revenue visibility. Central to the Snowflake Lawsuit are claims that management highlighted strong demand while allegedly failing to disclose that product efficiency gains, the rollout of Iceberg Tables and tiered storage pricing were expected to materially reduce customer consumption and, by extension, revenue growth.

Law firms including Kaplan Fox & Kilsheimer, Bernstein Liebhard, Bronstein Gewirtz & Grossman, The Gross Law Firm, the Schall Law Firm and Rosen Law Firm are all seeking to represent shareholders. The suits broadly argue that Snowflake’s upbeat commentary about consumption trends and demand lacked a reasonable basis, and that once the underlying reality became clear, investors experienced significant losses as the stock repriced.

Importantly for U.S. investors, no class has yet been certified, and shareholders are free either to petition to become lead plaintiff or to remain passive class members. The April 27, 2026 cutoff is about who directs the litigation, not whether investors can benefit from any eventual settlement or judgment.

How do insider transactions shape the narrative?

Overlaying the Snowflake Lawsuit is an eye‑catching pattern of insider activity. A fresh Form 4 filed with the SEC shows co‑founder and director Benoit Dageville recorded a gift of 1,567,652 Class A shares on April 7, 2026. While the transaction is recorded at $0.00 as a transfer, it comes on top of a long trail of open‑market sales by Snowflake insiders over the past several quarters.

Data from recent months highlight repeated selling by senior figures including Chairman Frank Slootman, Dageville himself, and other executives such as Christian Kleinerman and Vivek Raghunathan. Many of those transactions were executed under pre‑arranged Rule 10b5‑1 trading plans, and insider selling alone does not prove wrongdoing. However, in the context of a fast‑growing list of securities suits, the optics of heavy insider monetization near higher price levels could weigh on investor confidence.

For institutional money managers benchmarked to the NASDAQ and S&P 500 growth segments, the combination of legal uncertainty and aggressive insider selling often triggers fresh risk reviews. Position sizes may be trimmed, option hedges increased, or new purchases deferred until key litigation milestones are visible.

How does Snowflake compare with other tech names?

Snowflake has been a high‑beta way to play the growth of data‑driven cloud and AI workloads, often mentioned in the same breath as NVIDIA, Tesla and other high‑multiple innovators. Unlike mature mega‑caps that enjoy diversified revenue streams, Snowflake remains more exposed to swings in customer consumption and to perception risk around its long‑term model.

For now, the Street’s major banks have not publicly overhauled ratings in response specifically to the Snowflake Lawsuit headlines, but the legal overhang could influence future calls from firms such as Goldman Sachs, Morgan Stanley, Citigroup or RBC Capital Markets as they reassess valuation versus execution risk. If growth decelerates faster than expected because efficiency gains outpace new workload adoption, earnings models and price targets may need to be cut.

In contrast, some large‑cap peers in cloud infrastructure and AI hardware have recently rallied on clearer demand narratives and lower legal noise. That divergence underscores why active managers are increasingly discriminating within high‑growth tech, rather than treating the sector as a monolith.

Related coverage for Snowflake investors

Investors looking for deeper context on market psychology around Snowflake can review the recent analysis “Snowflake Class Action: -7.4% Plunge Shocks Investors“, which explores how earlier legal headlines triggered a sharp stock drop and widened the debate on long‑term confidence in the data‑cloud story. For a broader sector angle, “Intel Google Partnership +4.7% Rally Shocks Wall Street” examines how an AI‑focused collaboration in semiconductors is reshaping sentiment for legacy chip players, offering a useful contrast to Snowflake’s current legal headwinds.

In sum, the expanding Snowflake Lawsuit, combined with notable insider transactions and a steep share‑price pullback, creates a complex setup for U.S. investors. The stock remains a high‑profile play on cloud data and AI, but carries elevated legal and perception risk that may not fit every risk budget. The next key milestones will be court decisions on class certification and any updates from management on how efficiency‑driven revenue headwinds are evolving, and those developments will help determine whether the current volatility ultimately proves to be a buying opportunity or a warning sign.