Is the SolarEdge Turnaround finally turning into a durable AI‑power rally, or just another short squeeze in a volatile solar cycle?

Is SolarEdge Back On Wall Street’s Radar?

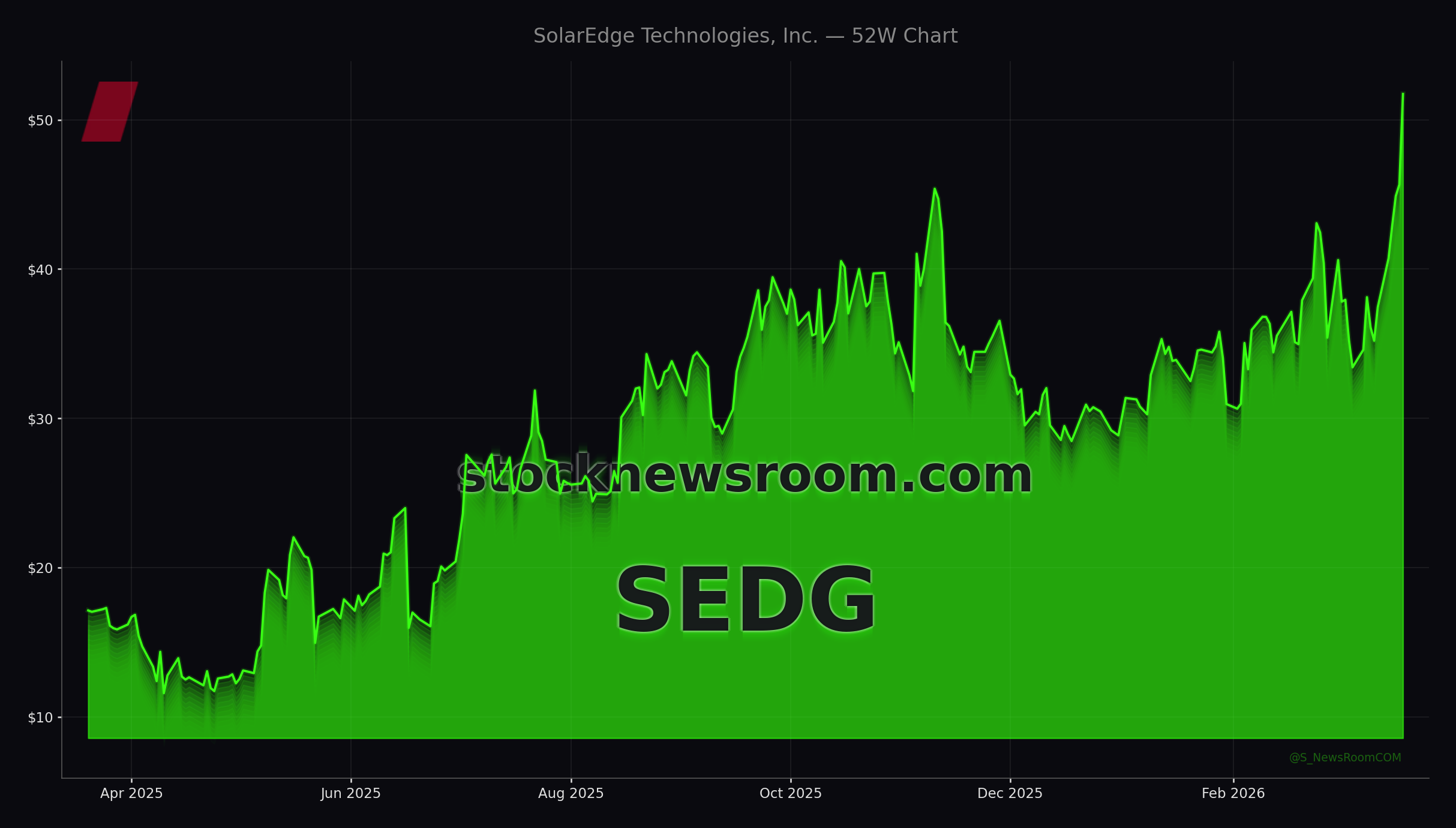

Solar stocks roared higher on Friday as investors piled into names leveraged to rising electricity demand from AI data centers, clean energy policies and expectations for lower interest rates. SolarEdge Technologies, Inc. led the move, closing up more than 13% at $51.73, with modest additional gains in after‑hours trading.

The stock has now tripled over the past year but remains roughly 81% below its five‑year highs near $280, underscoring how early the SolarEdge Turnaround still is. For U.S. investors, SEDG has quickly shifted from a tax‑loss candidate to a high‑beta way to play the intersection of solar power, grid modernization and AI infrastructure, alongside semiconductor leaders like NVIDIA and hyperscale plays that are scrambling for power capacity.

Sector‑wide, the rally also lifted peers such as Canadian Solar and Enphase Energy, but the market is increasingly differentiating between a genuine operational repair story at SolarEdge and more speculative bounces in other solar names.

How Strong Is SolarEdge’s Operational Recovery?

The backbone of the SolarEdge Turnaround is improving execution and a much healthier balance sheet. In Q4 2025, SolarEdge reported revenue of $335.36 million, up 96.4% year over year, signaling a sharp rebound in demand for its core inverter and smart energy solutions. Non‑GAAP gross margin widened to 23.3%, the fifth consecutive quarter of margin expansion and a key confirmation that price discipline and cost controls are sticking.

Cash flow tells an even more dramatic story: operating cash flow swung to a positive $104.26 million for full‑year 2025 from negative $313.32 million in 2024. That shift from heavy cash burn to self‑funding operations is central to the SolarEdge Turnaround narrative and reduces the risk of dilutive equity raises that previously weighed on the stock.

Management is positioning 2026 as a pivot year. CEO Shuki Nir has called 2026 “transformational” for SolarEdge, highlighting the company’s Nexis platform and power solutions aimed at AI data centers and large‑scale commercial customers. With cloud players and chip vendors like NVIDIA and Intel racing to add capacity, the ability to deliver efficient power electronics and storage systems could open higher‑margin, utility‑scale opportunities beyond traditional rooftop solar.

What Role Do Europe And New Products Play?

Another building block in the SolarEdge Turnaround is product expansion in key international markets. This week, SolarEdge launched its next‑generation three‑phase SolarEdge Nexis residential solar and storage system in Germany, one of Europe’s largest rooftop solar markets. The system allows homeowners to scale battery capacity in small steps, supporting higher self‑consumption and grid resilience while potentially unlocking better economics for installers.

Europe has been a pain point for the company, with unsold inventory piling up amid slower‑than‑expected demand in recent years. But volatility in European energy prices and renewed interest in energy independence, especially in light of Middle East tensions and oil market disruptions, are reviving order activity. The ability to monetize older inventory and ramp Nexis deployments could provide both margin support and working‑capital relief in 2026.

For U.S. portfolios, the European reset matters because it reduces regional risk concentration and makes SolarEdge less dependent on any single residential cycle. It also positions the company to benefit if EU green‑energy incentives and grid‑upgrade spending accelerate.

What Are Jefferies And TD Cowen Saying About SolarEdge?

Wall Street is cautiously warming to the SolarEdge Turnaround. On Friday, Jefferies analyst Julien Dumoulin‑Smith upgraded SolarEdge from “underperform” to “hold” and raised his price target from $30 to $49 per share. The stock immediately traded above that level, underscoring how fast sentiment is shifting as investors re‑price the recovery story.

Jefferies is not yet outright bullish, pointing out that the stock is still deeply below its long‑term peak and that recent sales trends remain uneven, with profitability not yet fully restored. Even so, the firm flagged the Middle East conflict and resulting energy price volatility as catalysts that could accelerate solar adoption, particularly in Europe, and improve SolarEdge’s ability to work down inventory and stabilize margins.

Earlier this year, TD Cowen also nudged expectations higher, lifting its price target on SEDG to $43 from $38 after the Q4 2025 report and highlighting the company’s improving fundamentals. The fact that the stock now trades well above those targets suggests the market is betting the SolarEdge Turnaround has more runway than early‑2026 models assume, but also that expectations are rising and execution risk is back in focus.

How Does SolarEdge Stack Up Against U.S. Peers?

Compared with U.S.‑listed rival Enphase Energy and panel maker peers, SolarEdge sits at an interesting intersection of risk and reward. Unlike mega‑cap tech winners such as Apple or Tesla, SEDG is not part of the S&P 500 and remains a mid‑cap name with higher volatility, which can amplify both gains and drawdowns in diversified portfolios.

Whereas Canadian Solar is bouncing off multi‑year lows with a still‑uncertain transition, SolarEdge’s rally is increasingly grounded in tangible margin and cash‑flow improvement. That makes the SolarEdge Turnaround more than just a macro or rate‑cut bet; it hinges on whether the company can continue to execute on its Nexis rollout, tap AI‑related power demand and manage competition in inverters and storage.

2026 will be a transformational year for SolarEdge.— Shuki Nir, CEO of SolarEdge Technologies, Inc.

For U.S. investors, SEDG is evolving into a tactical way to gain exposure to global solar electrification and AI infrastructure spending without paying mega‑cap tech valuations, albeit with significantly higher risk.