Is the S&P 500 quietly pricing in a soft landing while recession risk builds beneath the surface?

Is S&P 500 Recession Risk underpriced?

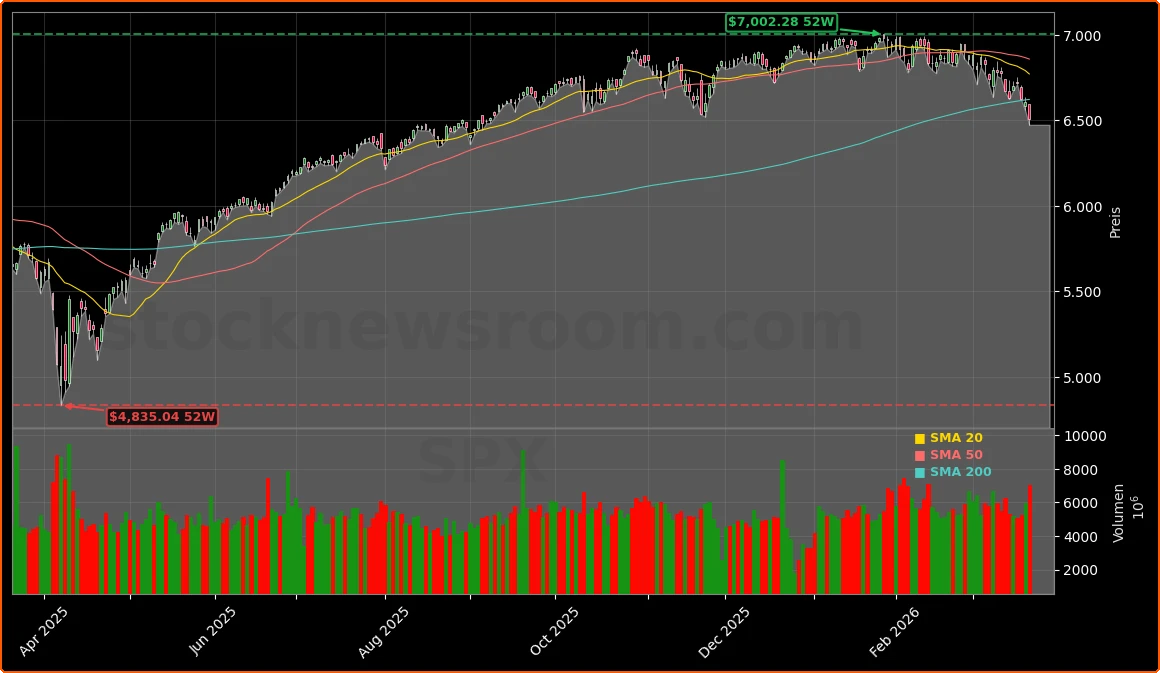

The S&P 500 recently traded near 6,506, about 1.5% below the previous close of 6,606, after a long stretch of strength that left U.S. benchmarks outperforming Europe. While the pullback has grabbed headlines, the broader picture suggests that S&P 500 Recession Risk may still be underestimated. Equity valuations remain elevated versus historical averages, and earnings estimates have only modestly adjusted for a softer macro backdrop.

Strategists on Wall Street point out that the index level around 6,600 does not yet embed a classic mild recession playbook. In a typical cyclical downturn, consensus earnings are cut more deeply and price-to-earnings multiples compress as investors demand higher risk premia. So far, revisions have been incremental, not aggressive. That leaves portfolios exposed if growth data in coming quarters confirm a more persistent slowdown.

For U.S. investors, the implication is straightforward: the market is still priced closer to a soft-landing or mid‑cycle cooling scenario than to a full-blown recession. If the economy merely slows, current levels may prove justified, but if activity slips into contraction, the repricing could be abrupt rather than gradual.

How deep could a downturn hit the index?

The central debate around S&P 500 Recession Risk now revolves around the depth of a potential downturn. Market strategists differentiate sharply between a mild and a severe recession. In a mild scenario, with only a short-lived contraction in GDP and contained job losses, the downside for the S&P 500 from current levels might be limited to a mid‑teens percentage decline as earnings are trimmed and multiples adjust.

A severe recession is a different story. In that case, history suggests that global indices could undergo corrections of well over 20% to 25% from recent peaks, as investors rapidly reprice both profit expectations and credit risk. For the S&P 500, that could mean a slide far below current levels, with cyclical sectors such as industrials, consumer discretionary, and parts of financials bearing the brunt.

Importantly, the recent modest drop of roughly 1.5% from the latest close offers little real cushion against a severe scenario. Volatility may also increase if bond markets price in more aggressive Federal Reserve easing in response to weakening data, putting additional focus on earnings quality and balance sheet strength across the index.

What does this mean for NVIDIA, Apple and Tesla?

S&P 500 Recession Risk is particularly relevant for the large-cap growth and technology names that have driven much of the index’s advance. NVIDIA, Apple and Tesla together carry significant weight in the S&P 500 and Nasdaq, meaning any repricing in these stocks quickly feeds through to broader benchmarks.

So far, many investors still view mega-cap tech as relatively resilient: robust balance sheets, strong cash generation and structural growth themes such as AI and cloud computing support the bull case. However, even these names are not immune if earnings expectations prove too optimistic or if multiples compress from elevated levels. A broad-based de-rating across growth leaders could magnify index declines beyond what a simple GDP slowdown would suggest.

Citigroup, Goldman Sachs and Morgan Stanley have recently highlighted in their strategy notes that concentration risk in a handful of mega caps increases portfolio vulnerability if sentiment turns. While they differ on exact targets, they broadly caution that investors should stress-test their exposure to these leaders under both mild and severe recession scenarios instead of assuming that the group will remain a one-way hedge.

How are analysts framing S&P 500 Recession Risk?

Equity strategists at major U.S. banks are increasingly explicit about the gap between current pricing and classic recession playbooks. RBC Capital Markets has emphasized that past severe recessions typically coincide with earnings contractions of 15% to 25% and meaningful multiple compression, neither of which is fully visible in current consensus numbers. Goldman Sachs, by contrast, remains more constructive, arguing that a soft landing is still the base case, though it acknowledges that downside risks are rising.

For portfolio managers, the takeaway is that S&P 500 Recession Risk is less about predicting the exact GDP print and more about understanding how far earnings and valuations could realistically fall if conditions deteriorate. That means closely tracking guidance in upcoming earnings seasons, watching leading indicators such as ISM surveys and jobless claims, and assessing whether credit spreads begin to widen more materially.

The index level around 6,600 does not yet look like a classic recession discount; investors are still paying a soft-landing price for increasingly uncertain growth.— Senior U.S. equity strategist at a major Wall Street bank

Against this backdrop, investors are increasingly distinguishing between high-quality balance sheets and more leveraged business models. Companies with strong free cash flow, ample liquidity and pricing power may still weather a downturn with smaller valuation hits, while weaker names could face outsized drawdowns if financing conditions tighten.