Is Super Micro’s AI server boom strong enough to outgrow legal probes, margin pressure and rising doubts on Wall Street?

Is Super Micro still an AI winner for Wall Street?

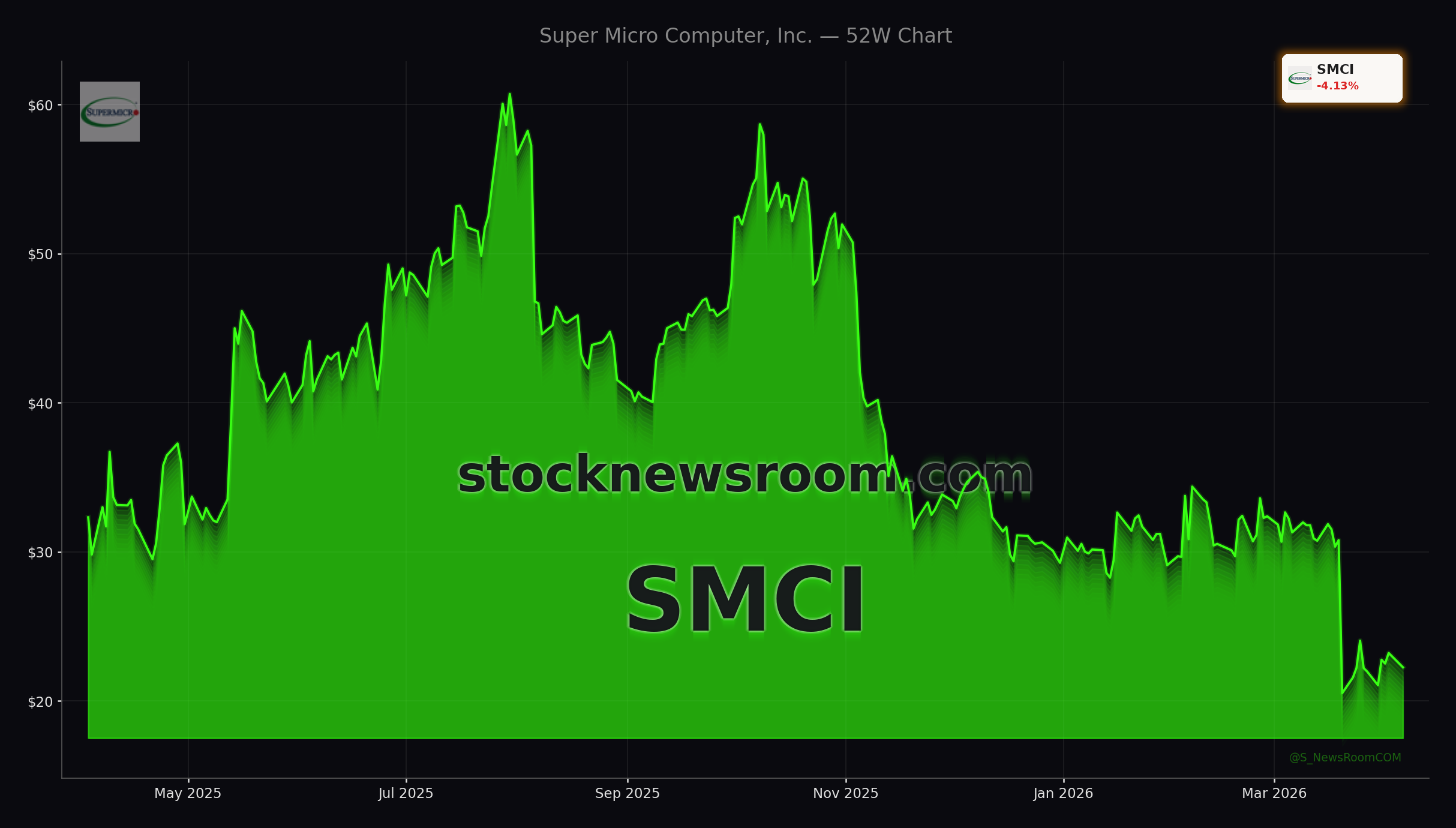

At today’s close of $22.21 (previous close $23.20), Super Micro (SMCI) trades on a forward P/E around the high teens and a price-to-sales ratio near 1, far below premium AI beneficiaries like NVIDIA or hyperscale cloud names. The stock remains tightly linked to the AI build-out because Super Micro designs and assembles GPU‑rich servers, liquid‑cooled racks and energy‑efficient systems that underpin modern data centers. Yet the latest Super Micro Analysis shows that this growth story is overshadowed by legal, governance and competitive concerns that now dominate the narrative on NASDAQ.

From a macro perspective, Super Micro is trying to ride the same “picks-and-shovels” AI wave that propelled chip designers and accelerator suppliers into the market’s top tier. But while demand for AI server capacity is robust through at least 2027, investors are increasingly questioning whether this particular vendor will capture that upside, or whether rivals such as Dell and other Taiwanese manufacturers end up taking the lion’s share.

How damaging are the legal probes for Super Micro Computer?

The stock’s latest leg down was triggered by U.S. federal charges involving alleged smuggling of AI hardware to China, with three individuals — including a Super Micro co‑founder — accused of moving roughly $2.5 billion of advanced technology in violation of export controls. Multiple investor-rights firms, including Rosen Law Firm, Faruqi & Faruqi and Robbins Geller, have launched securities class actions and investigations focused on whether Super Micro misled shareholders on compliance with U.S. export laws.

Class period definitions generally span from spring 2024 through March 19, 2026, giving a sense of how long investors may have been exposed to undisclosed risks. One investigation cites a nearly 28.5% single‑day share price drop following the Reuters report on the charges, underscoring the market’s sensitivity to governance issues. This legal overhang feeds directly into Super Micro Analysis on valuation: even a low multiple can be justified if investors anticipate fines, compliance costs, management changes or potential disruption to key supplier and customer relationships.

Crucially, Super Micro’s tight relationship with NVIDIA is under fresh scrutiny. GPU‑centric products reportedly account for more than two‑thirds of Super Micro’s revenue, yet the partnership is not locked in with a long‑term supply contract. Any move by NVIDIA to distance itself from Super Micro due to compliance concerns would hit the business model at its core and could reshape the AI server landscape overnight.

Super Micro Analysis: Are fundamentals holding up?

Beyond the legal headlines, recent operating trends raise their own questions. In the latest reported quarter, net sales fell about 15% year over year to roughly $5.0 billion, despite the ongoing global AI data center capex boom. Over the same period, major partners like NVIDIA delivered rapid revenue growth, highlighting a widening gap between chip suppliers and system integrators like Super Micro.

Margin pressure is just as worrying. Gross margin dropped from about 13.1% to 9.3%, as competition intensified and low‑cost Taiwanese rivals undercut pricing with servers reportedly sold at margins near 4%. Historically, Super Micro justified a premium on the strength of its custom designs, rapid time‑to‑market and power‑efficient configurations. The latest Super Micro Analysis suggests that moat may be eroding, leaving the company exposed in a commodity‑leaning segment where scale and procurement leverage are critical.

Still, there is a valuation cushion. At a forward P/E near 17–18 versus an S&P 500 average around 22, and trading well below consensus price targets in the mid‑$30s, the stock already embeds substantial pessimism. Hedge funds have built short positions to roughly 14% of float, indicating that professional investors are actively betting against a near‑term rebound, but also setting up the possibility of a sharp squeeze if sentiment unexpectedly turns.

What are Mizuho and other analysts signaling?

Analyst rhetoric has cooled considerably. Mizuho on Monday cut its price target for Super Micro from $33 to $25 while maintaining a “Neutral” rating. The firm cited near‑term risks from export‑control controversies and federal indictments, warning that some orders could shift toward Dell as customers seek vendors with lower compliance risk. Mizuho nonetheless acknowledged strong long‑term AI server demand, implying that the fundamental market backdrop is intact even if Super Micro’s share of that pie is in doubt.

Earlier, some analysts had highlighted better‑than‑expected earnings per share of $0.69 versus a $0.49 consensus and quarterly revenue of $12.68 billion. Yet the stock’s inability to respond positively to the beat shows how dominant the legal and governance narrative has become in Super Micro Analysis. For now, ratings skew toward “Hold” or “Neutral,” with relatively modest upside implied from today’s price and a wide dispersion of views on legal outcomes and customer behavior.

Related Coverage: A deeper dive into the compliance and export-control dimension can be found in Super Micro Computer Investigations: +8.1% Surge Amid Legal Shock, which examines how legal probes intersect with the company’s $40 billion AI ambitions and what that might mean for institutional investors on Wall Street.

In summary, the current Super Micro Analysis paints a company caught between robust structural demand for AI infrastructure and a self‑inflicted credibility crisis that clouds both its customer pipeline and its crucial GPU supply relationships. For U.S. investors, the stock’s discounted valuation and AI leverage are intriguing but sit squarely against legal risk, governance questions and intensifying competition. The next phases in the export‑control cases, any governance overhaul and upcoming quarters will determine whether Super Micro belongs in high‑risk AI baskets or remains sidelined as a cautionary tale of growth under pressure.