Can a booming AI business outweigh legal turmoil and China export risks in shaping the Super Micro Computer Forecast?

Is Super Micro Computer Forecast clouded by Mizuho cut?

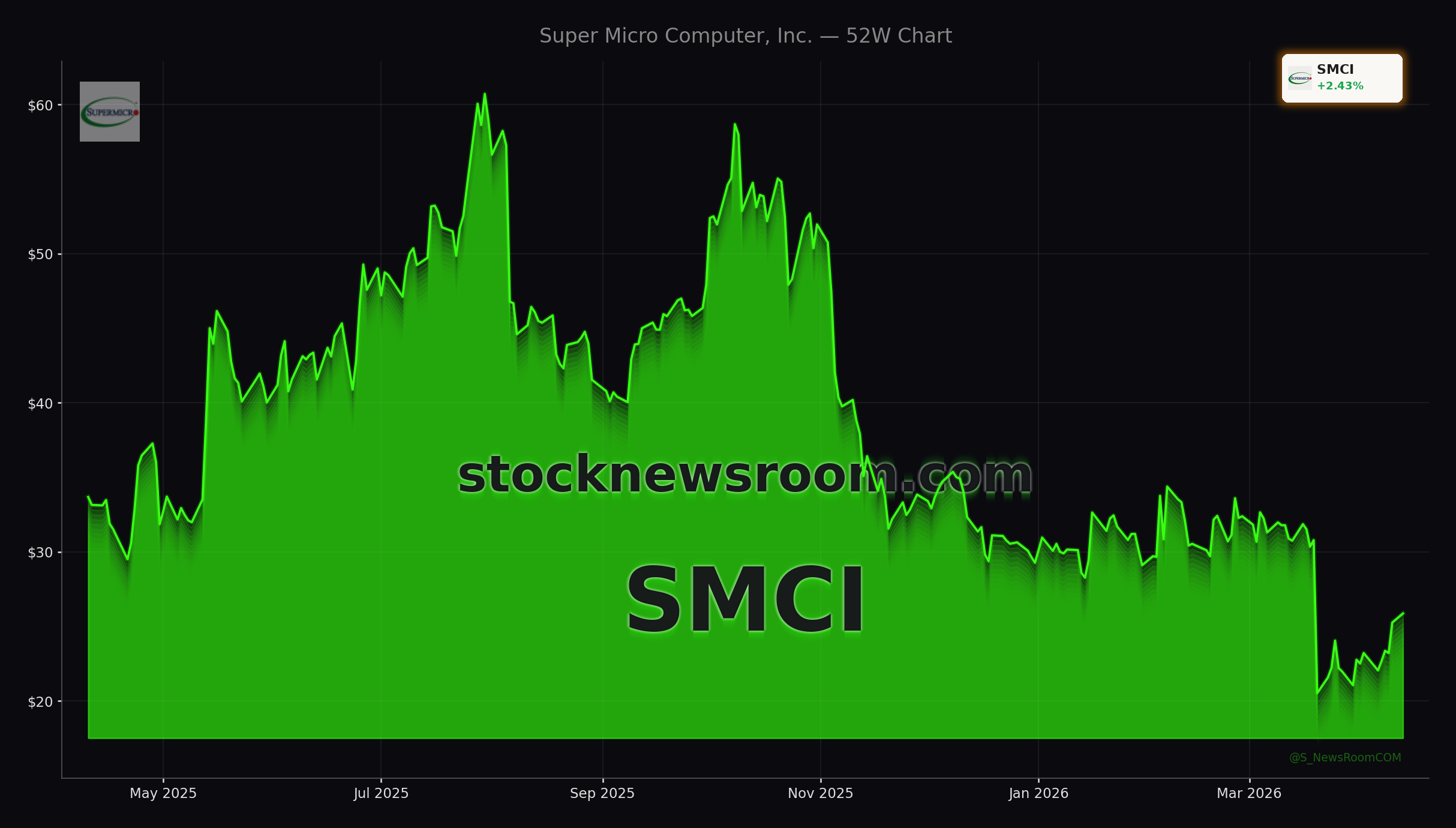

Super Micro Computer, Inc. shares closed at $25.68 on Monday, up 1.64% from the prior close but still far below the 52‑week high of $62.36 reached in late July, according to recent trading data. That rebound has not stopped Mizuho from taking a more cautious stance. On April 6, the bank lowered its price target for SMCI to $25 from $33 while maintaining a Neutral rating, effectively signaling that today’s price already reflects its near‑term expectations.

Mizuho still expects robust AI server demand through 2026–2027, driven by continued hyperscaler capex and accelerating enterprise AI rollouts. However, the firm warned that export‑control uncertainty around China and intensifying competition from Dell and Hewlett Packard Enterprise could pressure margins and create order volatility. For U.S. investors, the updated Super Micro Computer Forecast from Mizuho points to a classic risk‑reward trade‑off: powerful secular growth, but with headline risk that could keep valuation multiples in check.

How do legal and China risks hit Super Micro Computer, Inc.?

The greatest overhang on the Super Micro Computer Forecast now comes from legal exposure tied to alleged export‑control violations. Co‑founder Yih‑Shyan Liaw has pleaded not guilty in U.S. federal court over accusations that Nvidia‑powered servers were diverted to China in violation of export rules. Multiple securities class‑action suits have followed, claiming investors were misled about compliance and sales practices.

Law firms including Rosen Law Firm and Kahn Swick & Foti are soliciting shareholders who bought SMCI stock between early 2024 and March 19, 2026, to seek lead‑plaintiff status in federal cases. Another suit highlighted by Faruqi & Faruqi focuses on alleged misstatements around exports to Chinese customers. These actions could lead to sizable legal costs, potential settlements, and sustained reputational damage, especially with Washington tightening controls on advanced AI hardware shipped to China.

For global portfolio managers, this backdrop raises questions about Super Micro’s ability to navigate the same geopolitical fault lines that have forced NVIDIA and other U.S. chip leaders to rework China strategies. While the underlying demand for high‑performance AI servers remains strong, any additional export restrictions or adverse court rulings could add new downside scenarios to the Super Micro Computer Forecast.

Does AI growth still support a positive Super Micro Computer Forecast?

Despite the legal noise, the operating story behind SMCI remains compelling. The company recently reported 123% year‑over‑year revenue growth, easily topping Wall Street expectations and sending the stock up around 8% in a single session. At the same time, Super Micro rolled out its new Gold Series of pre‑configured enterprise servers—more than 25 systems built on its existing architecture—to make AI infrastructure deployments faster and simpler for corporate IT teams.

Super Micro is also pushing hard into edge AI. New compact, energy‑efficient systems powered by AMD EPYC 4005 processors target space‑ and power‑constrained use cases in retail, manufacturing, and healthcare. These mini‑1U, short‑depth rack, and slim‑tower designs aim to bring inferencing and real‑time analytics closer to where data is generated, a trend that could complement data‑center demand rather than cannibalize it.

Industry forecasts for 2026 IT spending add another tailwind. As data‑center operators expand capacity to support generative AI and high‑performance computing, Super Micro’s “building‑block” approach—with rapid design cycles and close alignment to GPU partners like NVIDIA—positions it to win share even against giants like Dell and Hewlett Packard Enterprise. For growth‑oriented investors, that operating momentum continues to support a constructive Super Micro Computer Forecast beyond the current legal cycle.

How does SMCI stack up for U.S. tech investors?

From a U.S. portfolio standpoint, SMCI sits at the crossroads of several themes: AI infrastructure, reshoring and export controls, and elevated market volatility across high‑beta tech. The stock is not in the S&P 500, but it trades on the NASDAQ alongside AI bellwethers such as NVIDIA, Tesla, and Apple, and has become a favored vehicle for investors seeking leveraged exposure to AI servers via products like the GraniteShares 2x Long SMCI Daily ETF.

Volatility cuts both ways. After a steep decline from last year’s peak, the recent rebound suggests investors are reassessing worst‑case legal outcomes and refocusing on fundamentals. Yet the cluster of class actions and the open Justice Department probe mean that any new headline could spark sharp intraday swings. That makes position sizing and risk management critical, especially for retail traders using leveraged ETFs instead of the common stock.

Valuation also looks more balanced after the pullback. With the stock well below its 52‑week high but revenue still growing triple digits, the market appears to be applying a sizable “legal discount” to the Super Micro Computer Forecast. If SMCI can demonstrate stronger compliance controls, settle or narrow key lawsuits, and sustain its growth trajectory in data‑center and edge AI, there is room for multiple expansion. Conversely, a negative turn in the legal saga or tighter‑than‑expected export rules on AI servers bound for China would likely cap near‑term upside.

Related Coverage

Investors looking for a deeper dive into the tug‑of‑war between growth and risk can read Super Micro Analysis -4.3%: AI Growth vs Legal Shock, which examines whether the company’s AI server boom can outpace mounting legal probes, margin pressure, and growing skepticism on Wall Street. That analysis complements the current Super Micro Computer Forecast by exploring how valuation and sentiment may evolve as new developments emerge.

In summary, the Super Micro Computer Forecast now hinges on whether blistering AI‑driven growth can outrun legal and geopolitical headwinds tied to China exports. For U.S. investors, SMCI offers high‑beta exposure to one of tech’s strongest secular themes, but with a legal overhang that justifies careful sizing and close monitoring. The next catalysts—updates on class‑action progress, regulatory clarity, and upcoming earnings—will determine whether today’s risk discount narrows or becomes a more permanent feature of the stock’s story.