Can Super Micro Computer Investigations derail the company’s $40 billion AI ambitions just as the stock shows signs of a rebound?

How are Super Micro Computer Investigations moving the stock?

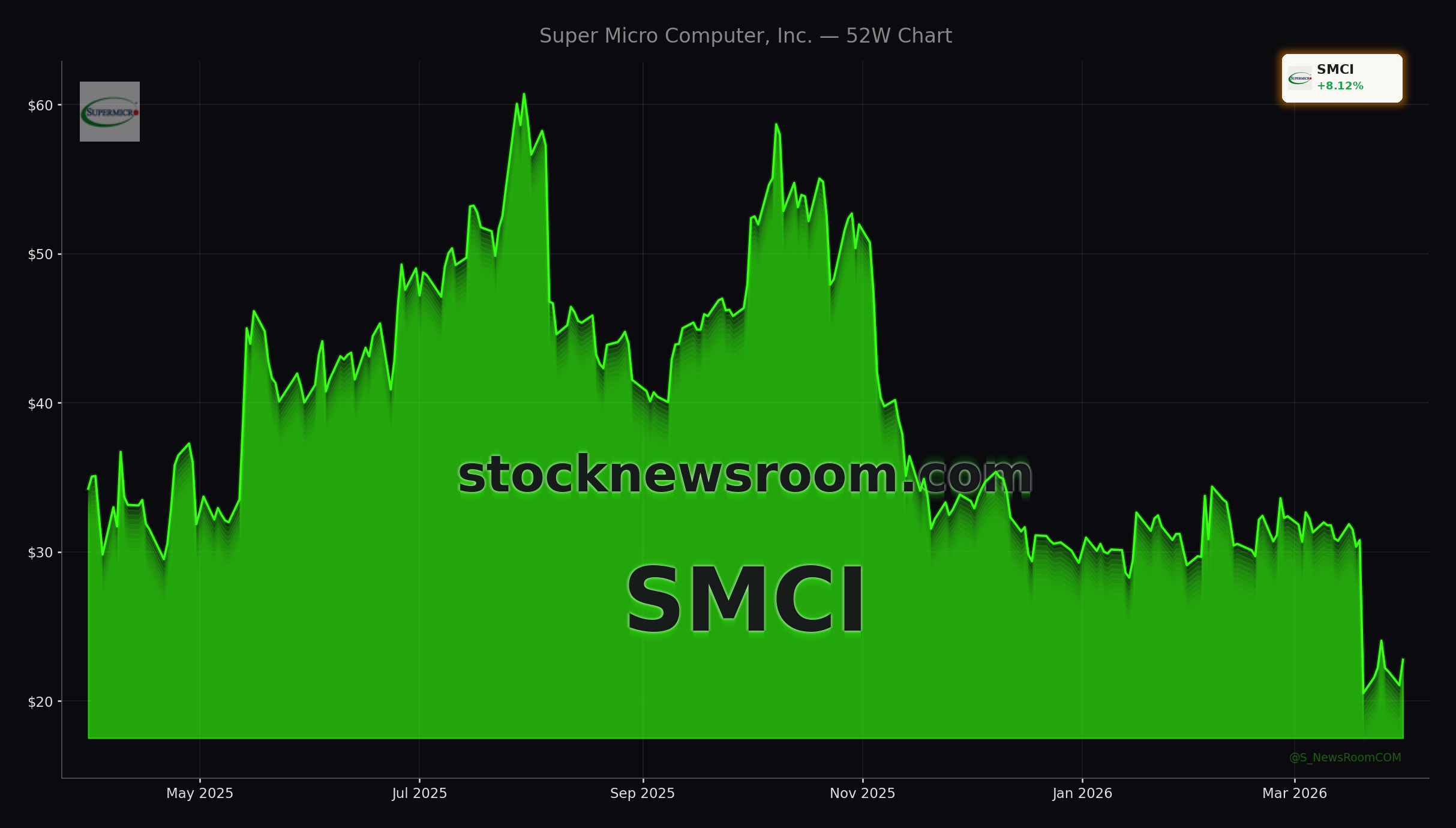

On Tuesday, SMCI traded higher to $22.77, up 8.12% from the prior close of $20.85, before slipping modestly in after-hours trading to $22.67. Even after the bounce, the stock remains well below its 52-week high of $62.36, reflecting how deeply the Super Micro Computer Investigations have reshaped sentiment. Year to date, shares are still down more than 28%, and roughly 38% over the past 12 months, underscoring persistent skepticism on Wall Street.

The immediate catalyst for the selloff in March was the arrest of board member and co-founder Yih-Shyan “Wally” Liaw, who faces charges tied to an alleged scheme to route servers with NVIDIA GPUs into China via third countries. An employee and a contractor have also been indicted, though Super Micro itself has not been charged and maintains that the individuals acted against company policy. Nonetheless, the reputational damage has been significant, as investors evaluate whether export-control issues could ultimately threaten access to critical components and key hyperscale customers.

At the same time, broader macro factors have occasionally provided support. A calmer tone around Middle East tensions and reassuring comments from the Federal Reserve about inflation have helped risk assets broadly, providing a tailwind for SMCI’s recent rebound even as legal headlines remain front and center.

What do export probes mean for Super Micro Computer and AI growth?

The heart of the Super Micro Computer Investigations narrative is the company’s dependence on advanced GPUs for its AI server platforms. SMCI integrates accelerators from NVIDIA and AMD into high-density, liquid- and air-cooled systems that underpin data centers for generative AI, cloud, and enterprise workloads. Bernstein Research has warned that any disruption in GPU allocations from key suppliers could substantially impair operations, given how central these chips are to Super Micro’s value proposition.

So far, there is no public indication that major customers have walked away, and SMCI’s own guidance points to extraordinary demand. The company has lifted its full-year fiscal 2026 revenue outlook to at least $40 billion, up from $33 billion just two quarters ago. In its most recent quarter, revenue surged to $12.68 billion, a 123% year-over-year increase, handily beating consensus expectations. Non-GAAP EPS of $0.69 also topped forecasts, suggesting the core AI business remains intact despite mounting legal scrutiny.

Management emphasizes that its Data Center Building Block Solutions and direct liquid cooling technology allow faster, more efficient deployments than traditional OEMs such as Dell Technologies and Hewlett Packard Enterprise. With manufacturing capacity expanding across the United States, Taiwan, and the Netherlands, Super Micro is positioning itself to capture global AI infrastructure demand while partially insulating itself from tariff and logistics risk that has also affected peers like Apple and other multinational tech leaders.

How serious are the lawsuits and shareholder actions?

While criminal charges have so far targeted individuals, civil exposure is escalating. A series of securities class actions filed in U.S. federal courts allege that Super Micro misled investors about compliance with U.S. export-control laws and failed to disclose material weaknesses in its controls. Several major plaintiffs’ firms are now soliciting shareholders to seek lead-plaintiff status, with key deadlines in late May 2026. Parallel derivative and fiduciary-duty investigations focus on potential board and management responsibility for any alleged misconduct.

One complaint highlights a federal indictment asserting that roughly $2.5 billion in AI server sales during fiscal 2024 and 2025 may have violated export rules, a figure that, if proven, would represent a meaningful share of the company’s $15 billion in fiscal 2024 and $22 billion in fiscal 2025 revenue. For investors, the risk profile includes potential damages, legal fees, governance reforms, and—most importantly—lasting reputational harm that could influence future contract awards.

Analyst opinion is split. Bank of America has reiterated an Underperform rating on SMCI and cut its price target, citing the risk that the Super Micro Computer Investigations could restrict access to components, weigh on margins, and accelerate customer diversification toward rival vendors. By contrast, the broader sell-side community maintains a more balanced stance, with a mix of buy, hold, and sell ratings and an average target price of $34.53, implying upside from current levels if worst-case legal outcomes do not materialize.

Can Super Micro Computer outgrow its legal overhang?

Beyond the courtroom, fundamentals remain a tug-of-war between rapid top-line expansion and mounting financial pressure. Gross margin compression is notable: GAAP gross margin has fallen to 6.3%, down sharply from 11.8% a year earlier, reflecting aggressive pricing and the heavy cost of scaling complex AI systems. Total liabilities have climbed above $21 billion, more than five times higher than a year ago, while operating cash flow turned negative in the first half of fiscal 2026.

For U.S. and global investors, the key debate is whether SMCI is an undervalued way to participate in the AI server boom or a value trap weighed down by Super Micro Computer Investigations and governance questions. Bulls argue that with AI infrastructure spend still accelerating and rivals like Tesla building out their own AI clusters, demand for high-density, energy-efficient servers should remain robust for years. Bears counter that legal uncertainty, thinner margins, and growing balance-sheet leverage make the risk-reward less compelling than large-cap chipmakers or diversified cloud platforms.

Related Coverage

For a deeper dive into how legal risks have already shaken investor confidence, including an -8.2% plunge in the wake of earlier headlines, readers can review Super Micro Computer Lawsuit: -8.2% Plunge Tests AI Boom. That analysis explores how previous lawsuit developments intersected with SMCI’s explosive AI growth narrative and set the stage for the current phase of Super Micro Computer Investigations.

Super Micro is scaling rapidly to support large AI and enterprise deployments while continuing to strengthen our operational and financial execution.— Charles Liang, CEO of Super Micro Computer, Inc.

In the end, the Super Micro Computer Investigations have turned SMCI into one of the most polarizing AI stocks on the NASDAQ. The company’s ambition to surpass $40 billion in revenue and its central role in next-generation data centers keep the growth story alive, but litigation and export-control scrutiny remain powerful headwinds. The next few quarters, including any updates on legal proceedings and GPU supply, will likely determine whether SMCI is remembered as a high-risk detour or a resilient winner of the AI infrastructure race.