Can Super Micro Computer’s explosive AI growth outrun a deepening lawsuit storm and a sharp share-price plunge?

Super Micro Computer Lawsuit: How big is the hit?

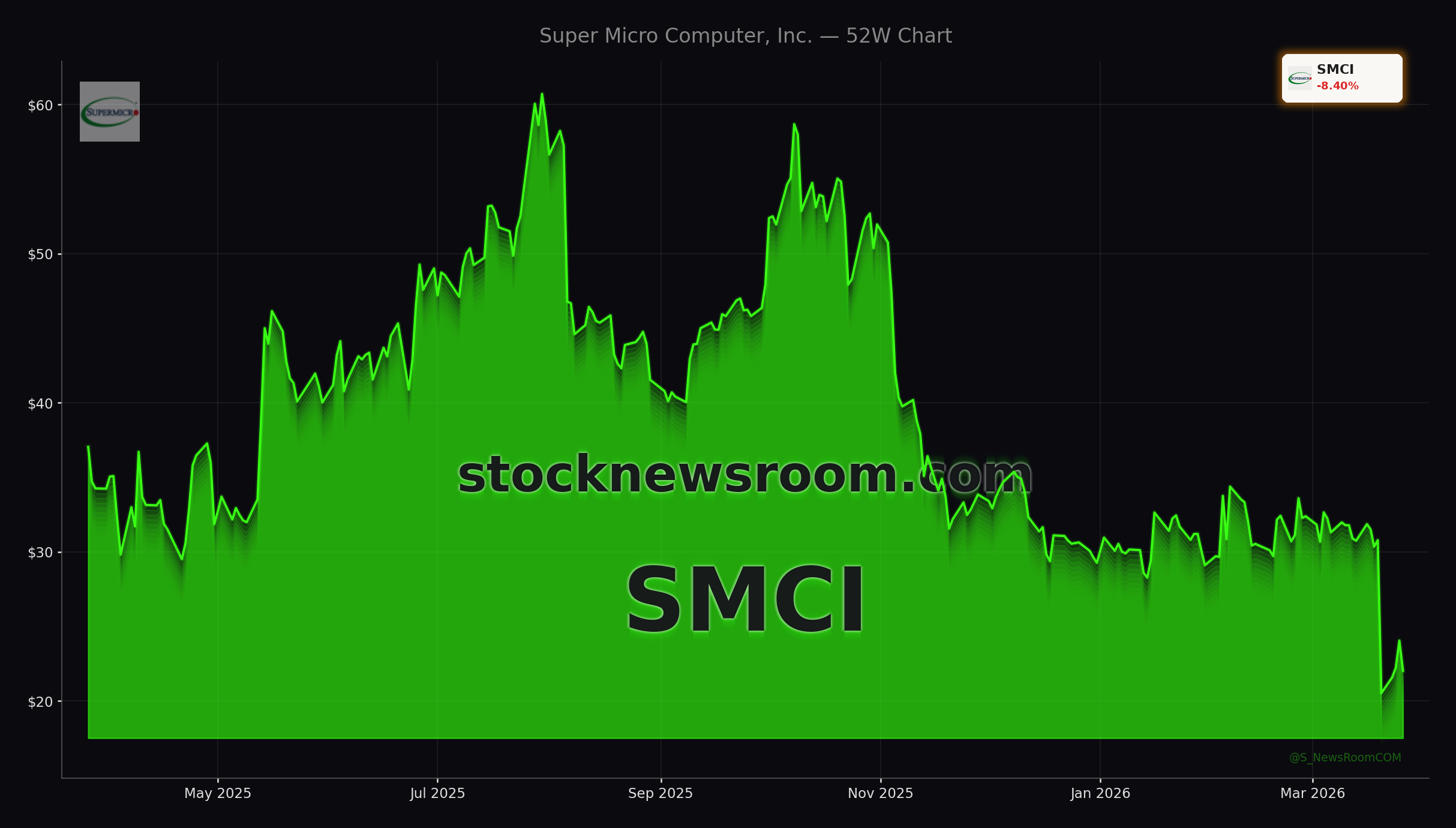

The latest Super Micro Computer Lawsuit activity centers on a series of class actions filed on behalf of investors who bought SMCI stock between April 30, 2024 and March 19, 2026. Law firms including Rosen Law Firm, Faruqi & Faruqi, Holzer & Holzer and several others are vying to represent shareholders, with a key deadline of May 26, 2026 to seek lead‑plaintiff status. The stock’s roughly 8% slide on Thursday to $22.08, versus a previous close of $23.94, extends a month‑long rout that has already erased about 30% of market value and left the shares down nearly 40% year over year.

At the core of the Super Micro Computer Lawsuit allegations is the claim that a “significant portion” of the company’s server sales went to customers in China in ways that allegedly violated U.S. export control laws. Plaintiffs argue that management failed to disclose both the scale of this China exposure and material weaknesses in export‑compliance controls, rendering prior bullish commentary about the business misleading. If a court agrees, the company could face not only damages but potentially tighter regulatory oversight at a time when AI infrastructure is under intense geopolitical scrutiny.

Super Micro Computer and the federal smuggling case

The civil Super Micro Computer Lawsuit headlines are landing against an already fraught legal backdrop. Co‑founder Wally Liaw faces federal charges related to an alleged $2.5 billion AI chip smuggling ring, a case that has startled investors because it directly touches high‑end accelerators that power AI data centers. The company has stressed that it is not a defendant in that federal action, a distinction bulls highlight to argue that legal risk remains contained at the individual level.

However, the new shareholder suits change the risk calculus for institutions. Instead of merely monitoring a founder’s personal legal troubles, investors are now potential plaintiffs themselves, arguing the company misled them. For large funds that must manage headline risk and ESG governance scores alongside returns, that is a material shift. It also raises questions for hyperscale and enterprise customers, which prize rock‑solid compliance when buying sensitive AI server and storage systems.

Can Super Micro Computer’s AI growth offset governance fears?

Despite the Super Micro Computer Lawsuit overhang, the underlying business continues to grow at an extraordinary pace. In Q2 of fiscal 2026, Super Micro Computer, Inc. reported revenue of $12.68 billion, up 123.4% year over year and more than 20% above consensus estimates. Management raised full‑year guidance to roughly $40 billion in sales on the back of a swelling AI server backlog, including more than $13 billion in Blackwell Ultra‑based system orders heading into the quarter.

Super Micro has carved out a central role in the AI infrastructure stack by quickly integrating NVIDIA’s latest RTX PRO Blackwell GPUs and Vera Rubin systems into modular server platforms that target AI factories and cloud data centers. While mega‑caps like Apple and Tesla dominate AI narratives on the NASDAQ, SMCI is one of the few mid‑cap names offering direct exposure to the physical hardware build‑out behind those software and model stories. CEO Charles Liang recently emphasized that the company is scaling its global manufacturing footprint to support “large AI and enterprise deployments,” underscoring management’s conviction that the demand cycle has years to run.

Why margins and the balance sheet worry Wall Street

The challenge for the bull case is that breakneck top‑line growth has not translated into robust profitability. GAAP gross margin shrank to 6.3% in Q2 FY2026, down sharply from 11.8% a year earlier, as component costs, aggressive pricing and mix pressure squeezed the bottom line. While there is some hope that weaker demand and falling prices for certain memory and storage components could ease input cost pressure, the current margin profile leaves little room for error if legal or regulatory costs rise.

At the same time, balance sheet risk is building. Total liabilities surged to $21.01 billion, more than 500% higher year over year, while the company reported negative operating cash flow of roughly $917.5 million in Q1 FY2026. Financing a huge AI build‑out is expensive, and a company with this liability load needs uninterrupted access to credit and unwavering confidence from both customers and suppliers. Any adverse outcome from the Super Micro Computer Lawsuit, or a finding of serious export‑control failures, could complicate that funding picture.

How are Wall Street analysts reacting?

Analysts have been quick to recalibrate expectations as legal and balance‑sheet risks climbed. Citigroup recently cut its SMCI price target from $39 to $25, citing mounting uncertainty and a more cautious stance on near‑term growth. Northland Capital Markets downgraded the stock to “Market Perform” and slashed its target from $63 to $22, with analyst Nehal Chokshi now expecting “flattish” growth instead of the previously assumed steep AI ramp. The current consensus target near $36 masks a wide dispersion of views, reflecting disagreement over whether SMCI is a temporarily dislocated compounder or a structurally impaired governance story.

Relative to larger AI beneficiaries in the S&P 500 and NASDAQ—particularly NVIDIA, which still enjoys stronger margins and a cleaner governance profile—Super Micro now screens as a high‑beta, high‑controversy play. For diversified U.S. portfolios, that makes position sizing and risk management more important than simple enthusiasm for the AI server theme.

Related Coverage

For a deeper look at how export‑control headlines first cracked investor confidence, readers can review Super Micro Computer Export Scandal: +7.2% Rally After a Brutal Crash, which analyzes the initial shock to the stock, the subsequent bounce, and what the early regulatory questions signaled about the company’s risk profile.

With our leading AI server and storage technology foundation, strong customer engagements, and expanding global manufacturing footprint, we are scaling rapidly to support large AI and enterprise deployments while continuing to strengthen our operational and financial execution.— Charles Liang, CEO of Super Micro Computer, Inc.

The Super Micro Computer Lawsuit wave now amplifies an already complex story: hyper‑growth in AI infrastructure, but with thin margins, a stretched balance sheet and rising legal scrutiny. For investors, SMCI has shifted from a straightforward AI hardware play into a legally charged turnaround bet where governance, compliance and cash flow execution will matter as much as Blackwell order momentum in determining long‑term returns.