Is the Super Micro Computer Scandal a lasting threat to its AI server boom, or a brutal buying opportunity after the crash?

How hard did markets hit Super Micro Computer?

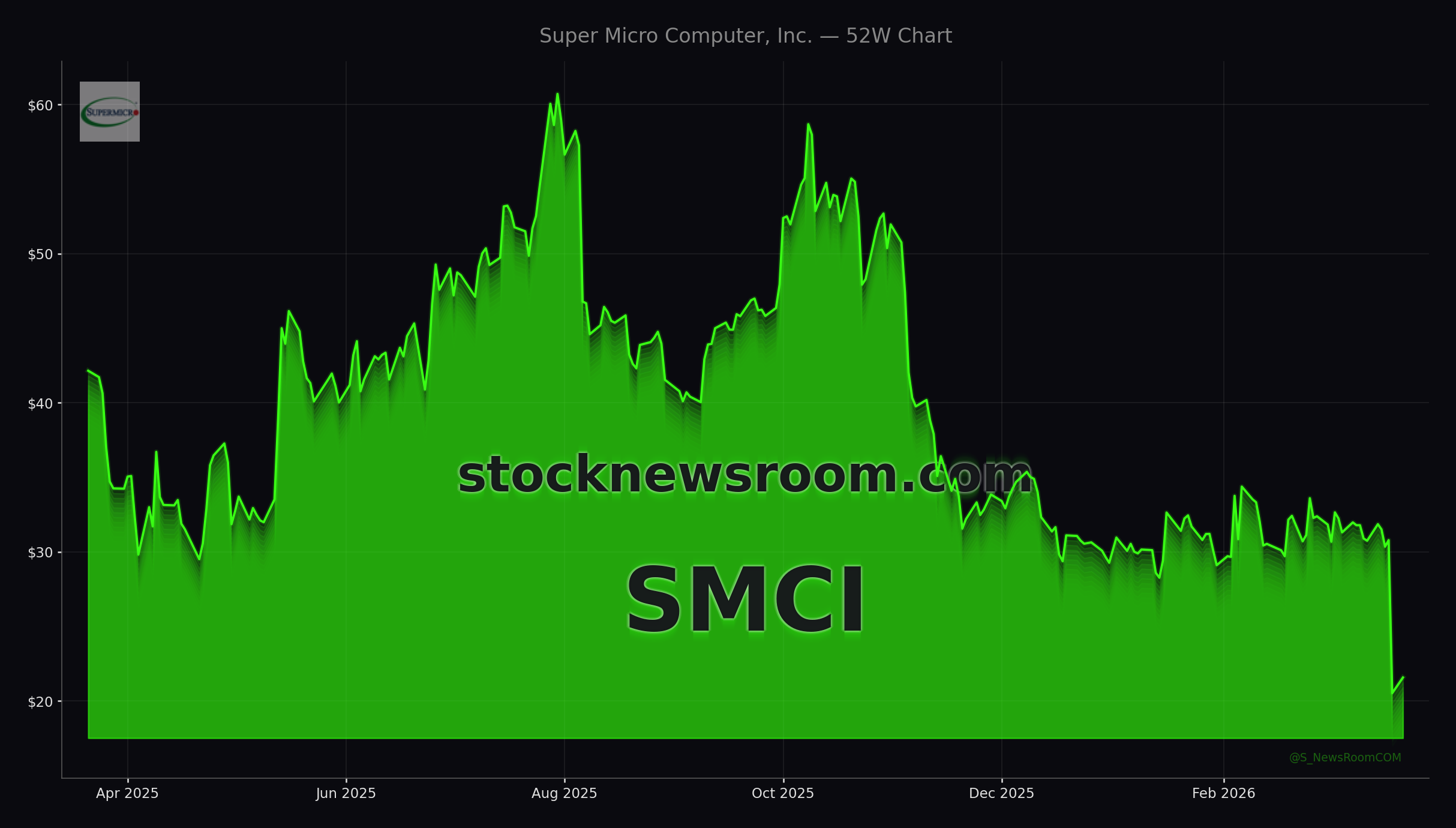

Friday’s collapse wiped out more than $6 billion in market capitalization, marking the steepest one-day drop for Super Micro Computer since October 2018 and turning the Super Micro Computer Scandal into a key cautionary tale for AI‑themed portfolios. After closing at $20.91 on Friday, shares clawed back about 5.11% on Monday to $21.58, trading in a volatile intraday range between $19.48 and $22.14. That still leaves the stock down roughly 30% year to date and almost 49% over the past 12 months, based on its 52‑week range of $19.48 to $62.36.

The selloff also made Super Micro Computer one of the biggest losers in the S&P 500 in the prior session, even as investors remain broadly bullish on AI hardware plays such as NVIDIA. For U.S. technology and growth investors who rode SMCI’s earlier surge as a pure‑play AI server beneficiary alongside names like Tesla and Apple, the scandal has introduced a new layer of risk that goes beyond standard cyclical or valuation concerns.

What triggered the Super Micro Computer Scandal?

Federal prosecutors have indicted three individuals, including co‑founder Yih‑Shyan “Wally” Liaw, in connection with an alleged $2.5 billion AI chip smuggling scheme. The indictment claims the group sold roughly $510 million worth of servers equipped with U.S.-restricted NVIDIA chips through a Southeast Asian intermediary to ultimately reach Chinese customers, allegedly using deceptive methods to bypass U.S. export controls.

Super Micro Computer has emphasized that the alleged conduct violated internal policies and that the company itself has not been named as a defendant in the criminal case. Liaw resigned from the board, was placed on leave, and several employees and at least one contractor linked to the case were terminated. The board also appointed DeAnna Luna as acting Chief Compliance Officer, signaling an attempt to ring‑fence the scandal and strengthen oversight.

Still, the Super Micro Computer Scandal comes against a backdrop of prior accounting irregularities and a near‑delisting from the NASDAQ in earlier years. That history is why many institutional investors are now treating the indictment as a broader governance wake‑up call rather than a one‑off incident.

How are analysts reacting to Super Micro Computer?

Wall Street’s response to the Super Micro Computer Scandal has been swift and mixed. Northland Capital Markets analyst Nehal Chokshi downgraded Super Micro Computer to “market perform” and slashed his price target from $63 to $22, essentially aligning it with the current trading range. Chokshi warned that customer trust could be undermined by the indictment and projected “flattish” growth ahead, a stark contrast to the triple‑digit revenue expansion the company has reported recently.

Argus Research also cut its rating from “buy” to “hold”, arguing that the legal developments could revive concerns over margins, revenue quality and the company’s previous near‑delisting episode. The firm highlighted that the stock may be driven more by headlines than fundamentals in the short term, complicating timing for new entries.

On the other hand, some research houses, including Zacks Investment Research, still point to the company’s role as a full IT solutions provider for AI, cloud, storage and edge computing as a structural positive. With fiscal Q2 2026 revenue reportedly surging 123% year over year to $12.68 billion and management guiding for at least $40 billion in full‑year revenue, the valuation at around 15x earnings appears inexpensive relative to growth. For those bulls, the absence of corporate-level charges is a key reason to treat the selloff as potentially overdone.

What do margins and China exposure tell investors?

Beyond the legal narrative, the Super Micro Computer Scandal is resurfacing questions around profitability. Recent figures show a gross margin of roughly 8–10% (with one estimate at 9.6%), underscoring how intense pricing pressure has become in the AI server space. Despite robust demand for GPU‑rich systems, Super Micro Computer appears to have limited pricing power, likely reflecting a competitive market where multiple integrators and OEMs battle over the same high‑value chips.

Analysts estimate that the allegedly diverted NVIDIA‑based servers tied to Chinese demand represent about 10% of a recent quarter’s revenue, underscoring how meaningful the China channel has been. As Washington tightens export controls on advanced AI hardware, U.S. rivals like Hewlett Packard Enterprise and Dell Technologies are maneuvering to capture compliant demand, while Super Micro Computer must demonstrate that its growth doesn’t rely on gray‑zone sales.

The stock’s violent move has also attracted legal scrutiny: multiple U.S. shareholder-rights law firms have launched investigations into potential securities fraud and disclosure failures, inviting investors who suffered losses to explore possible recovery claims. That adds a civil-litigation overhang on top of the existing criminal case against individuals.

Is the risk-reward now attractive for SMCI?

For U.S. investors, the Super Micro Computer Scandal turns SMCI into a high‑beta governance trade at the center of the AI build‑out. The bull case rests on three pillars: the company is not a named defendant; AI infrastructure demand remains strong; and the current valuation multiple already discounts a significant amount of bad news. Supporters argue that if Super Micro Computer can sustain triple‑digit revenue growth while tightening compliance, the recent crash may look like a buying opportunity in hindsight.

The bear case focuses on reputation and execution risk. Large enterprise and hyperscale customers may hesitate to deepen partnerships with a supplier linked to export‑control violations, especially when they can source similar systems from better‑established peers. With gross margins under visible pressure and new compliance structures still being put to the test, skeptics see limited room for error in the quarters ahead.

The path back to institutional credibility for Super Micro Computer runs through sustained compliance actions, not a single session’s price move.— StockNewsroom.com analysis

Ultimately, the stock’s rebound from around $20 to the low‑$20s on heavy trading volume suggests that speculative money is already trying to time a bottom. Long‑term, risk‑aware investors, however, will likely wait for clearer signs that the governance reset is real and that headline risk from the Super Micro Computer Scandal is starting to fade.