Is Taiwan Semiconductor AI Expansion justifying TSMC’s stunning rally, or are investors pricing in an AI future too far ahead?

How is TSMC’s rally tied to Taiwan Semiconductor AI Expansion?

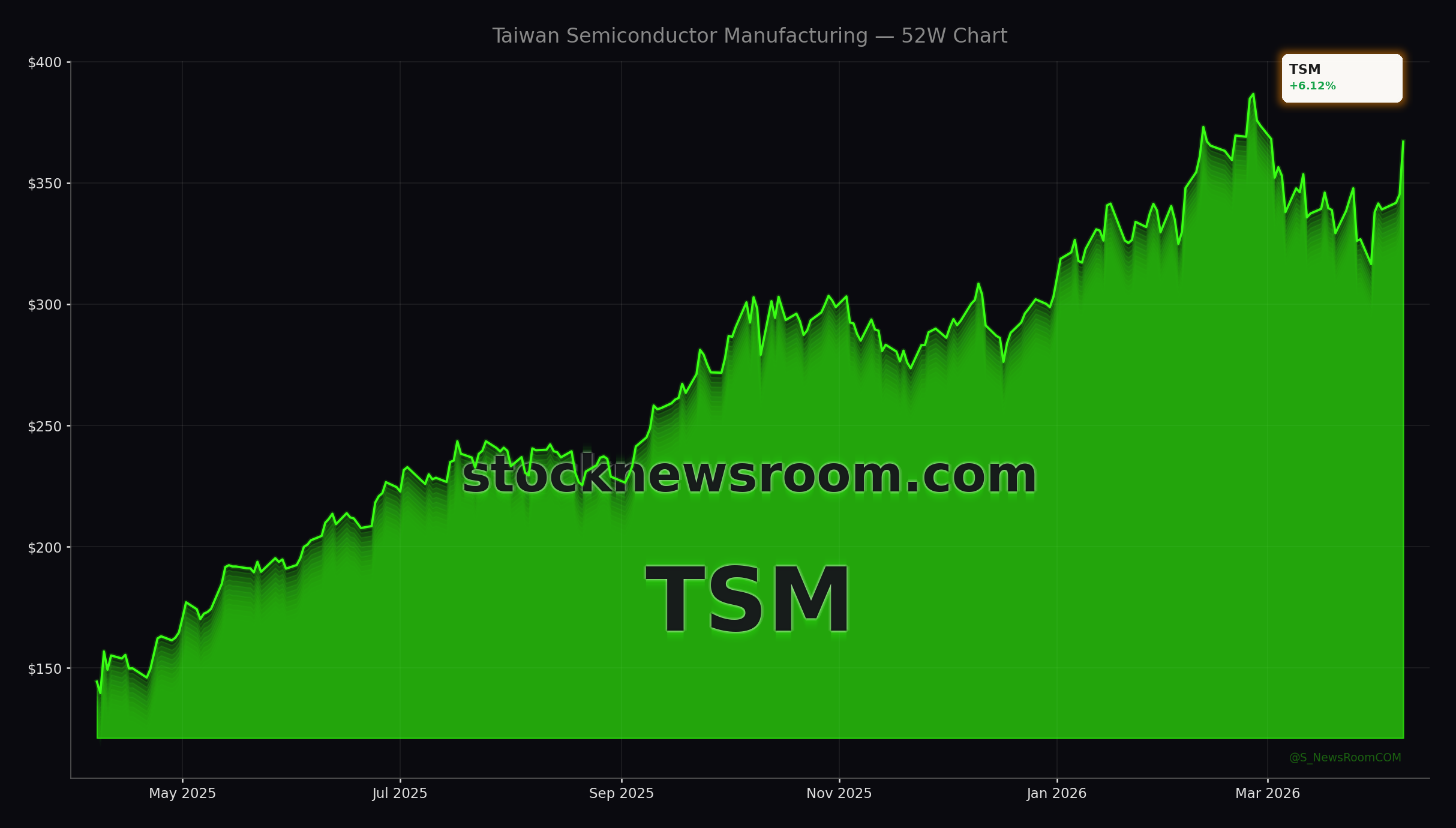

Shares of Taiwan Semiconductor Manufacturing Co. on the NYSE climbed to $366.45 in Wednesday trading, extending a roughly 130% twelve‑month run that has turned the foundry leader into a $1.7 trillion giant by market value. The move comes as institutional demand builds ahead of Q1 earnings, with firms like Aaron Wealth Advisors and Rathbones Group recently boosting positions, while call option activity points to rising conviction that Taiwan Semiconductor AI Expansion will sustain revenue and margin growth.

TSMC is the quintessential “pick‑and‑shovel” play in the AI supercycle, fabricating advanced processors for hyperscalers and chip designers. Rather than betting on which AI software or model will win, investors are targeting the company that supplies the underlying compute – from NVIDIA’s data‑center GPUs to next‑gen CPUs and custom accelerators. With AI capex by cloud giants now well over $200 billion annually, the market sees TSMC as a core infrastructure asset of the NASDAQ‑driven AI trade.

Why does Taiwan Semiconductor AI Expansion matter for AI chips?

TSMC manufactures roughly 90% of the world’s most advanced logic chips at 5nm and below, and has already moved into 2nm mass production with gate‑all‑around (GAA) transistors. That technological lead makes the company indispensable for training and inference hardware used by Apple, Tesla and other platform companies. In effect, Taiwan Semiconductor AI Expansion underpins the ability of Big Tech to ship smaller, more power‑efficient and more performant chips each product cycle.

Management has responded to surging demand by sharply increasing capital expenditures to expand leading‑edge capacity in Taiwan, Japan and the U.S. Unlike hyperscalers that can dial back data‑center spend relatively easily, TSMC’s decision to add multi‑billion‑dollar fabs suggests strong visibility into long‑term AI economics. If these fabs were to sit idle, it would be a direct hit to the company’s core business, so the aggressive capex is itself a signal that AI workloads are expected to remain a durable growth driver.

Is advanced packaging the new AI bottleneck for TSMC?

Even as wafer capacity grows, the next choke point in the AI hardware stack is emerging in advanced packaging – the process of integrating multiple dies into a single module that can be used in servers and high‑end systems. Today almost all high‑end packaging for AI accelerators is concentrated in Asia, and capacity is tight. TSMC’s Chip‑on‑Wafer‑on‑Substrate (CoWoS) technology, used in many of NVIDIA’s GPUs, is seeing demand grow at an estimated 80% compound rate as AI clusters scale.

TSMC is responding by ramping two new packaging facilities in Taiwan and planning two more U.S. sites in Arizona, which in time should reduce reliance on shipping wafers back to Taiwan from its Phoenix fab. The latest CoWoS‑L generation is particularly critical, as high‑end products like NVIDIA Blackwell reportedly tie up a large portion of this capacity. Longer term, the company is pushing toward 3D stacking with its SoIC platform, which stacks chips vertically for higher bandwidth and lower latency – another pillar of Taiwan Semiconductor AI Expansion.

How are analysts and valuation framing Taiwan Semiconductor AI Expansion?

After its 136% one‑year surge, TSMC’s valuation is under scrutiny on Wall Street. A recent discounted cash flow analysis suggested the shares may trade modestly above intrinsic value, yet on a price‑to‑earnings basis the stock looks more reasonable with a multiple in the high‑20s, not far from or below many U.S. high‑growth peers in the semiconductor space. Several research houses, including MarketBeat‑tracked brokerages, maintain Buy or Strong Buy ratings with an average price target near $390, implying upside from current levels.

Large asset managers have continued to add TSMC as a top‑tier holding, even as some hedge funds trim exposure following the rally. For U.S. investors building AI‑heavy portfolios dominated by names like NVIDIA and cloud hyperscalers, Taiwan Semiconductor AI Expansion offers diversification along the supply chain while still capturing the same secular tailwind. The flip side is that an investment in TSMC also embeds geopolitical and supply‑chain risk tied to Taiwan’s strategic position, energy constraints, and the cost and execution challenges of global fab projects in the U.S. and Japan.

How does Intel’s push change the AI foundry race?

Competition is intensifying as Intel pursues its own advanced packaging and foundry strategy, targeting AI customers including Elon Musk’s ecosystem. Intel’s EMIB and Foveros technologies rival TSMC’s CoWoS and SoIC approaches, while new alliances aim to claw back share in high‑performance compute. For now, however, TSMC remains the volume and technology leader, and most bleeding‑edge AI designs still rely on its process technology.

For S&P 500 and NASDAQ investors, this evolving race means Taiwan Semiconductor AI Expansion should be analyzed in the context of a broader ecosystem that includes Intel, AMD and U.S. equipment makers, not in isolation. Shifts in packaging capacity, customer mix, and government incentives could all alter relative economics between foundries over the next few years.

Related Coverage

For a deeper look at supply‑chain vulnerabilities, including gas constraints, readers can explore how a potential helium squeeze might affect TSMC’s output in “Taiwan Semiconductor Helium Shortage: +1.7% AI Shock”. That piece examines whether a Taiwan‑centered helium disruption could quietly derail part of the AI chip boom just as demand hits overdrive.

Investors tracking the competitive response should also read “Intel Terafab +9.7% Surge: Musk Alliance Reboots AI Foundry”, which analyzes how Intel’s Terafab initiative and partnerships across Elon Musk’s companies aim to reboot its AI ambitions and potentially reshape the foundry landscape that TSMC currently dominates.

In sum, Taiwan Semiconductor AI Expansion has cemented TSMC as the central infrastructure provider of the AI era, with today’s share price strength reflecting that status. For long‑term investors, the stock offers a way to own the backbone of global AI compute, while remaining sensitive to execution and geopolitical risks. The next few quarters of capacity ramp‑up, packaging build‑out and AI capex trends will show whether TSMC can continue to justify its premium and extend its lead in the chip revolution.